Chapter 10: Bayesian Model Selection

Chapter10.RmdSection 10.1: The Foundations of Bayesian Model Selection

Table 10.1: (Log) Bayes factor and model probabilities

library("BayesianLearningCode")

logBF <- -7:7

BF <- exp(logBF)

PrM1 <- BF / (1 + BF)

PrM2 <- 1 - PrM1

knitr::kable(cbind(BF, logBF, PrM1, PrM2))| BF | logBF | PrM1 | PrM2 |

|---|---|---|---|

| 0.0009119 | -7 | 0.0009111 | 0.9990889 |

| 0.0024788 | -6 | 0.0024726 | 0.9975274 |

| 0.0067379 | -5 | 0.0066929 | 0.9933071 |

| 0.0183156 | -4 | 0.0179862 | 0.9820138 |

| 0.0497871 | -3 | 0.0474259 | 0.9525741 |

| 0.1353353 | -2 | 0.1192029 | 0.8807971 |

| 0.3678794 | -1 | 0.2689414 | 0.7310586 |

| 1.0000000 | 0 | 0.5000000 | 0.5000000 |

| 2.7182818 | 1 | 0.7310586 | 0.2689414 |

| 7.3890561 | 2 | 0.8807971 | 0.1192029 |

| 20.0855369 | 3 | 0.9525741 | 0.0474259 |

| 54.5981500 | 4 | 0.9820138 | 0.0179862 |

| 148.4131591 | 5 | 0.9933071 | 0.0066929 |

| 403.4287935 | 6 | 0.9975274 | 0.0024726 |

| 1096.6331584 | 7 | 0.9990889 | 0.0009111 |

Example 10.5: CHF exchange rate data - Testing for zero mean

Before producing Figure 10.1, we begin with a concrete example. We load the data, compute the required parameters, and evaluate the two marginal likelihoods.

data("exrates", package = "stochvol")

y <- 100 * diff(log(exrates$USD / exrates$CHF))

c0 <- 1

C0 <- 1

N0 <- 10^(-5:3)

N <- length(y)

cN <- c0 + N / 2

CN_M1 <- C0 + sum(y^2) / 2

CN_M2 <- C0 + 0.5 * N * (mean((y - mean(y))^2) + N0 / (N0 + N) * mean(y)^2)

(logmarglikM1 <- lgamma(cN) + c0 * log(C0) -

lgamma(c0) - cN * log(CN_M1) - 0.5 * N * log(2 * pi))

#> [1] -3456.478

(logmarglikM2 <- lgamma(cN) + c0 * log(C0) + 0.5 * log(N0) -

lgamma(c0) - cN * log(CN_M2) - 0.5 * N * log(2 * pi) - 0.5 * log(N0 + N))

#> [1] -3465.344 -3464.192 -3463.041 -3461.890 -3460.739 -3459.588 -3458.440

#> [8] -3457.329 -3456.493The “direct” formula for the log Bayes factor is even simpler, and we can check whether we get the same answer.

(logBF <- 0.5 * (log(N0 + N) - log(N0)) + cN * (log(CN_M2) - log(CN_M1)))

#> [1] 8.86553606 7.71424355 6.56295141 5.41166293 4.26041101 3.10952463 1.96228321

#> [8] 0.85048010 0.01501194

all.equal(logBF, logmarglikM1 - logmarglikM2)

#> [1] TRUENow we are ready to investigate the sensitivity of the log Bayes factor with respect to prior hyperparameter choices.

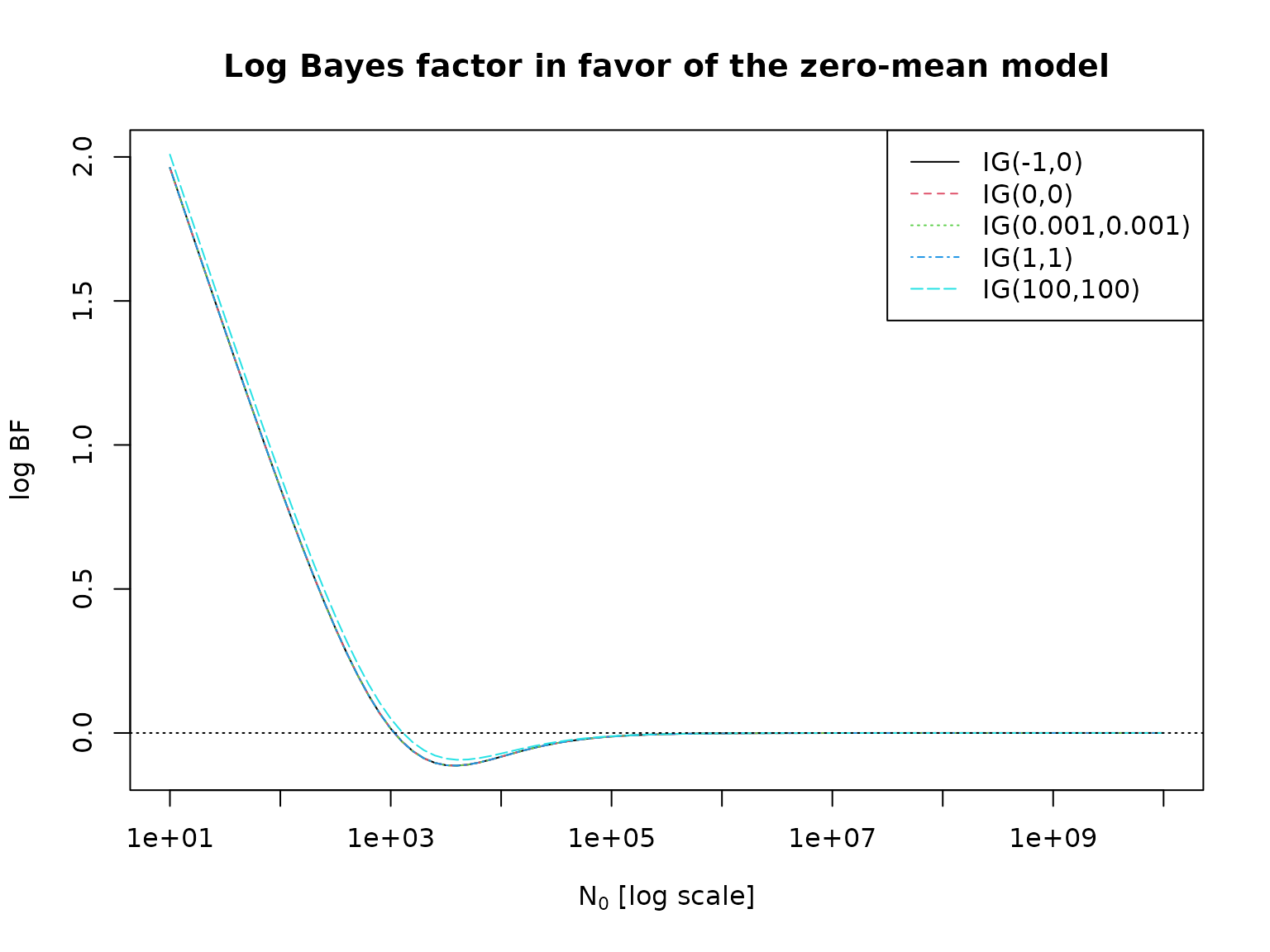

c0 <- c(-1, 0, 0.001, 1, 100)

