Chapter 7: Introduction to Bayesian Time Series Analysis

Chapter07.RmdSection 7.2: Bayesian Learning of (Stationary) Autoregressive Models

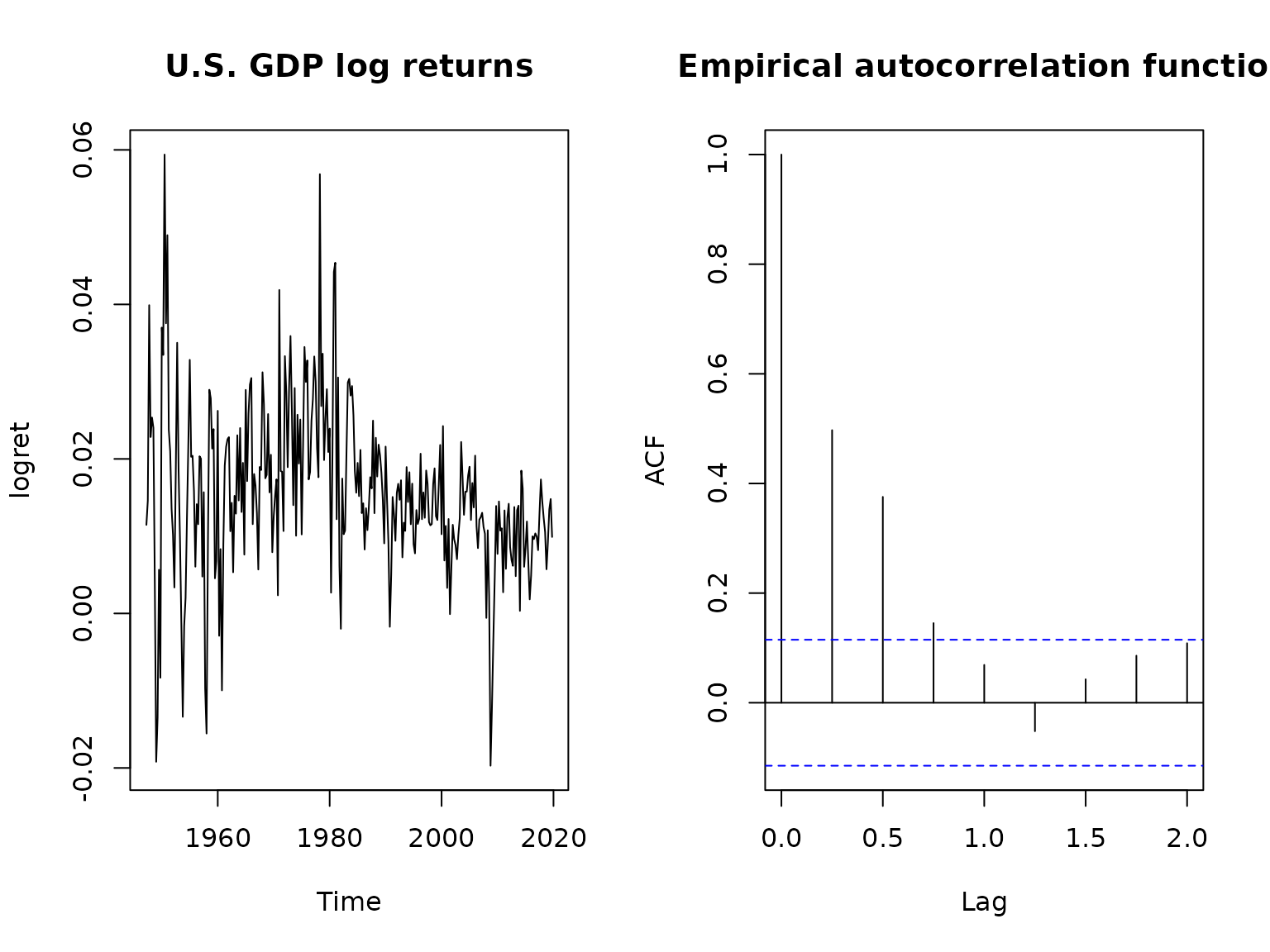

Figure 7.1: U.S. GDP data

First, we load the data. Because of the extreme outliers during the COVID pandemic, we restrict our analysis to the time before its outbreak.

Next, we compute the log returns.

logret <- log(dat[-1]) - log(dat[-length(dat)])

logret <- ts(logret, start = c(1947, 2), end = c(2019, 4),

frequency = 4)Now we can plot the data and its empirical autocorrelation function.

ts.plot(logret, main = "U.S. GDP log returns")

acf(logret, lag = 8, main = "")

title("Empirical autocorrelation function")

Before we move on, we define a function yielding posterior draws under a standard regression model, using the tools developed in Chapter 6.

library("BayesianLearningCode")

library("mvtnorm")

regression <- function(y, X, prior = "improper", b0 = 0, B0 = 1, c0 = 0.01,

C0 = 0.01, nburn = 1000L, M = 10000L) {

N <- nrow(X)

d <- ncol(X)

if (length(b0) == 1L) b0 <- rep(b0, d)

if (!is.matrix(B0)) {

if (length(B0) == 1L) {

B0 <- diag(rep(B0, d))

} else {

B0 <- diag(B0)

}

}

if (prior == "improper") {

fit <- lm.fit(X, y)

betahat <- fit$coefficients

SSR <- sum(fit$residuals^2)

cN <- (N - d) / 2

CN <- SSR / 2

bN <- betahat

BN <- solve(crossprod(X))

sigma2s <- rinvgamma(M, cN, CN)

betas <- matrix(NA_real_, M, d)

for (i in seq_len(M)) betas[i, ] <- rmvnorm(1, bN, sigma2s[i] * BN)

} else if (prior == "conjugate") {

B0inv <- solve(B0)

BNinv <- B0inv + crossprod(X)

BN <- solve(BNinv)

bN <- BN %*% (B0inv %*% b0 + crossprod(X, y))

Seps0 <- crossprod(y) + crossprod(b0, B0inv) %*% b0 -

crossprod(bN, BNinv) %*% bN

cN <- c0 + N / 2

CN <- C0 + Seps0 / 2

sigma2s <- rinvgamma(M, cN, CN)

betas <- matrix(NA_real_, M, d)

for (i in seq_len(M)) betas[i, ] <- rmvnorm(1, bN, sigma2s[i] * BN)

} else if (prior == "semi-conjugate") {

# Precompute some values

B0inv <- solve(B0)

B0invb0 <- B0inv %*% b0

cN <- c0 + N / 2

XX <- crossprod(X)

Xy <- crossprod(X, y)

# Prepare memory to store the draws

betas <- matrix(NA_real_, nrow = M, ncol = d)

sigma2s <- rep(NA_real_, M)

colnames(betas) <- colnames(X)

# Set the starting value for sigma2

sigma2 <- var(y) / 2

# Run the Gibbs sampler

for (m in seq_len(nburn + M)) {

# Sample beta from its full conditional

BN <- solve(B0inv + XX / sigma2)

bN <- BN %*% (B0invb0 + Xy / sigma2)

beta <- rmvnorm(1, mean = bN, sigma = BN)

# Sample sigma^2 from its full conditional

eps <- y - tcrossprod(X, beta)

CN <- C0 + crossprod(eps) / 2

sigma2 <- rinvgamma(1, cN, CN)

# Store the results

if (m > nburn) {

betas[m - nburn, ] <- beta

sigma2s[m - nburn] <- sigma2

}

}

}

list(betas = betas, sigma2s = sigma2s)

}Now we are ready to reproduce the results in the book.

Example 7.1: AR modeling of the U.S. GDP data

We begin by writing a function that sets up the design matrix for an AR() model.

ARdesignmatrix <- function(dat, p = 1) {

d <- p + 1

N <- length(dat) - p

Xy <- matrix(NA_real_, N, d)

Xy[, 1] <- 1

for (i in seq_len(p)) {

Xy[, i + 1] <- dat[(p + 1 - i) : (length(dat) - i)]

}

Xy

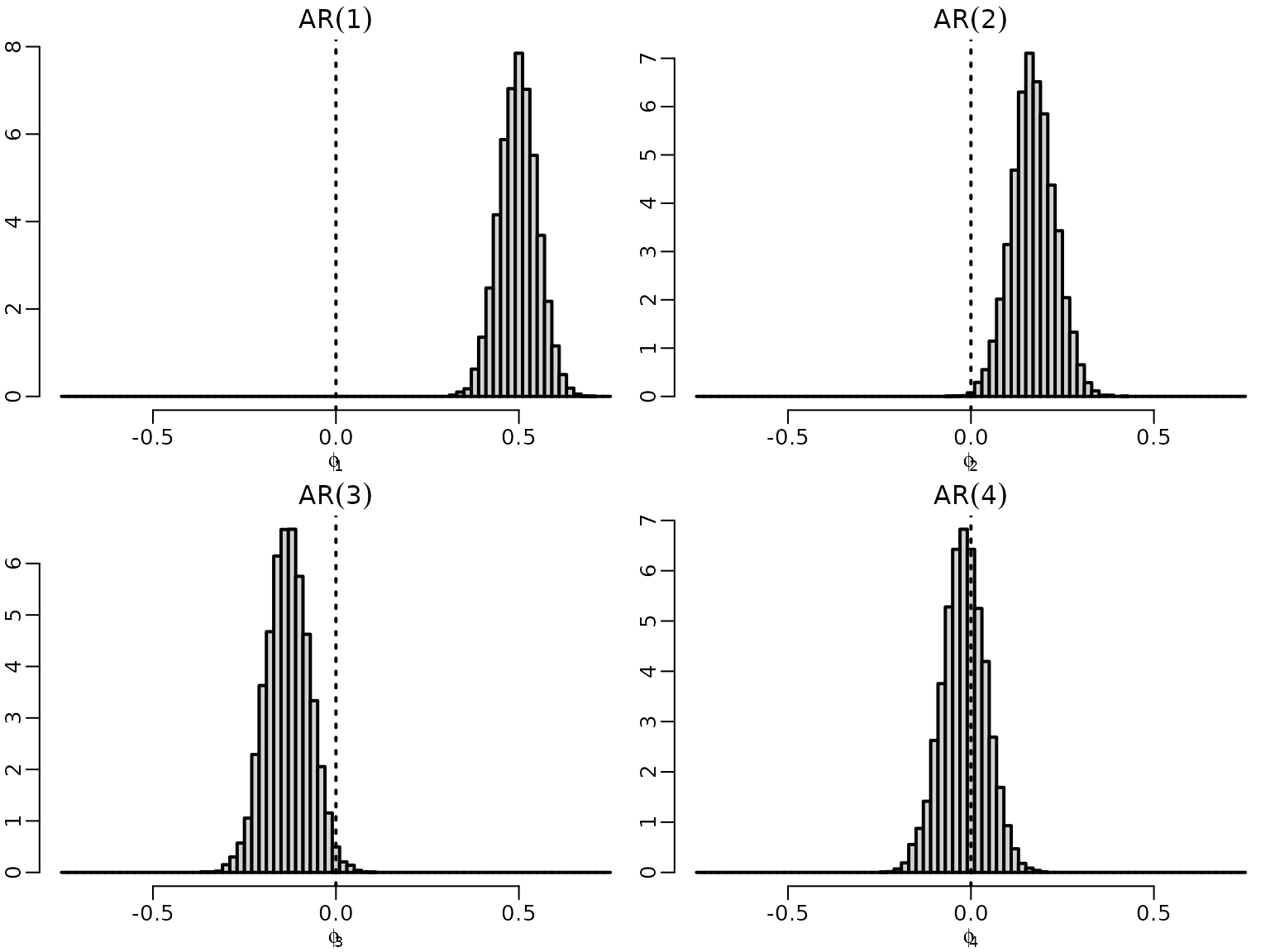

}We obtain draws for four AR models under the improper prior.

Figure 7.2: Exploratory model selection

Now we plot the draws for the leading coefficient, i.e., the coefficient corresponding to the highest lag in each of the models.

for (p in 1:4) {

hist(res[[p]]$betas[, p + 1], freq = FALSE, main = bquote(AR(.(p))),

xlab = bquote(phi[.(p)]), ylab = "", breaks = seq(-.75, .75, .02))

abline(v = 0, lty = 3)

}

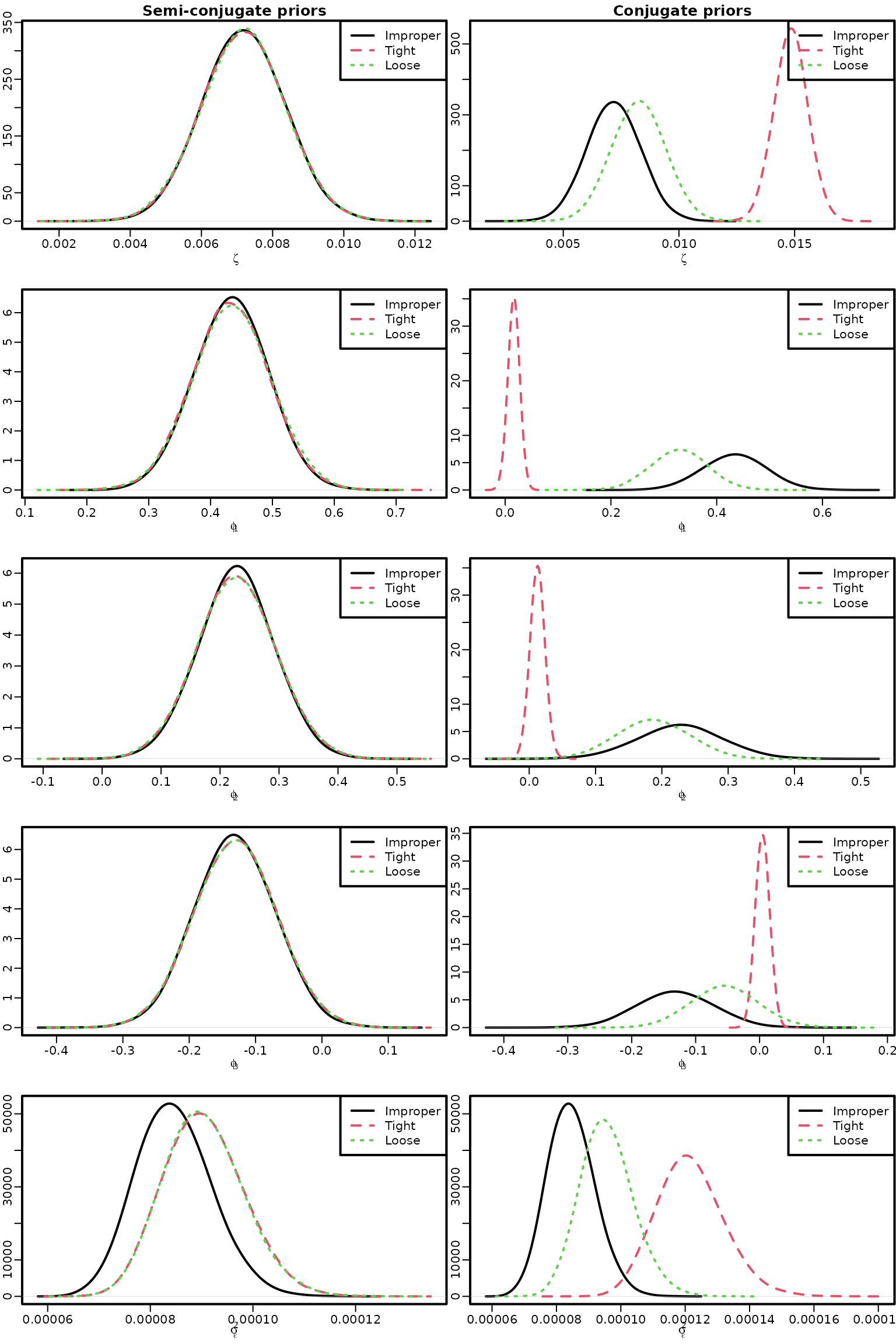

Next, we fit an AR(3) model with different priors.

y <- tail(logret, -3)

Xy <- ARdesignmatrix(logret, 3)

res_improper <- res[[3]]

res_conj_1 <- regression(y, Xy, prior = "conjugate",

b0 = rep(0, 4), B0 = diag(rep(1, 4)),

c0 = 2, C0 = 0.001)

res_semi_1 <- regression(y, Xy, prior = "semi-conjugate",

b0 = rep(0, 4), B0 = diag(rep(1, 4)),

c0 = 2, C0 = 0.001)

res_conj_2 <- regression(y, Xy, prior = "conjugate",

b0 = rep(0, 4), B0 = diag(rep(100, 4)),

c0 = 2, C0 = 0.001)

res_semi_2 <- regression(y, Xy, prior = "semi-conjugate",

b0 = rep(0, 4), B0 = diag(rep(100, 4)),

c0 = 2, C0 = 0.001)Figure 7.3: AR(3) models with improper, semi-conjugate, and conjugate priors

We now visualize the posterior of the model parameters under all those priors.

for (i in 1:5) {

if (i <= 4) {

if (i == 1) name <- bquote(zeta) else name <- bquote(phi[.(i - 1)])

dens_improper <- density(res_improper$betas[, i], bw = "SJ", adj = 2)

dens_semi_1 <- density(res_semi_1$betas[, i], bw = "SJ", adj = 2)

dens_semi_2 <- density(res_semi_2$betas[, i], bw = "SJ", adj = 2)

dens_conj_1 <- density(res_conj_1$betas[, i], bw = "SJ", adj = 2)

dens_conj_2 <- density(res_conj_2$betas[, i], bw = "SJ", adj = 2)

} else {

name <- bquote(sigma[epsilon]^2)

dens_improper <- density(res_improper$sigma2, bw = "SJ", adj = 2)

dens_semi_1 <- density(res_semi_1$sigma2, bw = "SJ", adj = 2)

dens_semi_2 <- density(res_semi_2$sigma2, bw = "SJ", adj = 2)

dens_conj_1 <- density(res_conj_1$sigma2, bw = "SJ", adj = 2)

dens_conj_2 <- density(res_conj_2$sigma2, bw = "SJ", adj = 2)

}

plot(dens_improper, main = "", xlab = name, ylab = "",

xlim = range(dens_improper$x, dens_semi_1$x, dens_semi_2$x),

ylim = range(dens_improper$y, dens_semi_1$y, dens_semi_2$y))

if (i == 1) title("Semi-conjugate priors")

lines(dens_semi_1, col = 2, lty = 2)

lines(dens_semi_2, col = 3, lty = 3)

legend("topright", c("Improper", "Tight", "Loose"), col = 1:3, lty = 1:3)

plot(dens_improper, main = "", xlab = name, ylab = "",

xlim = range(dens_improper$x, dens_conj_1$x, dens_conj_2$x),

ylim = range(dens_improper$y, dens_conj_1$y, dens_conj_2$y))

if (i == 1) title("Conjugate priors")

lines(dens_conj_1, col = 2, lty = 2)

lines(dens_conj_2, col = 3, lty = 3)

legend("topright", c("Improper", "Tight", "Loose"), col = 1:3, lty = 1:3)

}

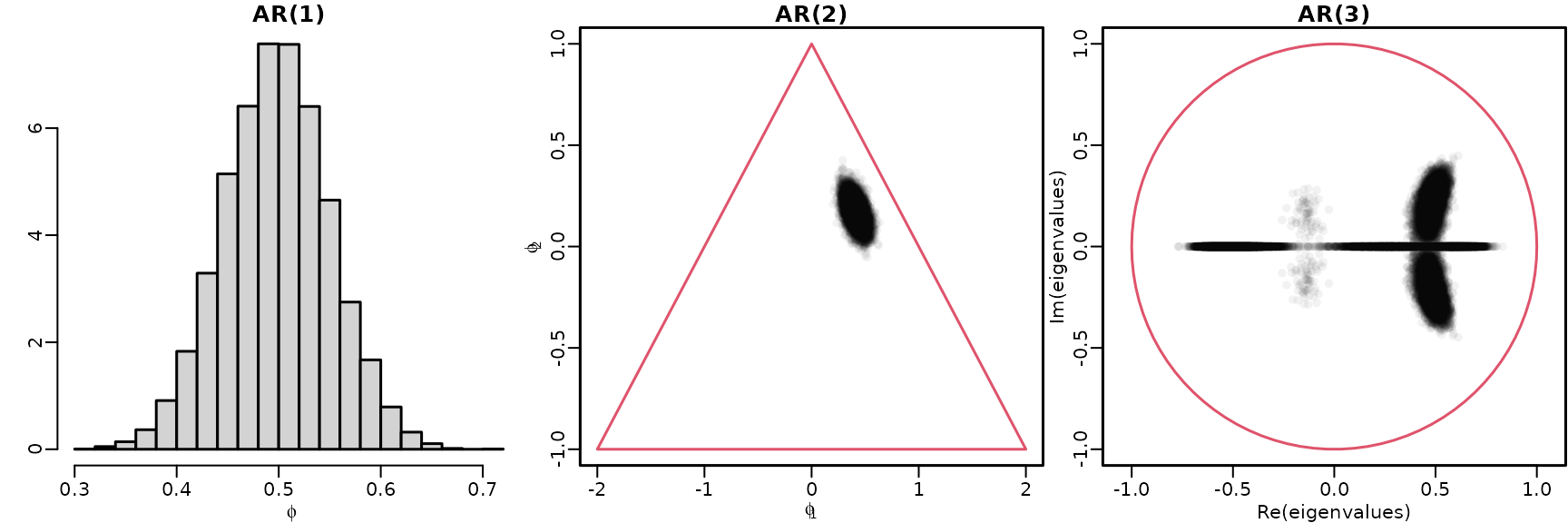

Section 7.2.2: Exploring stationarity during post-processing

We reuse the AR() models under the improper prior from above to explore stationarity for .