C0 <- c(0, 0, 0.001, 1, 100)

N0 <- 10^seq(1, 10, by = 0.1)

logBF <- matrix(NA_real_, nrow = length(N0), ncol = length(c0))

for (i in seq_along(c0)) {

cN <- c0[i] + N / 2

CN_M1 <- C0[i] + sum(y^2) / 2

CN_M2 <- C0[i] + 0.5 * N * (mean((y - mean(y))^2) + N0 / (N0 + N) * mean(y)^2)

logBF[, i] <- 0.5 * (log(N0 + N) - log(N0)) + cN * (log(CN_M2) - log(CN_M1))

}

matplot(N0, logBF, log = "x", type = "l",

xlab = expression(paste(N[0], " [log scale]")), ylab = "log BF")

abline(h = 0, lty = 3)

legend("topright", paste0("IG(", c0, ",", C0, ")"), col = seq_along(c0),

lty = seq_along(c0))

title("Log Bayes factor in favor of the zero-mean model")

Section 10.2: Bayesian Testing of Hypotheses

Example 10.6: Labor market data - Testing for heterogeneity of the no-income risk

First, we re-load the data from Chapter 3.

data("labor", package = "BayesianLearningCode")

labor <- subset(labor,

income_1997 != "zero" & female,

c(income_1998, wcollar_1986))

labor <- with(labor,

data.frame(unemployed = income_1998 == "zero",

wcollar = wcollar_1986))Next, we compute the marginal likelihoods for the homogeneity model.

N <- length(labor$unemployed)

SN <- sum(labor$unemployed)

hN <- SN / N

N0 <- c(2, 10)

a0 <- c(1, 0.5, hN * N0)

b0 <- c(1, 0.5, N0 * (1 - hN))

aN <- a0 + sum(labor$unemployed)

bN <- b0 + N - sum(labor$unemployed)

logmarglikM1 <- lbeta(aN, bN) - lbeta(a0, b0)And for the heterogeneity model.

N1 <- with(labor, sum(wcollar))

SN1 <- with(labor, sum(wcollar & unemployed))

N2 <- with(labor, sum(!wcollar))

SN2 <- with(labor, sum(!wcollar & unemployed))

hN <- (SN1 + SN2) / (N1 + N2) # redundant, same as above

a01 <- a02 <- c(1, 0.5, hN * N0) # redundant, same as a0

b01 <- b02 <- c(1, 0.5, N0 * (1 - hN)) # redundant, same as b0

aN1 <- a01 + SN1

bN1 <- b01 + N1 - SN1

aN2 <- a02 + SN2

bN2 <- b02 + N2 - SN2

logmarglikM2 <- lbeta(aN1, bN1) + lbeta(aN2, bN2) -

lbeta(a01, b01) - lbeta(a02, b02)We can now compute the model probabilities and the log BFs.

logBF <- logmarglikM1 - logmarglikM2

PrM2 <- 0.5 / (0.5 + 0.5 * exp(logBF))

PrM1 <- 1 - PrM2

#print(xtable::xtable(res, digits = c(0, 2, 2, 5, 5, 5), row.names = FALSE))

knitr::kable(res <- cbind(logmarglikM1, logmarglikM2, logBF, PrM1, PrM2))| logmarglikM1 | logmarglikM2 | logBF | PrM1 | PrM2 |

|---|---|---|---|---|

| -387.5820 | -385.9187 | -1.663244 | 0.1593270 | 0.8406730 |

| -387.5560 | -385.8867 | -1.669302 | 0.1585173 | 0.8414827 |

| -387.2933 | -385.3980 | -1.895305 | 0.1306408 | 0.8693592 |

| -386.2587 | -383.4054 | -2.853317 | 0.0545101 | 0.9454899 |

Example 10.7: Stomach cancer data - Testing for heterogeneity of the mortality rate

We proceed exactly as above, just with different data.

N1 <- 1668 # number at risk in City A

SN1 <- 2 # cancer deaths in City A

N2 <- 583 # number at risk in City B

SN2 <- 1 # cancer deaths in City BWe again begin with the homogeneity model.

N <- N1 + N2

SN <- SN1 + SN2

hN <- SN / N

N0 <- c(2, 10)

a0 <- c(1, 0.5, hN * N0)

b0 <- c(1, 0.5, N0 * (1 - hN))

aN <- a0 + SN

bN <- b0 + N - SN

logmarglikM1 <- lbeta(aN, bN) - lbeta(a0, b0)Followed by the heterogeneity model.

a01 <- a02 <- a0

b01 <- b02 <- b0

aN1 <- a01 + SN1

bN1 <- b01 + N1 - SN1

aN2 <- a02 + SN2

bN2 <- b02 + N2 - SN2

logmarglikM2 <- lbeta(aN1, bN1) + lbeta(aN2, bN2) -

lbeta(a01, b01) - lbeta(a02, b02)We can now compute the model probabilities and the log BFs.

logBF <- logmarglikM1 - logmarglikM2

PrM2 <- 0.5 / (0.5 + 0.5 * exp(logBF))

PrM1 <- 1 - PrM2

#print(xtable::xtable(res, digits = c(0, 2, 2, 3, 3, 3), row.names = FALSE))

knitr::kable(res <- cbind(logmarglikM1, logmarglikM2, logBF, PrM1, PrM2))| logmarglikM1 | logmarglikM2 | logBF | PrM1 | PrM2 |

|---|---|---|---|---|

| -29.08387 | -34.30308 | 5.219212 | 0.9946175 | 0.0053825 |

| -26.95877 | -30.22452 | 3.265757 | 0.9632352 | 0.0367648 |

| -28.40707 | -33.09584 | 4.688776 | 0.9908859 | 0.0091141 |

| -26.84585 | -29.97906 | 3.133212 | 0.9582421 | 0.0417579 |

Example 10.8: Testing for a structural break in the road safety data

We load the data.

data("accidents", package = "BayesianLearningCode")We define the priors hyperparameters and compute the log marginal likelihood for the exchangable model.

y <- accidents[, "children_accidents"]

a0_tmp <- c(0.01, 0.1, 0.5, 1, 2)

m0_tmp <- c(1, mean(y), 5, 7, 10)

grid <- expand.grid(a0 = a0_tmp, m0 = m0_tmp)

a0 <- grid$a0

b0 <- grid$a0 / grid$m0

aN <- sum(y) + a0

bN <- length(y) + b0

logmarglikM1 <- matrix(a0 * log(b0) + lgamma(aN) -

aN * log(bN) - lgamma(a0) -

sum(lgamma(y + 1)),

nrow = length(a0_tmp), ncol = length(m0_tmp),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2)))

knitr::kable(round(logmarglikM1, 2))| 1 | 1.84 | 5 | 7 | 10 | |

|---|---|---|---|---|---|

| 0.01 | -320.55 | -320.55 | -320.55 | -320.55 | -320.56 |

| 0.1 | -318.50 | -318.47 | -318.51 | -318.53 | -318.56 |

| 0.5 | -317.43 | -317.31 | -317.49 | -317.61 | -317.75 |

| 1 | -317.12 | -316.89 | -317.26 | -317.49 | -317.77 |

| 2 | -316.96 | -316.51 | -317.24 | -317.70 | -318.26 |

And now the same for the model with structural break.

accidents1 <- window(accidents, end = c(1994, 9))

accidents2 <- window(accidents, start = c(1994, 10))

a01 <- a02 <- a0

b01 <- b02 <- b0

aN1 <- a01 + sum(accidents1[, "children_accidents"])

aN2 <- a02 + sum(accidents2[, "children_accidents"])

bN1 <- b01 + length(accidents1[, "children_accidents"])

bN2 <- b02 + length(accidents2[, "children_accidents"])

logmarglikM2 <- matrix(a01 * log(b01) + lgamma(aN1) +

a02 * log(b02) + lgamma(aN2) -

aN1 * log(bN1) - lgamma(a01) -

aN2 * log(bN2) - lgamma(a02) -

sum(lgamma(y + 1)),

nrow = length(a0_tmp), ncol = length(m0_tmp),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2)))

knitr::kable(round(logmarglikM2, 2))| 1 | 1.84 | 5 | 7 | 10 | |

|---|---|---|---|---|---|

| 0.01 | -321.40 | -321.40 | -321.40 | -321.41 | -321.41 |

| 0.1 | -317.30 | -317.25 | -317.33 | -317.37 | -317.43 |

| 0.5 | -315.17 | -314.94 | -315.31 | -315.54 | -315.81 |

| 1 | -314.58 | -314.12 | -314.85 | -315.31 | -315.86 |

| 2 | -314.30 | -313.38 | -314.83 | -315.75 | -316.86 |

We can now compute log Bayes factors and corresponding model probabilities (under uniform prior probabilities).

logBF <- logmarglikM1[, 2] - logmarglikM2[, 2]

PrM2 <- 0.5 / (0.5 + 0.5 * exp(logBF))

PrM1 <- 1 - PrM2

knitr::kable(round(rbind(PrM1, PrM2), 3))| 0.01 | 0.1 | 0.5 | 1 | 2 | |

|---|---|---|---|---|---|

| PrM1 | 0.701 | 0.228 | 0.086 | 0.059 | 0.042 |

| PrM2 | 0.299 | 0.772 | 0.914 | 0.941 | 0.958 |

Example 10.9: CHF exchange rate data - Testing normal versus Student t

After loading the data, we define the degrees of freedom and the prior hyperparameters.

y <- 100 * diff(log(exrates$USD / exrates$CHF))

N <- length(y)

nu <- 7

c10 <- c30 <- 3

C10 <- 3

C30 <- (nu - 2) / nu * C10We now compute log marginal likelihoods. This is straightforward for the normal model.

c1N <- c10 + N / 2

C1N <- C10 + sum(y^2) / 2

logmarglikM1 <- lgamma(c1N) + c10 * log(C10) -

lgamma(c10) - c1N * log(C1N) - 0.5 * N * log(2 * pi)For the Student model, we need, e.g., numerical integration. Note that we apply the “log-sum-exp” trick here to normalize the integrand so that its maximum is 1.

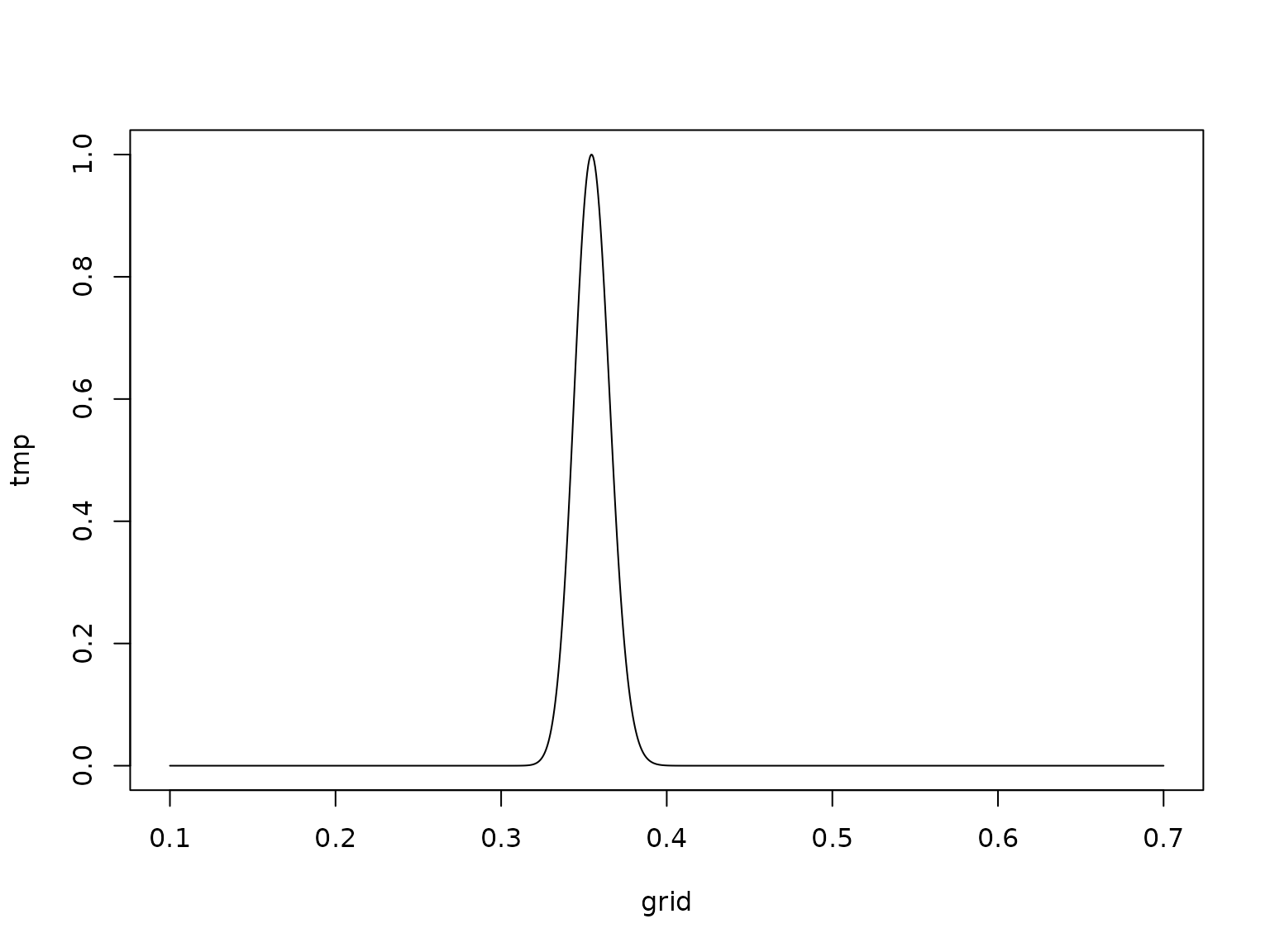

integrand_nonvec <- function(sigma2, y, c0, C0, nu, const = 0, log = FALSE) {

N <- length(y)

logint <- -(N/2 + c0 + 1) * log(sigma2) -

0.5 * (nu + 1) * sum(log(1 + y^2 / (nu * sigma2))) -

C0 / sigma2

if (log) logint + const else exp(logint + const)