Figure 7.4: Checking stationarity conditions for the GDP data

hist(res[[1]]$betas[, 2], breaks = 20, freq = FALSE, main = "AR(1)",

xlab = bquote(phi), ylab = "")

plot(res[[2]]$betas[, 2:3], main = "AR(2)", xlab = bquote(phi[1]),

ylab = bquote(phi[2]), xlim = c(-2, 2), ylim = c(-1, 1),

col = rgb(0, 0, 0, .05), pch = 16)

polygon(c(-2, 0, 2, -2), c(-1, 1, -1, -1), border = 2)

draws <- res[[3]]$betas[, 2:4]

eigenvalues <- matrix(NA_complex_, nrow(draws), ncol(draws))

for (m in seq_len(nrow(draws))) {

Phi <- matrix(c(draws[m, ], c(1, 0, 0), c(0, 1, 0)), byrow = TRUE, nrow = 3)

eigenvalues[m, ] <- eigen(Phi, only.values = TRUE)$values

}

plot(eigenvalues, xlim = c(-1, 1), ylim = c(-1, 1), asp = 1,

main = "AR(3)", col = rgb(0, 0, 0, .05), pch = 16)

symbols(0, 0, 1, add = TRUE, fg = 2, inches = FALSE)

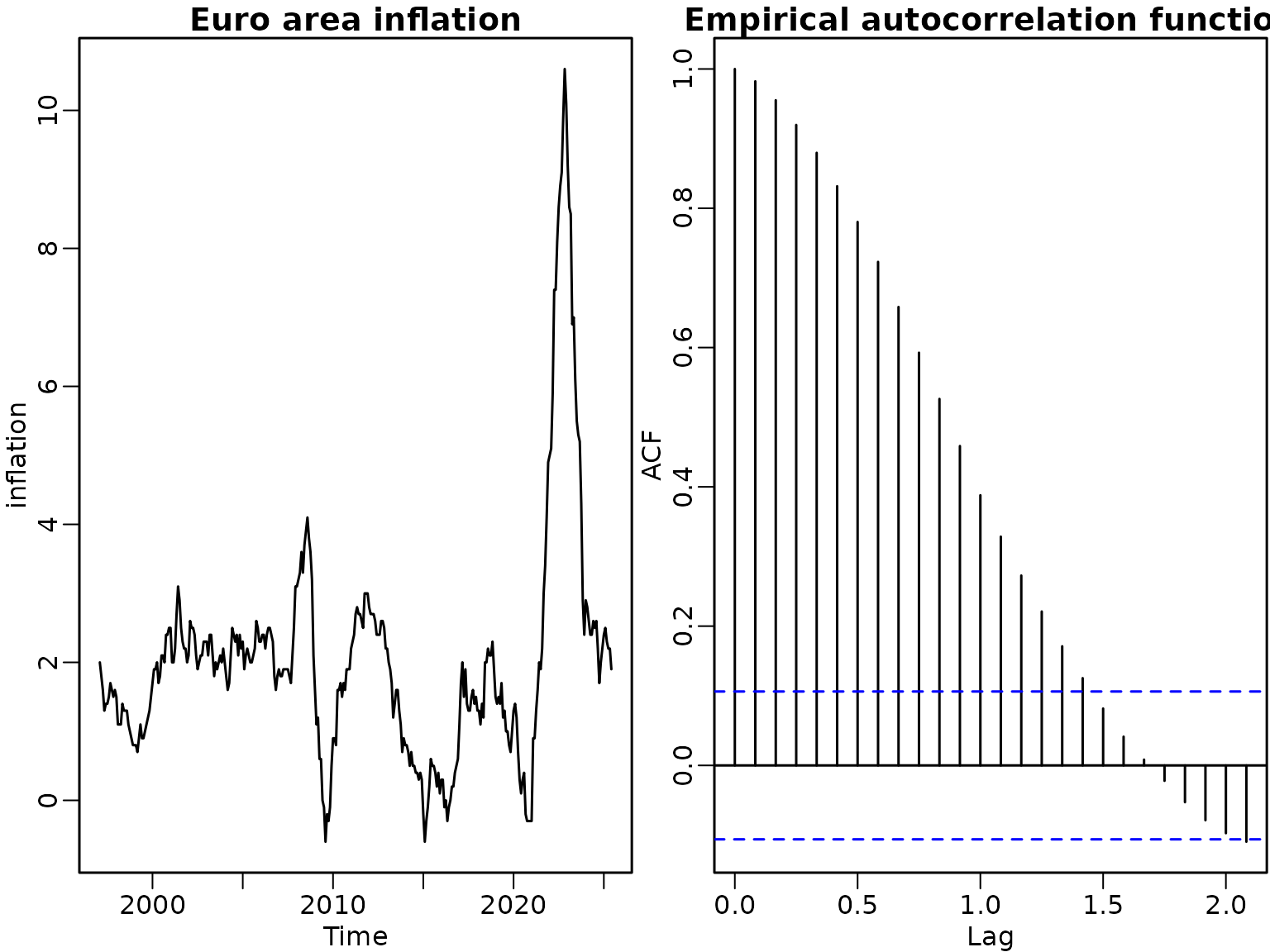

We now move towards analyzing the Euro area inflation data.

data("inflation", package = "BayesianLearningCode")

inflation <- ts(inflation, start = c(1997, 2), end = c(2025, 6),

frequency = 12)First, we plot the data and its empirical autocorrelation function.

Figure 7.5: Euro area inflation data

ts.plot(inflation, main = "Euro area inflation")

acf(inflation, main = "")

title("Empirical autocorrelation function")

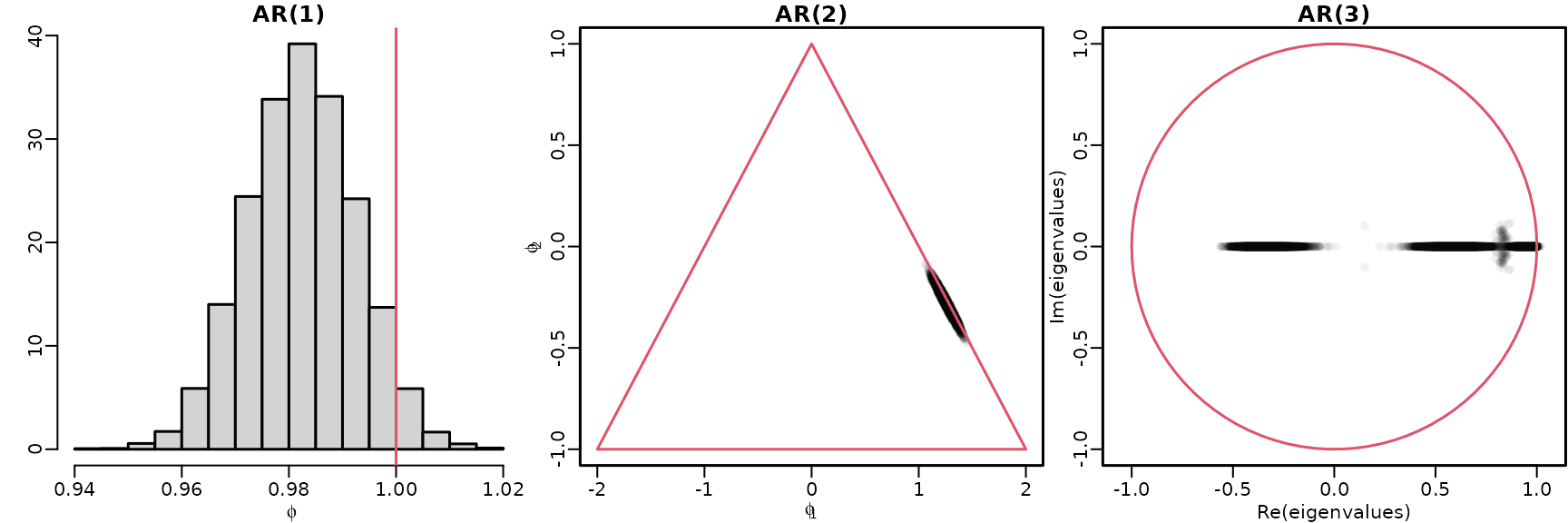

We fit AR() models under the improper prior to explore stationarity for .