}

integrand <- Vectorize(integrand_nonvec, "sigma2")

resolution <- 1000

grid <- seq(0.1, 0.7, length.out = resolution + 1)

logtmp <- integrand(grid, y, c30, C30, nu, log = TRUE)

const <- -max(logtmp)

tmp <- exp(logtmp + const)

plot(grid, tmp, type = 'l')

logarea <- log(sum(diff(grid) * .5 * (head(tmp, -1) + tail(tmp, -1)))) - const

logmarglikM3 <- c30 * log(C30) +

N * lgamma((nu + 1) / 2) -

lgamma(c30) -

N * lgamma(nu / 2) -

N / 2 * log(nu * pi) +

logareaWe can now compute log Bayes factors and corresponding model probabilities (under equal prior model probabilities).

logBF <- logmarglikM1 - logmarglikM3

PrM3 <- 0.5 / (0.5 + 0.5 * exp(logBF))

PrM1 <- 1 - PrM3

knitr::kable(cbind(logML1 = logmarglikM1, logML3 = logmarglikM3,

BF = exp(logBF), logBF = logBF, Pr1 = PrM1, Pr3 = PrM3))| logML1 | logML3 | BF | logBF | Pr1 | Pr3 |

|---|---|---|---|---|---|

| -3456.384 | -3305.694 | 0 | -150.6898 | 0 | 1 |

Example 10.10: Eye tracking data - Testing homogeneity against unobserved heterogeneity

We begin by loading the data and specifying the hyperparameters.

data("eyetracking", package = "BayesianLearningCode")

y <- eyetracking$anomalies

N <- length(y)

a0_tmp <- c(0.1, 0.5, 1, 2)

m0_tmp <- c(1, mean(y), 5, 10, 20)

grid <- expand.grid(a0 = a0_tmp, m0 = m0_tmp)

a0 <- grid$a0

m0 <- grid$m0

b0 <- a0 / m0Now we can compute and print the log marginal likelihoods.

logmarglikM1 <- a0 * log(b0) + lgamma(a0 + sum(y)) -

lgamma(a0) - (a0 + sum(y)) * log(b0 + N) -

sum(lgamma(y + 1))

logmarglikM2 <- rep(NA_real_, length(a0))

for (i in seq_along(a0)) {

logmarglikM2[i] <- N * a0[i] * log(b0[i]) + sum(lgamma(a0[i] + y)) -

N * lgamma(a0[i]) - sum(a0[i] + y) * log(b0[i] + 1) -

sum(lgamma(y + 1))

}

resM1 <- matrix(logmarglikM1, nrow = length(a0_tmp), ncol = length(m0_tmp),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2)))

resM2 <- matrix(logmarglikM2, nrow = length(a0_tmp), ncol = length(m0_tmp),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2)))

knitr::kable(resM1, digits = 2)| 1 | 3.52 | 5 | 10 | 20 | |

|---|---|---|---|---|---|

| 0.1 | -472.91 | -472.78 | -472.78 | -472.82 | -472.87 |

| 0.5 | -472.25 | -471.62 | -471.64 | -471.81 | -472.07 |

| 1 | -472.45 | -471.20 | -471.25 | -471.59 | -472.11 |

| 2 | -473.31 | -470.81 | -470.92 | -471.60 | -472.63 |

knitr::kable(resM2, digits = 2)| 1 | 3.52 | 5 | 10 | 20 | |

|---|---|---|---|---|---|

| 0.1 | -249.61 | -237.68 | -238.22 | -241.61 | -246.80 |

| 0.5 | -271.04 | -223.77 | -226.24 | -242.34 | -267.54 |

| 1 | -316.77 | -241.38 | -245.87 | -276.12 | -324.87 |

| 2 | -381.56 | -273.80 | -281.39 | -335.39 | -426.86 |

Example 10.11: Eye tracking data - Testing Poisson vs. negative binomial

In the negative binomial case, if is fixed and follows a beta prime prior, we have a closed-form expression for the marginal likelihood.

alpha_b0 <- rep(6, length(a0))

beta_b0 <- (alpha_b0 - 1) * m0 / a0

sdb0 <- sqrt(alpha_b0 * (alpha_b0 + beta_b0 - 1) /

((beta_b0 - 2) * (beta_b0 - 1)^2))

alpha_bN <- alpha_b0 + N * a0

beta_bN <- beta_b0 + sum(y)

logmarglikM3 <- rep(NA_real_, length(a0))

for (i in seq_along(a0)) {

logmarglikM3[i] <- lbeta(alpha_bN[i], beta_bN[i]) - lbeta(alpha_b0[i], beta_b0[i]) -

N * lgamma(a0[i]) + sum(lgamma(a0[i] + y)) - sum(lgamma(y + 1))

}

resM3 <- matrix(logmarglikM3, nrow = length(a0_tmp), ncol = length(m0_tmp),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2)))

knitr::kable(resM3, digits = 2)| 1 | 3.52 | 5 | 10 | 20 | |

|---|---|---|---|---|---|

| 0.1 | -241.31 | -238.24 | -238.23 | -239.61 | -242.82 |

| 0.5 | -228.15 | -224.98 | -224.96 | -227.12 | -233.66 |

| 1 | -245.75 | -242.92 | -242.88 | -245.01 | -252.11 |

| 2 | -278.03 | -275.68 | -275.62 | -277.48 | -284.21 |

Example 10.12: CHF exchange rate data - Savage-Dickey density ratio

y <- 100 * diff(log(exrates$USD / exrates$CHF))

c0R <- 1

c0U <- c0R - 1/2 # This is needed for the SD theorem to be valid!

C0 <- 1

N0 <- 10^(2:5)

N <- length(y)

bNs <- sum(y) / (N0 + N)

cNR <- c0R + N / 2

cNU <- c0U + N / 2

CNs <- C0 + 0.5 * sum((y - mean(y))^2) + 0.5 * N * N0 * mean(y)^2 / (N0 + N)

(logSD <- dstudt(0, bNs, sqrt(CNs / (cNU * (N0 + N))), df = 2 * cNU, log = TRUE) -

dstudt(0, 0, sqrt(C0 / (c0U * N0)), df = 2 * c0U, log = TRUE))

#> [1] 1.7416826 0.9061529 0.8085183 0.8784890Let us double-check this:

CN_M1 <- C0 + sum(y^2) / 2

logmarglikM1 <- lgamma(cNR) + c0R * log(C0) -

lgamma(c0R) - cNR * log(CN_M1) - 0.5 * N * log(2 * pi)

logmarglikM2 <- lgamma(cNU) + c0U * log(C0) + 0.5 * log(N0) -

lgamma(c0U) - cNU * log(CNs) - 0.5 * N * log(2 * pi) - 0.5 * log(N0 + N)

(logBF <- logmarglikM1 - logmarglikM2)

#> [1] 1.7416826 0.9061529 0.8085183 0.8784890

all.equal(logSD, logBF)

#> [1] TRUEHere is a visualization.

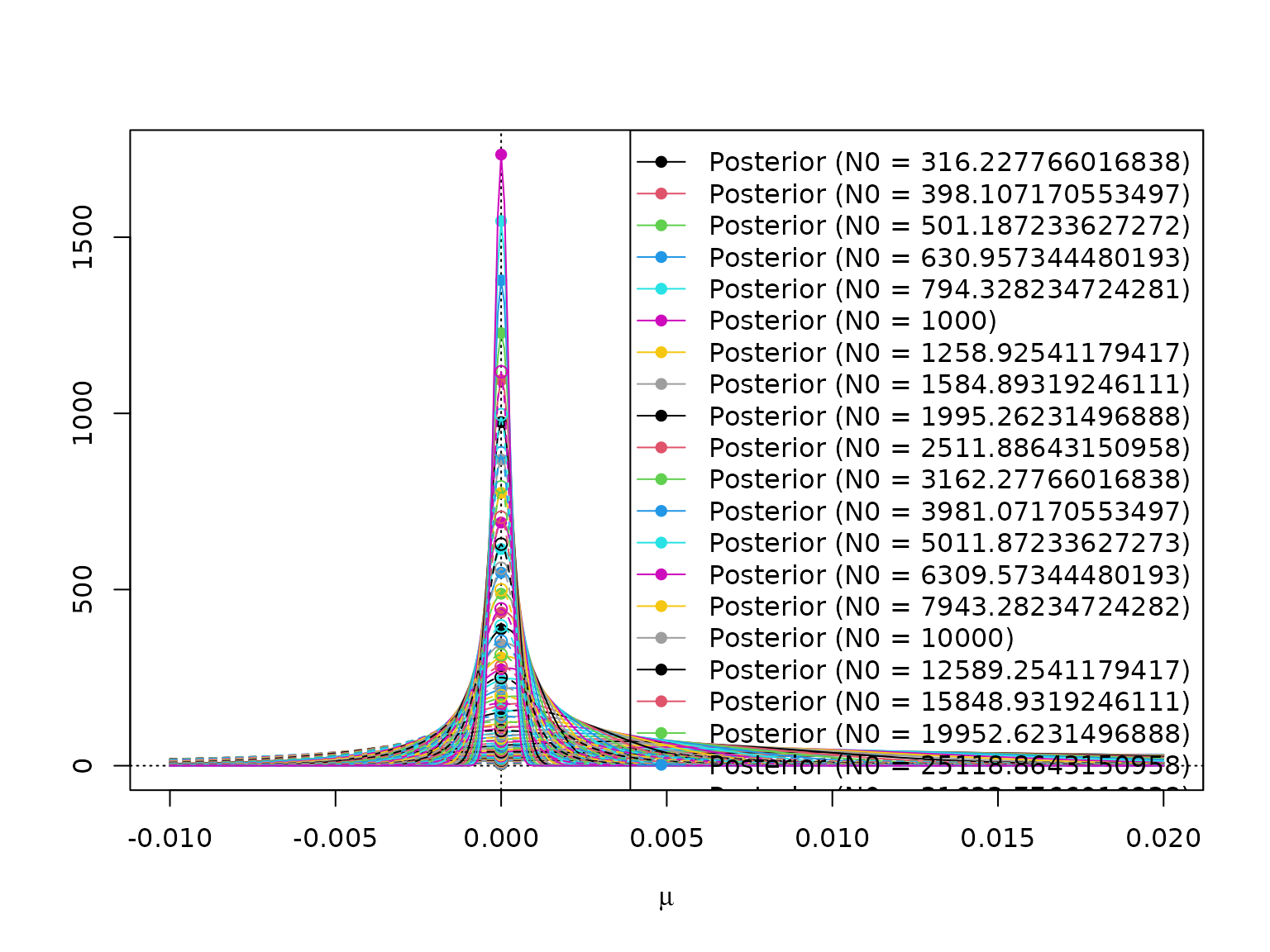

par(mar = c(2.5, 1.5, .5, .5), mgp = c(1.6, .6, 0))

mus <- seq(-.01, .02, 0.0001)

plot(NULL, xlim = range(mus), log = "", xlab = expression(mu), ylab = "",

ylim = range(dstudt(mus,

bNs[length(N0)],

sqrt(CNs[length(N0)] / (cNU * (N0[length(N0)] + N))),

df = 2 * cNU)))

abline(v = 0, lty = 3)

abline(h = 0, lty = 3)

for (i in seq_along(N0)) {

lines(mus, dstudt(mus, 0, sqrt(C0 / (c0R * N0[i])), df = 2 * c0R),

lty = 2, col = i)

lines(mus, dstudt(mus, bNs[i], sqrt(CNs[i] / (cNU * (N0[i] + N))), df = 2 * cNU),

lty = 1, col = i)

points(c(0, 0),

c(dstudt(0, 0, sqrt(C0 / (c0R * N0[i])), df = 2 * c0R),

dstudt(0, bNs[i], sqrt(CNs[i] / (cNU * (N0[i] + N))), df = 2 * cNU)),

col = i, pch = c(1, 16))

}

op <- options(scipen = 999) # to avoid scientific notation

legend("topright", parse(text = c(paste0("Posterior ~ (N[0] == ", N0, ")"),

paste0("Prior ~ (N[0] == ", N0, ")"))),

lty = rep(c(1, 2), each = length(N0)),

pch = rep(c(16, 1), each = length(N0)),

col = rep(seq_along(N0), 2))

options(op) # reset to allow scientific notationFinally, we repeat the exercise for a higher number of different values of .

par(mar = c(2.5, 2.5, 1.5, .5), mgp = c(1.6, .6, 0))

N0 <- 10^seq(1, 10, by = 0.1)

N <- length(y)

bNs <- sum(y) / (N0 + N)

cNR <- c0R + N / 2

cNU <- c0U + N / 2

CNs <- C0 + 0.5 * sum((y - mean(y))^2) + 0.5 * N * N0 * mean(y)^2 / (N0 + N)

logSD <- dstudt(0, bNs, sqrt(CNs / (cNU * (N0 + N))), df = 2 * cNU, log = TRUE) -

dstudt(0, 0, sqrt(C0 / (c0U * N0)), df = 2 * c0U, log = TRUE)

plot(N0, logSD, type = "l", log = "x", ylim = c(0, max(logSD)),

xlab = expression(paste(N[0], " [log scale]")), ylab = "log BF",

main = "Log Bayes factor in favor of the zero-mean model")

abline(h = 0, lty = 3)

abline(h = logSD[length(logSD)], lty = 2)