Figure 7.6: Checking stationarity conditions for the Euro area inflation data

ar1draws <- res2[[1]]$betas[, 2]

ar2draws <- res2[[2]]$betas[, 2:3]

ar3draws <- res2[[3]]$betas[, 2:4]

hist(ar1draws, breaks = 20, freq = FALSE, main = "AR(1)",

xlab = bquote(phi), ylab = "")

abline(v = 1, col = 2)

plot(ar2draws, main = "AR(2)", xlab = bquote(phi[1]),

ylab = bquote(phi[2]), xlim = c(-2, 2), ylim = c(-1, 1),

col = rgb(0, 0, 0, .05), pch = 16)

polygon(c(-2, 0, 2, -2), c(-1, 1, -1, -1), border = 2)

eigenvalues <- matrix(NA_complex_, nrow(ar3draws), ncol(ar3draws))

for (m in seq_len(nrow(ar3draws))) {

Phi <- matrix(c(ar3draws[m, ], c(1, 0, 0), c(0, 1, 0)), byrow = TRUE, nrow = 3)

eigenvalues[m, ] <- eigen(Phi, only.values = TRUE)$values

}

plot(eigenvalues, xlim = c(-1, 1), ylim = c(-1, 1), asp = 1,

main = "AR(3)", col = rgb(0, 0, 0, .05), pch = 16)

symbols(0, 0, 1, add = TRUE, fg = 2, inches = FALSE)

To assess the probability of nonstationarity, we can simply count the draws outside of the stationarity region.

nonstationary <- matrix(NA, nrow(ar3draws), 3,

dimnames = list(NULL, order = 1:3))

nonstationary[, 1] <- abs(ar1draws) > 1

nonstationary[, 2] <- ar2draws[, 1] + ar2draws[, 2] > 1 |

abs(ar2draws[, 2]) > 1 |

ar2draws[, 2] > 1 + ar2draws[, 1]

nonstationary[, 3] <- apply(Mod(eigenvalues) > 1, 1, any)

colMeans(nonstationary)

#> 1 2 3

#> 0.0408 0.0107 0.0032Section 7.2.3: Recovering Missing Time Series Data – An Introduction to Data Augmentation

Assume that the values at certain time points are missing. (Note that for our sampler, we require the missing time points to be far enough apart. This restriction is not substantial, though.)

missing <- seq(10, 100, by = 10)

yaug <- logret

yaug[missing] <- NA_real_To set up the Gibbs sampler, we need starting values for . Here, we interpolate linearly (take the average of the adjacent values).

For simplicity, we employ our improper prior and sample iteratively.

ndraws <- 10000

nburn <- 1000

ind <- missing - 2

ytilde <- rep(NA_real_, 3)

betas <- matrix(NA_real_, ndraws, 3)

sigma2s <- rep(NA_real_, ndraws)

ymisses <- matrix(NA_real_, ndraws, length(ind))

for (m in seq_len(ndraws + nburn)) {

# Augment the observed time series with the missing values

yaug[missing] <- ymiss

# Sample the parameters conditional on the augmented data

Xy <- ARdesignmatrix(yaug, 2)

y <- tail(yaug, -2)

N <- nrow(Xy)

d <- ncol(Xy)

BN <- solve(crossprod(Xy))

bN <- BN %*% crossprod(Xy, y)

cN <- (N - d) / 2

CN <- sum((y - Xy %*% bN)^2) / 2

sigma2 <- rinvgamma(1, cN, CN)

beta <- rmvnorm(1, bN, sigma2 * BN)

zeta <- beta[1]

phi <- beta[2:3]

# Sample the missing values conditional on the parameters

for (i in seq_along(ind)) {

ytilde[1] <- -zeta - phi[1] * y[ind[i] - 1] - phi[2] * y[ind[i] - 2]

ytilde[2] <- -zeta + y[ind[i] + 1] - phi[2] * y[ind[i] - 1]

ytilde[3] <- -zeta + y[ind[i] + 2] - phi[1] * y[ind[i] + 1]

X <- matrix(c(-1, phi), nrow = 3)

BN <- solve(crossprod(X))

bN <- BN %*% crossprod(X, ytilde)

ymiss[i] <- rmvnorm(1, bN, sigma2 * BN)

}

# Store the results

if (m > nburn) {

betas[m - nburn, ] <- beta

sigma2s[m - nburn] <- sigma2

ymisses[m - nburn, ] <- ymiss

}

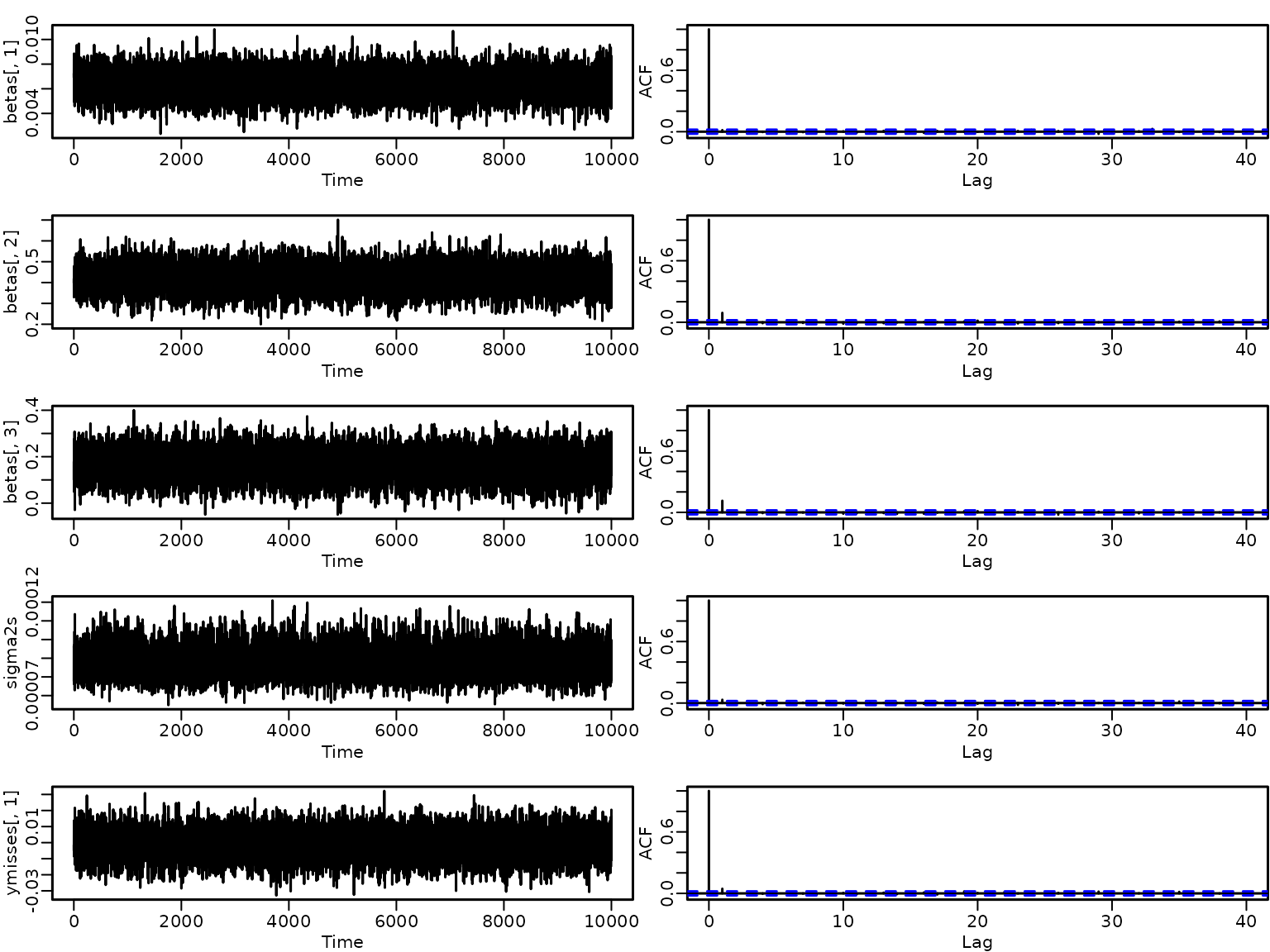

}Let us briefly check some trace plots and ACFs of the draws.

par(mfrow = c(5, 2))

ts.plot(betas[, 1])

acf(betas[, 1])

ts.plot(betas[, 2])

acf(betas[, 2])

ts.plot(betas[, 3])

acf(betas[, 3])

ts.plot(sigma2s)

acf(sigma2s)

ts.plot(ymisses[, 1])

acf(ymisses[, 1])

Seems like the mixing is perfect and there is no cause for concern.