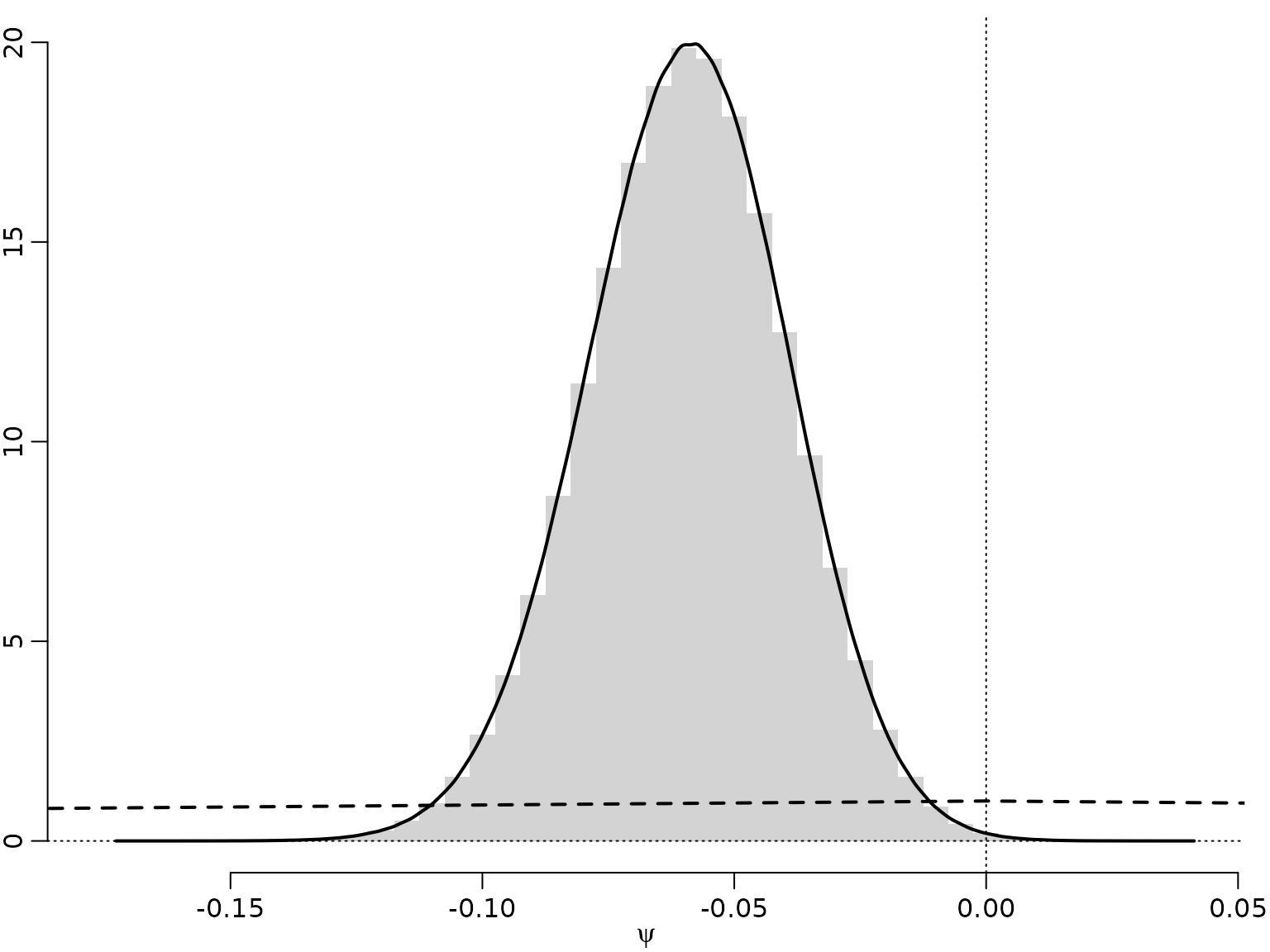

Example 10.13: Labor market data - Savage-Dickey density ratio for the no-income-risk homogeneity test

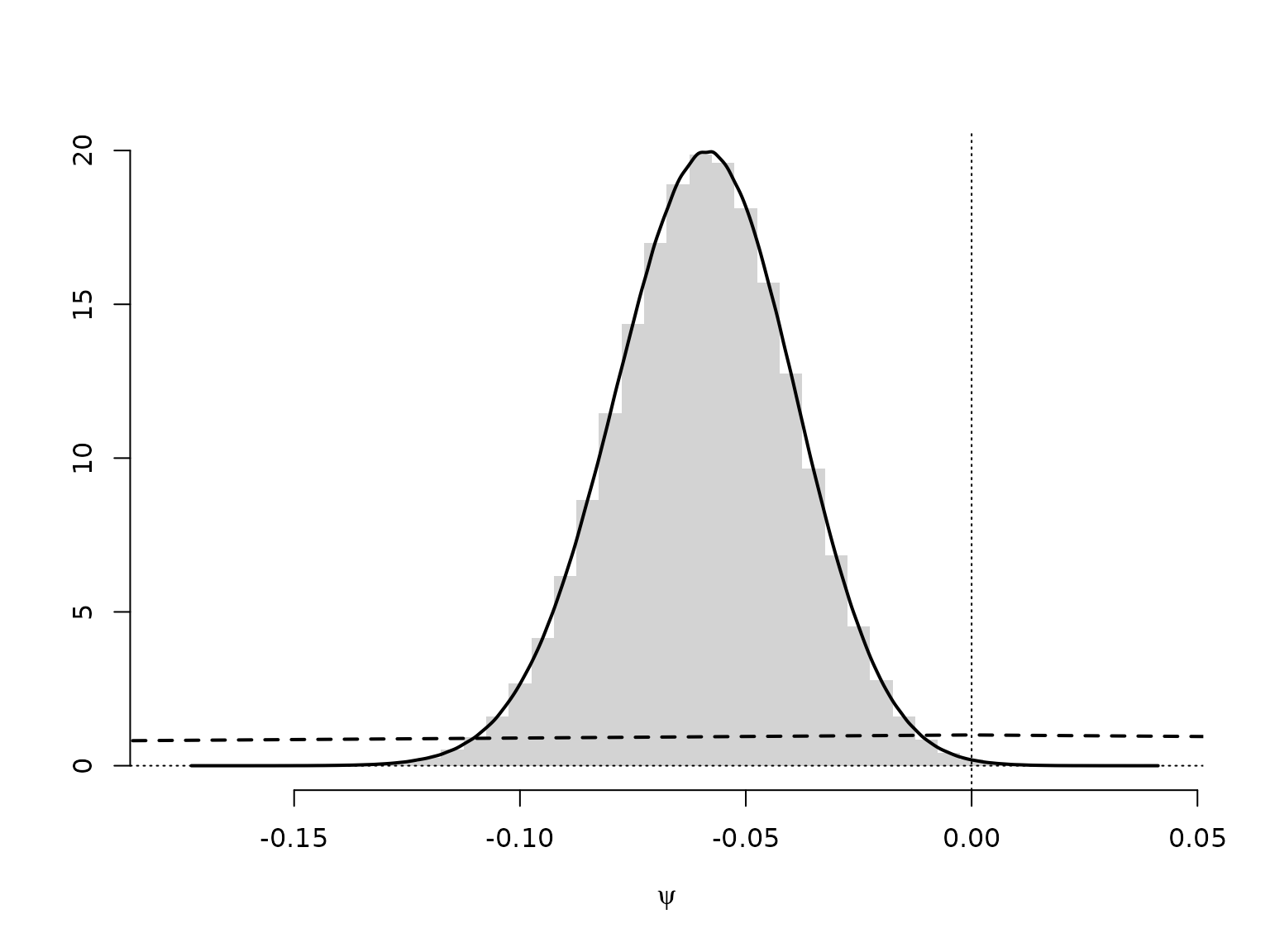

We only need to re-estimate the heterogeneity model which we use to simulate the prior and the posterior of the no-income-risk difference.

par(mar = c(2.5, 1.5, .5, .8), mgp = c(1.6, .6, 0))

set.seed(42)

M <- 10000000

a01 <- a02 <- 1

b01 <- b02 <- 1

N1 <- with(labor, sum(wcollar))

SN1 <- with(labor, sum(wcollar & unemployed))

N2 <- with(labor, sum(!wcollar))

SN2 <- with(labor, sum(!wcollar & unemployed))

aN1 <- a01 + SN1

bN1 <- b01 + N1 - SN1

aN2 <- a02 + SN2

bN2 <- b02 + N2 - SN2

psi <- rbeta(M, aN1, bN1) - rbeta(M, aN2, bN2)

mybreaks <- seq(floor(200 * min(psi)) / 200 - 0.0025,

ceiling(200 * max(psi)) / 200 + 0.0025,

by = 0.005)

hist(psi, breaks = mybreaks, freq = FALSE, xlab = expression(psi),

main = "", ylab = "", border = NA)

lines(c(-1, 0, 1), c(0, 1, 0), lty = 2, lwd = 2)

abline(v = 0, lty = 3)

abline(h = 0, lty = 3)

# Estimate density

lines(d <- density(psi), lwd = 2)

We can approximate the Bayes factor through the estimated Savage-Dickey density ratio. Note, though, that this can be a very poor approximation.

# Evaluate as close a possible to zero (with linear interpolation)

x1 <- sum(d$x < 0) # Find largest x below 0

x2 <- x1 + 1L # Find smallest x above 0

pos <- -d$x[x1] / (d$x[x2] - d$x[x1])

dpost <- (1 - pos) * d$y[x1] + pos * d$y[x2]

# The prior is a symmetric triangular distribution on [-1, 1], thus p(0) = 1

dprior <- 1

(logSD <- log(dpost) - log(dprior))

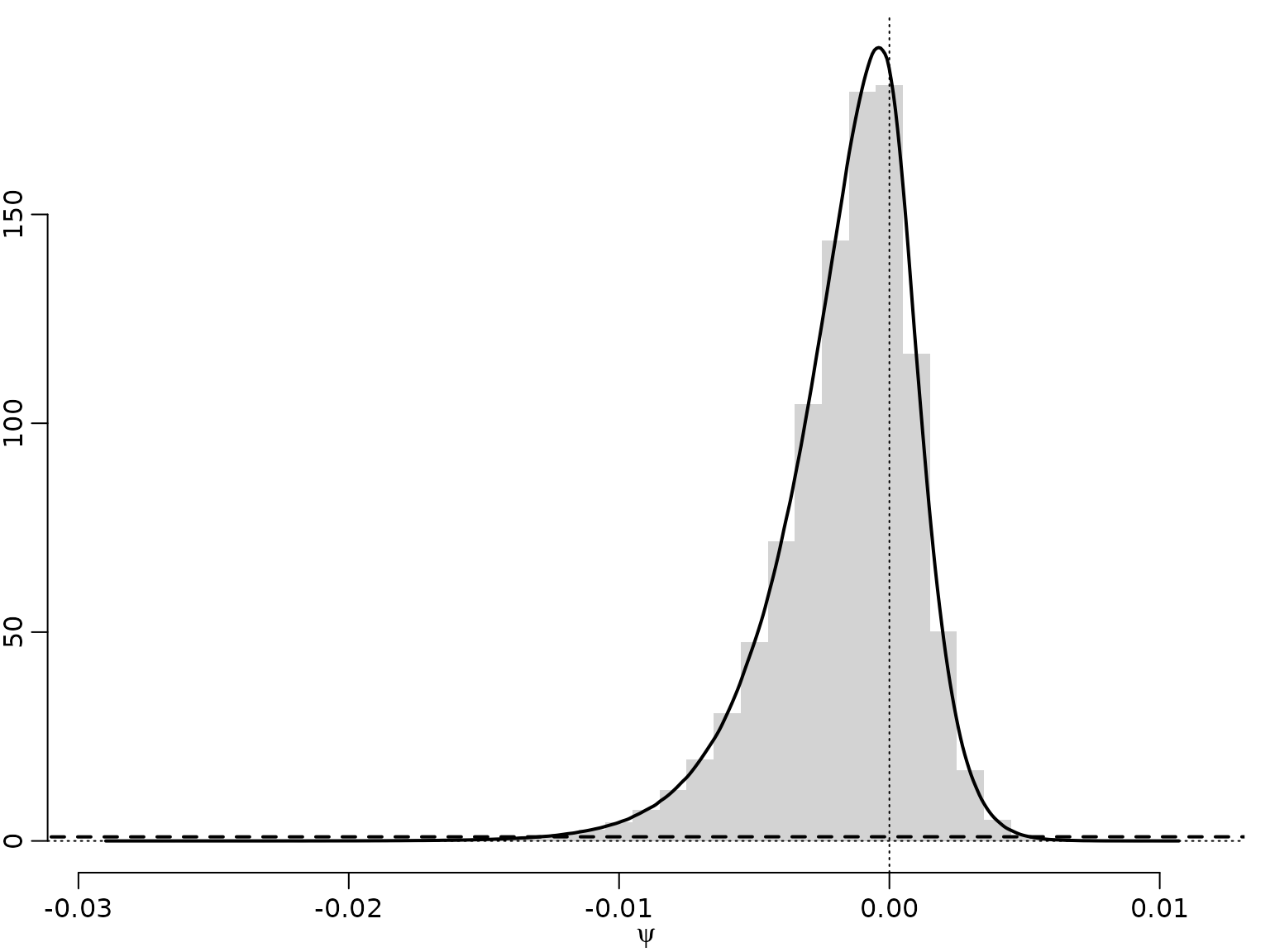

#> [1] -1.657269Example 10.14: Stomach cancer data - Savage-Dickey density ratio for the mortality rate homogeneity test

As above, with different data.

par(mar = c(2.5, 1.5, .5, .8), mgp = c(1.6, .6, 0))

N1 <- 1668 # number at risk in City A

SN1 <- 2 # cancer deaths in City A

N2 <- 583 # number at risk in City B

SN2 <- 1 # cancer deaths in City B

aN1 <- a01 + SN1

bN1 <- b01 + N1 - SN1

aN2 <- a02 + SN2

bN2 <- b02 + N2 - SN2

psi <- rbeta(M, aN1, bN1) - rbeta(M, aN2, bN2)

mybreaks <- seq(floor(1000 * min(psi)) / 1000 - 0.0005,

ceiling(1000 * max(psi)) / 1000 + 0.0005,

by = 0.001)

d <- density(psi)

hist(psi, breaks = mybreaks, freq = FALSE, xlab = expression(psi),

main = "", ylab = "", ylim = c(0, max(d$y)), border = NA)

lines(d, lwd = 2)

lines(c(-1, 0, 1), c(0, 1, 0), lty = 2, lwd = 2)

abline(v = 0, lty = 3)

abline(h = 0, lty = 3)

We can approximate the Bayes factor through the estimated Savage-Dickey density ratio. Note, though, that this can be a very poor approximation.