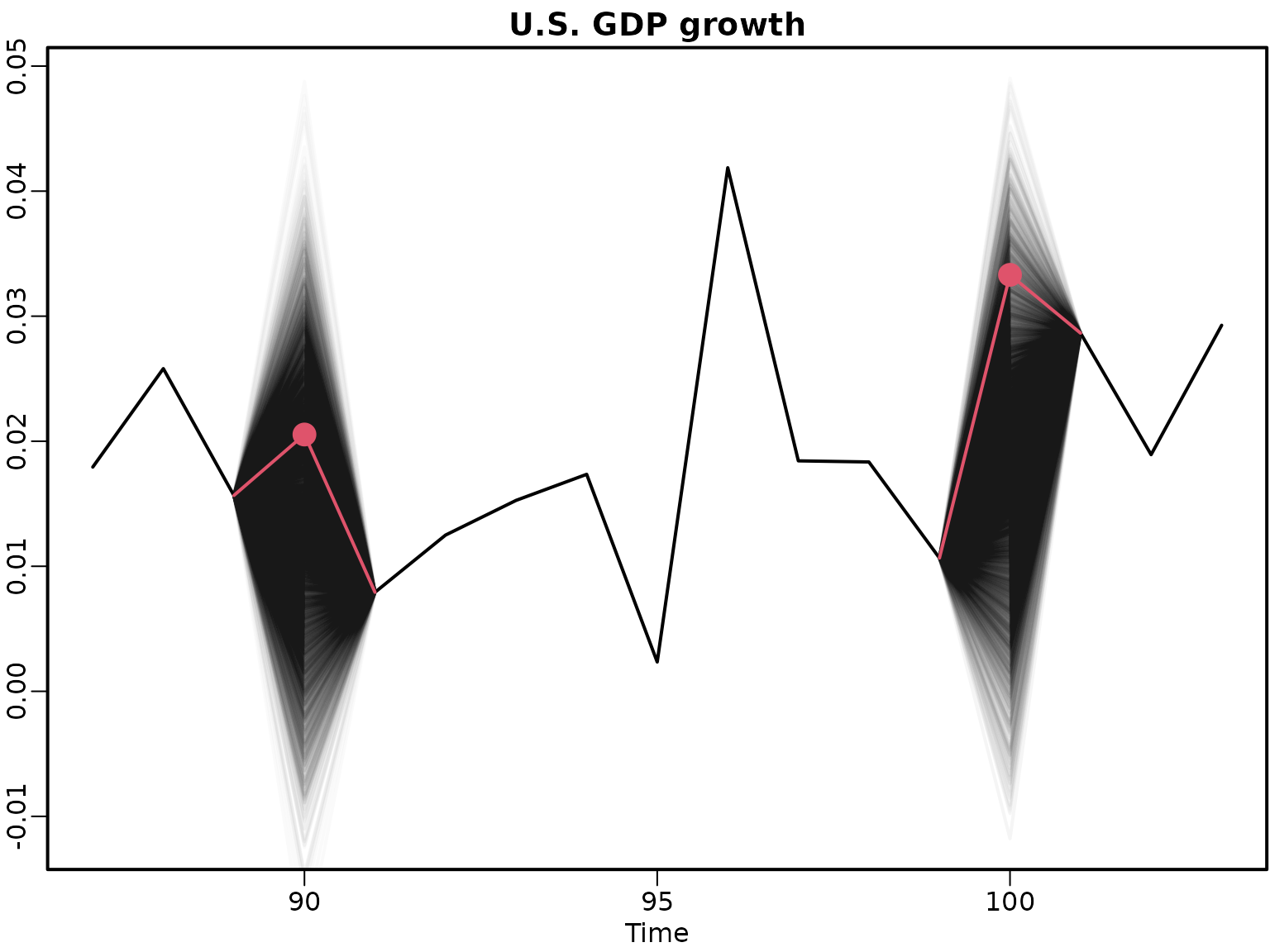

We move on to visualizing the observed and the missing values (black lines), alongside the unobservable true values (red circles).

yaug[missing] <- NA

where <- seq(max(missing) - 13, max(missing) + 3)

plot(where, yaug[where], type = "l", ylim = range(ymisses[, i]),

xlab = "Time", ylab = "", main = "U.S. GDP growth")

for (i in seq_along(missing)) {

for (j in seq_len(nrow(ymisses))) {

lines(c(missing[i] - 1, missing[i], missing[i] + 1),

c(yaug[missing[i] - 1], ymisses[j, i], yaug[missing[i] + 1]),

col = rgb(0, 0, 0, .02))

}

points(missing[i], logret[missing[i]], col = 2, cex = 2, pch = 16)

lines(c(missing[i] - 1, missing[i], missing[i] + 1),

c(yaug[missing[i] - 1], logret[missing[i]], yaug[missing[i] + 1]),

col = 2, cex = 2)

}

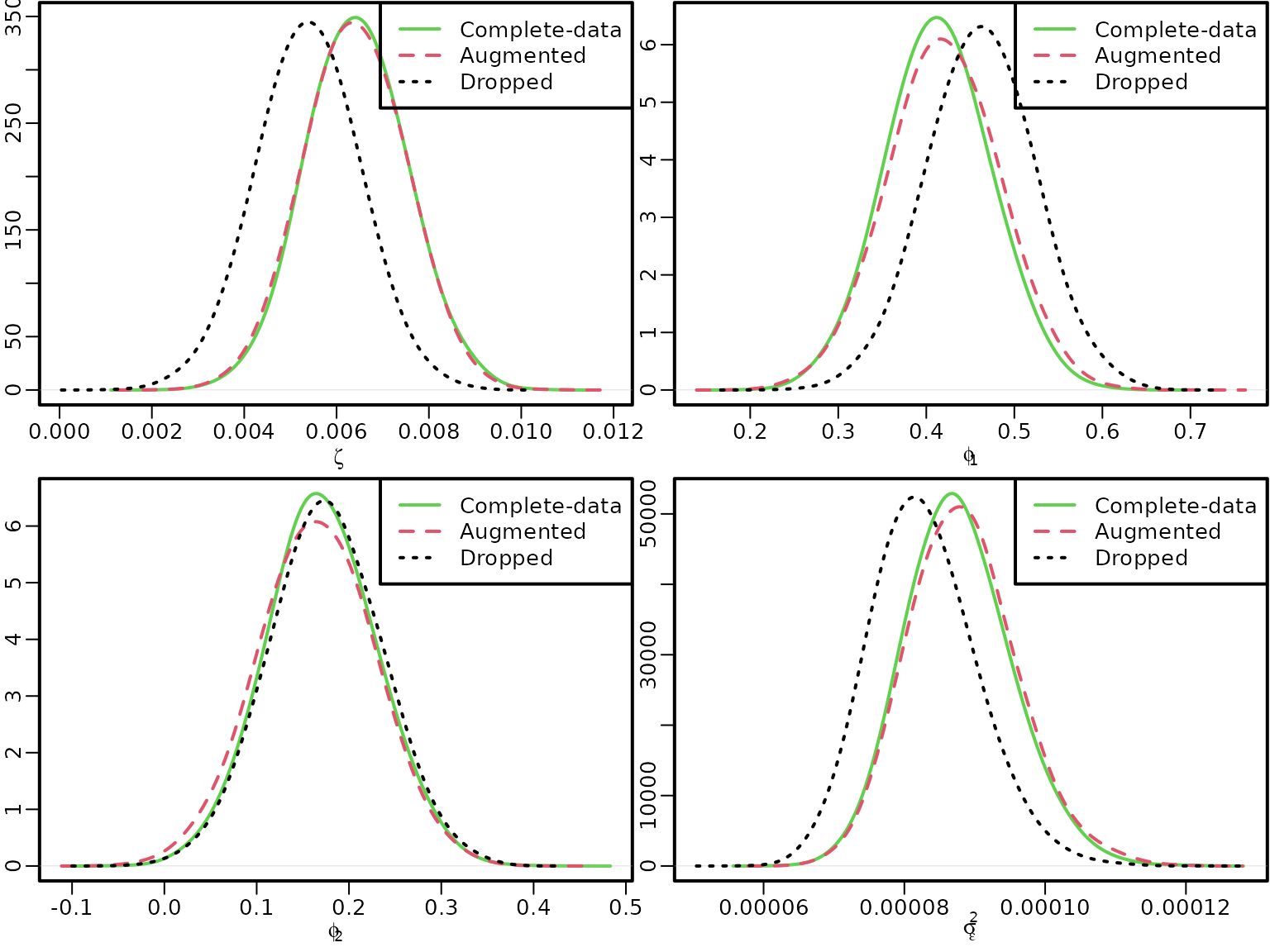

Now let us compare the parameter estimates with the complete-data posterior and the posterior arising when missing values are ignored.

We start by estimating a model where all equations containing missing data are simply dropped.

Xy <- ARdesignmatrix(yaug, 2)

y <- tail(yaug, -2)

containsNA <- apply(is.na(cbind(y, Xy)), 1, any)

yred <- y[!containsNA]

Xyred <- Xy[!containsNA, ]

res_drop <- regression(yred, Xyred, prior = "improper")Now we can plot.

for (i in 1:4) {

if (i <= 3) {

if (i == 1) name <- bquote(zeta) else name <- bquote(phi[.(i - 1)])

dens_improper <- density(res[[2]]$betas[, i], bw = "SJ", adj = 2)

dens_drop <- density(res_drop$betas[, i], bw = "SJ", adj = 2)

dens_aug <- density(betas[, i], bw = "SJ", adj = 2)

} else {

name <- bquote(sigma[epsilon]^2)

dens_improper <- density(res[[2]]$sigma2, bw = "SJ", adj = 2)

dens_drop <- density(res_drop$sigma2, bw = "SJ", adj = 2)

dens_aug <- density(sigma2s, bw = "SJ", adj = 2)

}

plot(dens_improper, xlim = range(dens_improper$x, dens_drop$x, dens_aug$x),

ylim = range(dens_improper$y, dens_drop$y, dens_aug$y),

main = "", xlab = name, ylab = "", col = 3)

lines(dens_aug, col = 2, lty = 2)

lines(dens_drop, lty = 3)

legend("topright", c("Complete-data", "Augmented", "Dropped"),

col = 3:1, lty = 1:3)

}

Section 7.2.4: Imposing Stationarity via an Independence MH Algorithm

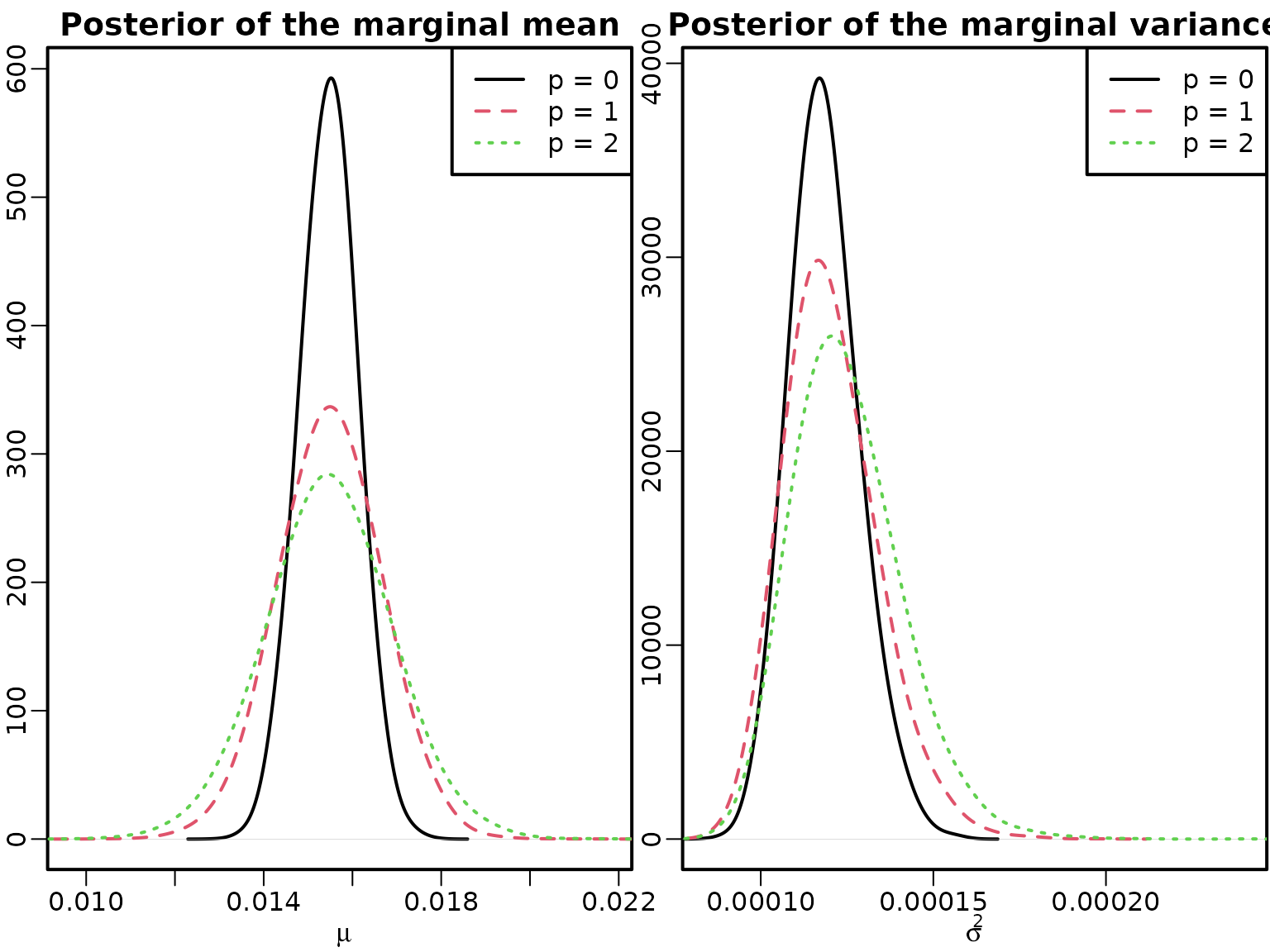

First, we fit an AR(0), i.e., an intercept-only, model, to the GDP data.

Xy <- ARdesignmatrix(logret, 0) # Fill the N x 1 design matrix with 1s

res0 <- regression(logret, Xy, prior = "improper")We now create Figure 7.9 via simple transformations.

mu <- sigma2 <- matrix(NA_real_, ndraws, 3, dimnames = list(NULL, order = 0:2))

mu[, "0"] <- res0$betas[, 1]

sigma2[, "0"] <- res0$sigma2s

for (p in 1:2) {

mu[, as.character(p)] <- res[[p]]$betas[, 1] /

(1 - rowSums(res[[p]]$betas[, 2:(p + 1), drop = FALSE]))

}

# AR(1):

phi <- res[[1]]$betas[, 2]

sigma2[, "1"] <- res[[1]]$sigma2s / (1 - phi^2)

# AR(2):

phi1 <- res[[2]]$betas[, 2]

phi2 <- res[[2]]$betas[, 3]

sigma2[, "2"] <- (1 - phi2) * res[[1]]$sigma2s /

((1 + phi2) * (1 - phi1^2 + phi2^2 - 2 * phi2))

plot(density(mu[, "0"], bw = "SJ", adj = 2), xlim = range(mu), ylab = "",

main = "Posterior of the marginal mean", xlab = expression(mu))

for (p in 1:2) lines(density(mu[, as.character(p)], bw = "SJ", adj = 2),

col = p + 1, lty = p + 1)

legend("topright", paste0("p = ", 0:2), col = 1:3, lty = 1:3)

plot(density(sigma2[, "0"], bw = "SJ", adj = 2), xlim = range(sigma2),

xlab = expression(sigma^2), ylab = "",

main = "Posterior of the marginal variance")

for (p in 1:2) lines(density(sigma2[, as.character(p)], bw = "SJ", adj = 2),

col = p + 1, lty = p + 1)

legend("topright", paste0("p = ", 0:2), col = 1:3, lty = 1:3)

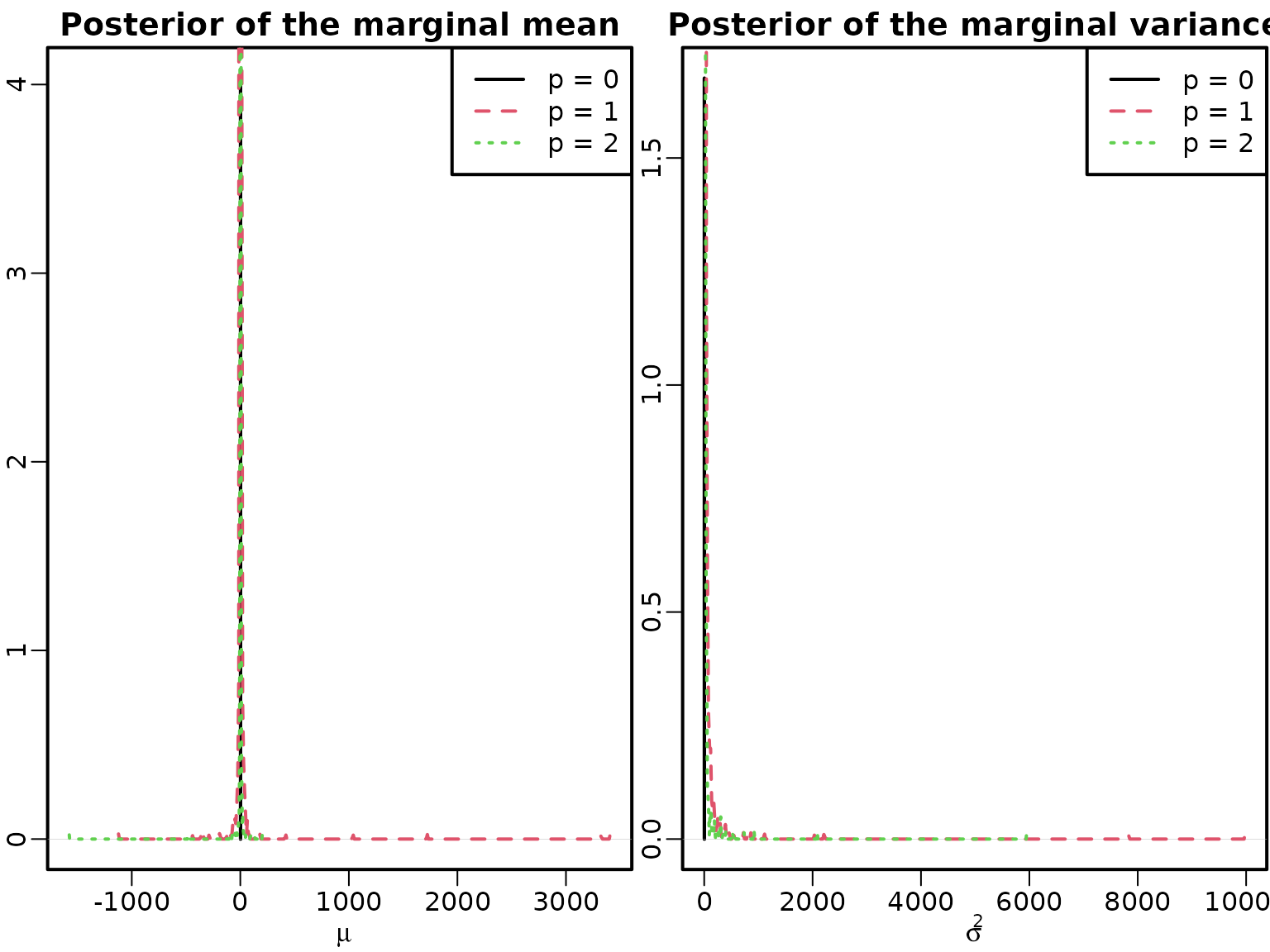

We continue by fitting an AR(0) model to the inflation data.

Xy <- ARdesignmatrix(inflation, 0) # Fill the N x 1 design matrix with 1s

res20 <- regression(inflation, Xy, prior = "improper")Before we can compute unconditional mean and unconditional variance from our fitted AR models, we need to remove nonstationary draws. Apart from that, we proceed as above.

mu <- sigma2 <- list()

mu[["0"]] <- res20$betas[, 1]

sigma2[["0"]] <- res20$sigma2s

for (p in 1:2) {

mu[[as.character(p)]] <- res2[[p]]$betas[!nonstationary[, p], 1] /

(1 - rowSums(res2[[p]]$betas[!nonstationary[, p], 2:(p + 1), drop = FALSE]))

}

# AR(1):

phi <- res2[[1]]$betas[!nonstationary[, 1], 2]

sigma2[["1"]] <- res2[[1]]$sigma2s[!nonstationary[, 1]] / (1 - phi^2)

# AR(2):

phi1 <- res2[[2]]$betas[!nonstationary[, 2], 2]

phi2 <- res2[[2]]$betas[!nonstationary[, 2], 3]

sigma2[["2"]] <- (1 - phi2) * res2[[2]]$sigma2s[!nonstationary[, 2]] /

((1 + phi2) * (1 - phi1^2 + phi2^2 - 2 * phi2))

plot(density(mu[["0"]], bw = "SJ", adj = 2), xlim = range(mu), ylab = "",

main = "Posterior of the marginal mean", xlab = expression(mu))

for (p in 1:2) lines(density(mu[[as.character(p)]], bw = "SJ", adj = 2),

col = p + 1, lty = p + 1)

legend("topright", paste0("p = ", 0:2), col = 1:3, lty = 1:3)

plot(density(sigma2[["0"]], bw = "SJ", adj = 2), xlim = range(sigma2),

xlab = expression(sigma^2), ylab = "",

main = "Posterior of the marginal variance", )

for (p in 1:2) lines(density(sigma2[[as.character(p)]], bw = "SJ", adj = 2),

col = p + 1, lty = p + 1)

legend("topright", paste0("p = ", 0:2), col = 1:3, lty = 1:3)

We now move on to imposing stationarity through employing a non-conjugate transformed beta prior on , i.e., and employ a 4-step sampler to obtain posterior draws. In addition, we assume that is unknown and a priori follows the stationary distribution of the AR(1) process.

We start by defining the density function of the rescaled beta.

dbetarescaled <- function(x, a, b, log = FALSE) {

tmp <- dbeta((x + 1) / 2, a, b, log = TRUE) - log(2)

if (log) tmp else exp(tmp)

}We need to specify the hyperparameters and define the left hand side variable as well as the design matrix.