Section 10.4: Addressing Model Uncertainty

We re-use the marginal likelihoods from above to compute posterior probabilities under a uniform prior for the individual models.

res <- rbind(resM1, resM3)

probs_unnormalized <- exp(res - max(res))

probs <- probs_unnormalized / sum(probs_unnormalized)

knitr::kable(probs, digits = 2)| 1 | 3.52 | 5 | 10 | 20 | |

|---|---|---|---|---|---|

| 0.1 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 0.5 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 0.1 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 0.5 | 0.02 | 0.46 | 0.47 | 0.05 | 0 |

| 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

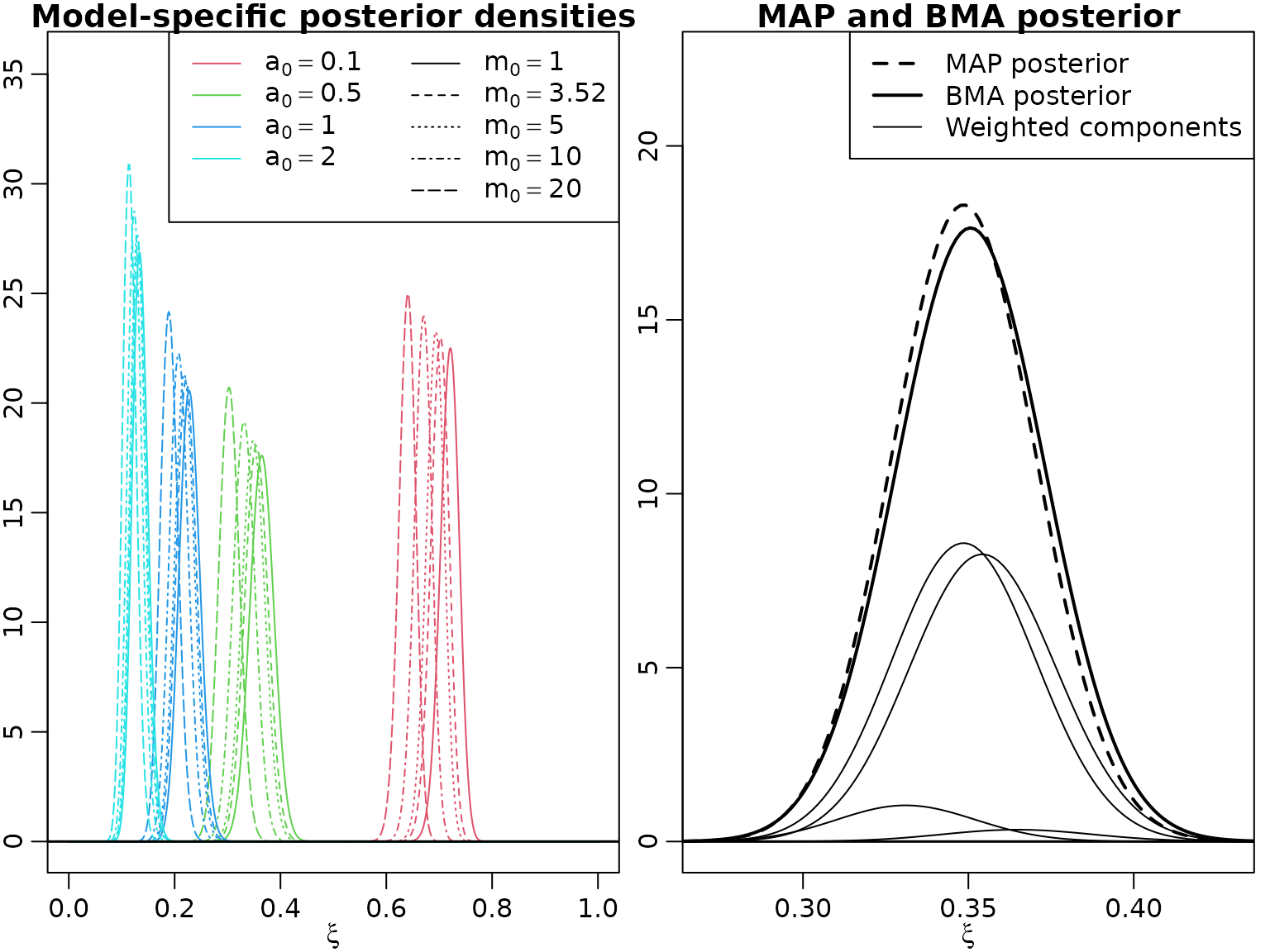

We now evaluate the posteriors for for the different hyperparameter values.

posterior_xi <- function(xi, y, a0, m0, alpha_b0, log = FALSE) {

N <- length(y)

alpha_bN <- alpha_b0 + N * a0

beta_bN <- (alpha_b0 - 1) * m0 / a0 + sum(y)

logdens <- -log(a0) - lbeta(alpha_bN, beta_bN) +

(alpha_bN / a0 - 1) * log(xi) +

(beta_bN - 1) * log(1 - xi^(1 / a0))

if (log) logdens else exp(logdens)

}

xis <- seq(0, 1, length.out = 700)

post_xis <- array(NA_real_,

dim = c(length(a0_tmp), length(m0_tmp), length(xis)),

dimnames = list(a0 = a0_tmp, m0 = round(m0_tmp, 2), xi = xis))

for (i in seq_along(a0_tmp)) {

for (j in seq_along(m0_tmp)) {

post_xis[i, j, ] <- posterior_xi(xis, eyetracking$anomalies,

a0_tmp[i], m0_tmp[j], 6)

}

}Now we visualize, first the individual (model-specific) posteriors, then the BMA density and (again) the one for the model with highest posterior probability.

plot(NULL, xlim = c(0, 1), ylim = c(0, 1.15 * max(post_xis)),

xlab = expression(xi), ylab = "",

main = "Model-specific posterior densities")

legend("topright", ncol = 2,

legend = parse(text = c(paste("a[0] == ", a0_tmp), '""',

paste("m[0] == ", round(m0_tmp, 2)))),

lty = c(rep(1, length(a0_tmp)), NA, seq_along(m0_tmp)),

col = c(seq_along(a0_tmp) + 1, NA, rep(1, length(m0_tmp))))

for (i in seq_along(a0_tmp)) {

for (j in seq_along(m0_tmp)) {

lines(xis, post_xis[i, j, ], col = i + 1, lty = j)

}

}

abline(h = 0, lwd = 1.5)

weighted_post_xis <- as.numeric(probs[5:8, ]) * post_xis

bma_post_xis <- apply(weighted_post_xis, 3, sum)

argmax <- which(probs[5:8, ] == max(probs[5:8, ]), arr.ind = TRUE)

plot(xis, post_xis[argmax[1, 1], argmax[1, 2], ], type = "l", lwd = 2,

xlim = c(0.27, 0.43),

ylim = c(0, 1.17 * max(post_xis[probs[5:8, ] > 0.0001])),

lty = 2, main = "MAP and BMA posterior", xlab = expression(xi))

lines(xis, bma_post_xis, lwd = 2)

for (i in seq_len(nrow(weighted_post_xis))) {

for (j in seq_len(ncol(weighted_post_xis))) {

if (probs[4 + i, j] > 0.0001) {

lines(xis, weighted_post_xis[i,j, ])

}

}

}

legend("topright", c("MAP posterior", "BMA posterior",

"Weighted components"),

col = 1, lty = c(2, 1, 1), lwd = c(2, 2, 1))

abline(h = 0, lwd = 1.5)

Let us compute the posterior mean for the most probable model and the BMA mean.

posterior_mean_xi <- function(y, a0, m0, alpha_b0) {

N <- length(y)

alpha_bN <- alpha_b0 + N * a0

beta_bN <- (alpha_b0 - 1) * m0 / a0 + sum(y)

logmean <- lbeta(alpha_bN + a0, beta_bN) - lbeta(alpha_bN, beta_bN)

exp(logmean)

}

grid <- expand.grid(a0 = a0_tmp, m0 = m0_tmp)

post_means <- posterior_mean_xi(eyetracking$anomalies, grid$a0, grid$m0, 6)

(bms_mean <- post_means[which.max(probs[5:8, ])])

#> [1] 0.3488389

(bma_mean <- sum(probs[5:8, ] * post_means))

#> [1] 0.3508087