# Specify the hyperparameters

c0 <- 0

C0 <- 0

b0 <- 0

B0 <- Inf

aphi <- 1

bphi <- 1

# Define the design matrix and y

y <- inflation

X <- matrix(NA_real_, nrow = length(y), 2)

X[, 1] <- 1

X[, 2] <- c(NA_real_, y[-length(y)])Now we are ready to sample!

# Allocate some space for the posterior draws and initialize the parameters:

y0s <- sigma2s <- zetas <- phis <- rep(NA_real_, ndraws)

zeta <- 0

phi <- .8

sigma2 <- var(y) * (1 - phi)

naccepts <- 0

for (m in seq_len(ndraws + nburn)) {

# Step (a): Draw y0

y0 <- rnorm(1, zeta + phi * y[1], sqrt(sigma2))

# Step (b): Draw the innovation variance

X[1, 2] <- y0

beta <- matrix(c(zeta, phi), nrow = 2)

tmp <- y - X %*% beta

sigma2 <- rinvgamma(1, c0 + (length(y) + 1) / 2,

C0 + .5 * (1 - phi^2) * (y0 - zeta / (1 - phi))^2 + .5 * crossprod(tmp))

# Step (c): Draw the intercept

BT <- 1 / (1 / B0 + (1 + phi) / (sigma2 * (1 - phi)) + length(y) / sigma2)

bT <- BT * (b0 / B0 + ((1 + phi) * y0 +

y[1] - phi * y0 + sum(y[-1] - phi * y[-length(y)])) / sigma2)

zeta <- rnorm(1, bT, sqrt(BT))

# Step (d): Draw the persistence

tmp <- y0^2 + sum(y[-length(y)]^2)

propmean <- (y0 * (y[1] - zeta) + sum(y[-length(y)] * (y[-1] - zeta))) / tmp

propvar <- sigma2 / tmp

phiprop <- rnorm(1, propmean, sqrt(propvar))

if (-1 < phiprop & phiprop < 1) {

logR <- dbetarescaled(phiprop, aphi, bphi, log = TRUE) -

dbetarescaled(phi, aphi, bphi, log = TRUE) +

dnorm(y0, zeta / (1 - phiprop), sqrt(sigma2 / (1 - phiprop^2)),

log = TRUE) -

dnorm(y0, zeta / (1 - phi), sqrt(sigma2 / (1 - phi^2)), log = TRUE)

if (log(runif(1)) < logR) {

phi <- phiprop

if (m > nburn) naccepts <- naccepts + 1L

}

}

# Store the draws

if (m > nburn) {

y0s[m - nburn] <- y0

sigma2s[m - nburn] <- sigma2

zetas[m - nburn] <- zeta

phis[m - nburn] <- phi

}

}

stationary1 <- data.frame(zeta = zetas, phi = phis, sigma2 = sigma2s, y0 = y0s)

naccepts1 <- nacceptsWe repeat the exercise with a more informative beta prior.

aphi <- 10

bphi <- 10

# Allocate some space for the posterior draws and initialize the parameters:

y0s <- sigma2s <- zetas <- phis <- rep(NA_real_, ndraws)

zeta <- 0

phi <- .8

sigma2 <- var(y) * (1 - phi)

naccepts <- 0

for (m in seq_len(ndraws + nburn)) {

# Step (a): Draw y0

y0 <- rnorm(1, zeta + phi * y[1], sqrt(sigma2))

# Step (b): Draw the innovation variance

X[1, 2] <- y0

beta <- matrix(c(zeta, phi), nrow = 2)

tmp <- y - X %*% beta

sigma2 <- rinvgamma(1, c0 + (length(y) + 1) / 2,

C0 + .5 * (1 - phi^2) * (y0 - zeta / (1 - phi))^2 + .5 * crossprod(tmp))

# Step (c): Draw the intercept

BT <- 1 / (1 / B0 + (1 + phi) / (sigma2 * (1 - phi)) + length(y) / sigma2)

bT <- BT * (b0 / B0 + ((1 + phi) * y0 +

y[1] - phi * y0 + sum(y[-1] - phi * y[-length(y)])) / sigma2)

zeta <- rnorm(1, bT, sqrt(BT))

# Step (d): Draw the persistence

tmp <- y0^2 + sum(y[-length(y)]^2)

propmean <- (y0 * (y[1] - zeta) + sum(y[-length(y)] * (y[-1] - zeta))) / tmp

propvar <- sigma2 / tmp

phiprop <- rnorm(1, propmean, sqrt(propvar))

if (-1 < phiprop & phiprop < 1) {

logR <- dbetarescaled(phiprop, aphi, bphi, log = TRUE) -

dbetarescaled(phi, aphi, bphi, log = TRUE) +

dnorm(y0, zeta / (1 - phiprop), sqrt(sigma2 / (1 - phiprop^2)),

log = TRUE) -

dnorm(y0, zeta / (1 - phi), sqrt(sigma2 / (1 - phi^2)), log = TRUE)

if (log(runif(1)) < logR) {

phi <- phiprop

if (m > nburn) naccepts <- naccepts + 1L

}

}

# Store the draws

if (m > nburn) {

y0s[m - nburn] <- y0

sigma2s[m - nburn] <- sigma2

zetas[m - nburn] <- zeta

phis[m - nburn] <- phi

}

}

stationary2 <- data.frame(zeta = zetas, phi = phis, sigma2 = sigma2s, y0 = y0s)

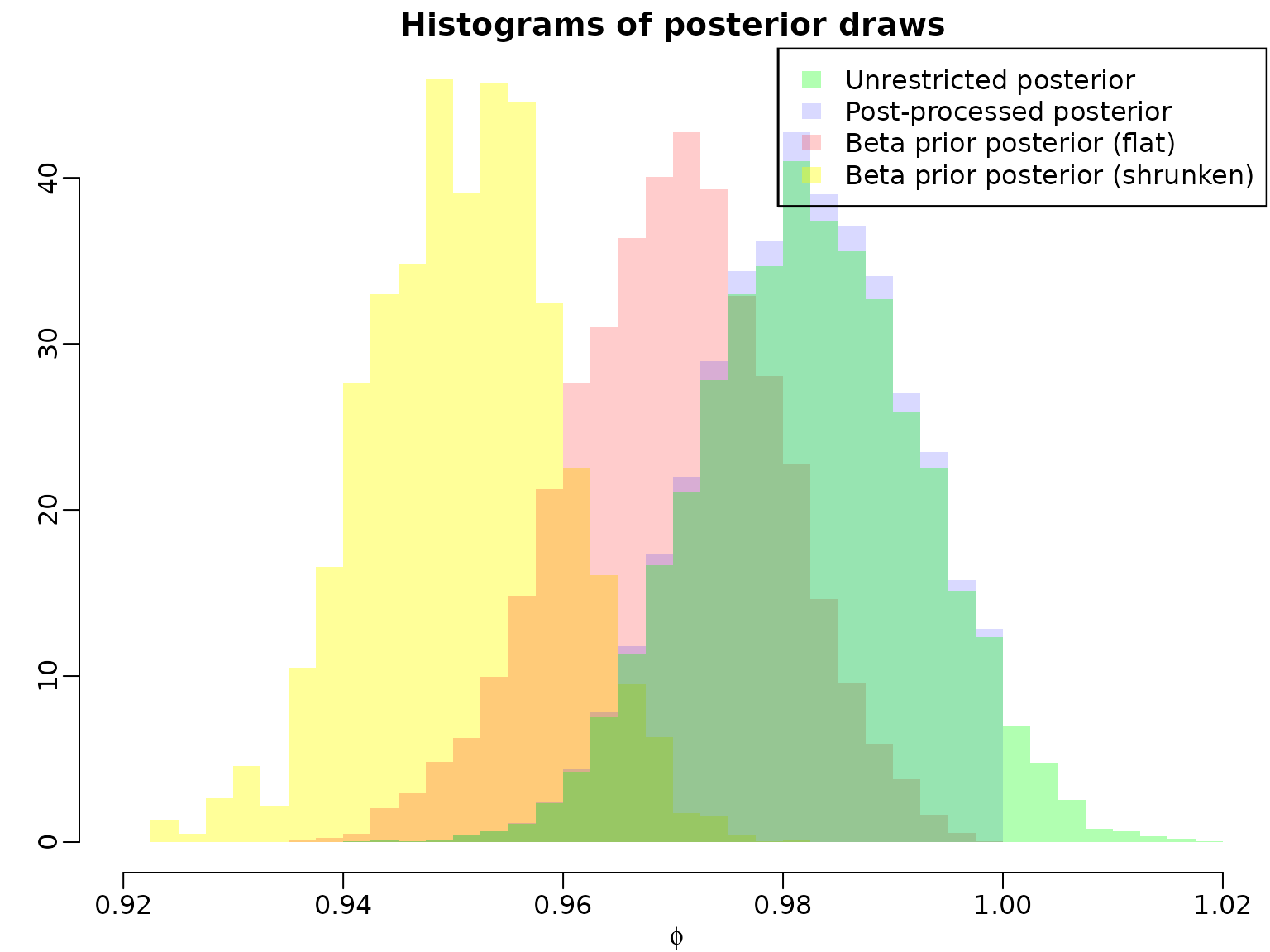

naccepts2 <- nacceptsTo conclude, we compare the posteriors of under the improper prior, the posterior obtained after post-processing draws to obtain stationarity, and the posterior under the stationary-enforcing shifted beta priors.

mybreaks <- seq(floor(100 * min(stationary1$phi, stationary2$phi)) / 100,

ceiling(100 * max(ar1draws)) / 100,

by = .0025)

hist(stationary2$phi, breaks = mybreaks, col = rgb(1, 1, 0, .4),

main = "Histograms of posterior draws", xlab = expression(phi),

freq = FALSE, ylab = "", border = NA)

hist(stationary1$phi, breaks = mybreaks, col = rgb(1, 0, 0, .2),

freq = FALSE, add = TRUE, border = NA)

hist(ar1draws[!nonstationary[, 1]], breaks = mybreaks, col = rgb(0, 0, 1, .15),

freq = FALSE, add = TRUE, border = NA)

hist(ar1draws, breaks = mybreaks, col = rgb(0, 1, 0, .3),

freq = FALSE, add = TRUE, border = NA)

legend("topright",

c("Unrestricted posterior", "Post-processed posterior",

"Beta prior posterior (flat)", "Beta prior posterior (shrunken)"),

fill = rgb(c(0, 0, 1, 1), c(1, 0, 0, 1), c(0, 1, 0, 0),

c(.3, .15, .2, .4)), border = NA)

Section 7.2.5: Evaluating the Efficiency of an MCMC Sampler

Example 7.11: Improving the independence MH step

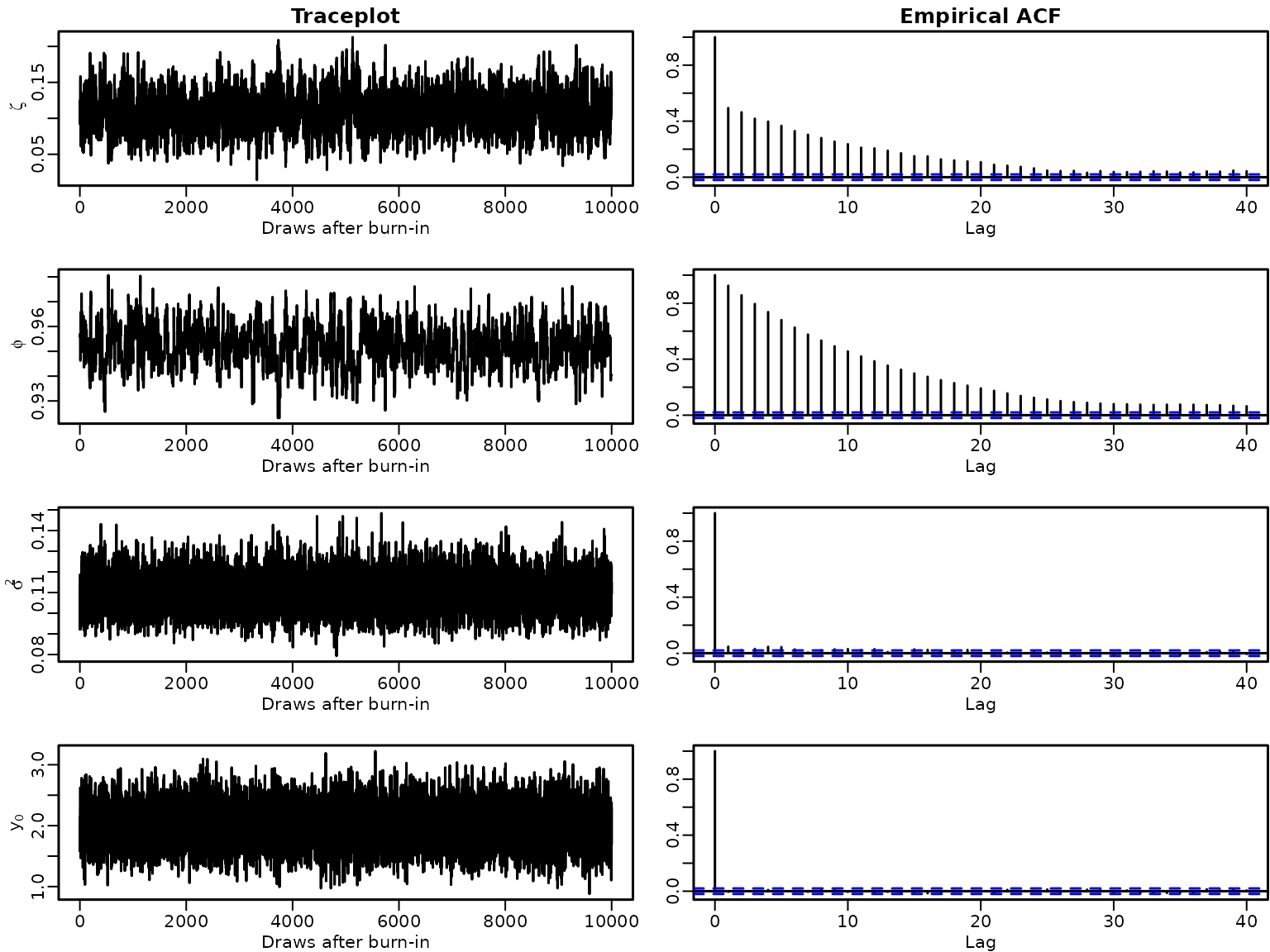

Let us investigate traceplots and empirical autocorrelation functions of the posterior draws under the informative stationarity-inducing prior.

par(mfrow = c(4, 2), mar = c(2.5, 2.8, 1.5, .1), mgp = c(1.5, .5, 0), lwd = 1.5)

for (i in seq_along(stationary2)) {

plot.ts(stationary2[i], xlab = "Draws after burn-in", ylab = labels[i])

if (i == 1) title("Traceplot")

acf(stationary2[i], ylab = "")

if (i == 1) title("Empirical ACF")

}

We now compute an estimate of the effective sample size (ESS) and the inefficiency factor (IF) use the coda package.

library("coda")

ess1 <- effectiveSize(data.frame(zeta = res2[[1]]$betas[, 1],

phi = res2[[1]]$betas[, 2],

sigma2 = res2[[1]]$sigma2s))

ess2 <- effectiveSize(data.frame(zeta = res2[[1]]$betas[!nonstationary[, 1], 1],

phi = res2[[1]]$betas[!nonstationary[, 1], 2],

sigma2 = res2[[1]]$sigma2s[!nonstationary[, 1]]))

ess3 <- effectiveSize(stationary1)

ess4 <- effectiveSize(stationary2)

ess <- rbind(unrestricted = c(ess1, y0 = NA),

postprocessed = c(ess2, y0 = NA),

betapriorflat = ess3,

betapriorinformative = ess4)

knitr::kable(round(ess))| zeta | phi | sigma2 | y0 | |

|---|---|---|---|---|

| unrestricted | 9562 | 10000 | 10000 | NA |

| postprocessed | 9184 | 9592 | 9592 | NA |

| betapriorflat | 2301 | 2189 | 10000 | 10000 |

| betapriorinformative | 634 | 338 | 6211 | 10000 |

| zeta | phi | sigma2 | y0 | |

|---|---|---|---|---|

| unrestricted | 1.05 | 1.00 | 1.00 | NA |

| postprocessed | 1.09 | 1.04 | 1.04 | NA |

| betapriorflat | 4.35 | 4.57 | 1.00 | 1 |

| betapriorinformative | 15.77 | 29.55 | 1.61 | 1 |

We now repeat the above exercise, but use the conditional posterior resulting from an auxiliary moment-matched prior in Step (d).

Note: Currently, three methods are implemented:

Ignore the part coming from and only moment-match the shifted beta prior. This is currently described in the manuscript (auxprior = analytical1)

Use a part coming from the determinant of the density of , resulting in a shifted (auxprior = analytical2)

Numerically approximate mode and curvature of the distribution at every iteration (auxprior = numerical)

auxprior <- "analytical1"

if (auxprior == "analytical1") {

aphiprop <- aphi

bphiprop <- bphi

} else if (auxprior == "analytical2") {

# Add .5 to aphi and bphi (from the determinant of the initial state prior)

aphiprop <- aphi + .5

bphiprop <- bphi + .5

}

if (auxprior != "numerical") {

# Compute mean and variance of the proposal using properties of the beta

auxpriormean <- 2 * aphiprop / (aphiprop + bphiprop) - 1

auxpriorvar <- 4 * (aphiprop * bphiprop) /

((aphiprop + bphiprop)^2 * (aphiprop + bphiprop + 1))

} else {

# For the numerical method, we need the density function of the target

dprior <- function(phi, zeta, sigma2, y0, aphi, bphi, log = FALSE) {

inside <- phi <= 1 & phi >= -1

logdens <- -Inf

logdens[inside] <- dbetarescaled(phi[inside], aphi, bphi, log = TRUE) +

dnorm(y0, zeta / (1 - phi[inside]), sqrt(sigma2 / (1 - phi[inside]^2)),

log = TRUE)

if (log) logdens else exp(logdens)

}

}

# Allocate some space for the posterior draws and initialize the parameters:

y0s <- sigma2s <- zetas <- phis <- rep(NA_real_, ndraws)

zeta <- 0

phi <- .8

sigma2 <- var(y) * (1 - phi)

naccepts <- 0

for (m in seq_len(ndraws + nburn)) {

# Step (a): Draw y0

y0 <- rnorm(1, zeta + phi * y[1], sqrt(sigma2))

# Step (b): Draw the innovation variance

X[1, 2] <- y0

beta <- matrix(c(zeta, phi), nrow = 2)

tmp <- y - X %*% beta

sigma2 <- rinvgamma(1, c0 + (length(y) + 1) / 2,

C0 + .5 * (1 - phi^2) * (y0 - zeta / (1 - phi))^2 + .5 * crossprod(tmp))

# Step (c): Draw the intercept

BT <- 1 / (1 / B0 + (1 + phi) / (sigma2 * (1 - phi)) + length(y) / sigma2)

bT <- BT * (b0 / B0 + ((1 + phi) * y0 +

y[1] - phi * y0 + sum(y[-1] - phi * y[-length(y)])) / sigma2)

zeta <- rnorm(1, bT, sqrt(BT))

# Step (d): Draw the persistence

if (auxprior == "numerical") { # overwrites pre-defined mean and variance

mode <- optimize(dprior, c(-1, 1), zeta = zeta, sigma2 = sigma2, y0 = y0,

aphi = aphi, bphi = bphi, log = TRUE, maximum = TRUE)$maximum

dd <- numDeriv::hessian(dprior, mode, zeta = zeta, sigma2 = sigma2, y0 = y0,

aphi = aphi, bphi = bphi)

auxpriormean <- mode

auxpriorvar <- -1 / as.numeric(dd)

}

tmp <- y0^2 + sum(y[-length(y)]^2)

propvar <- 1 / (1 / auxpriorvar + tmp / sigma2)

propmean <- propvar * (auxpriormean / auxpriorvar + (y0 * (y[1] - zeta) +

sum(y[-length(y)] * (y[-1] - zeta))) / sigma2)

phiprop <- rnorm(1, propmean, sqrt(propvar))

if (-1 < phiprop & phiprop < 1) {

logR <- dbetarescaled(phiprop, aphi, bphi, log = TRUE) -

dbetarescaled(phi, aphi, bphi, log = TRUE) +

dnorm(y0, zeta / (1 - phiprop), sqrt(sigma2 / (1 - phiprop^2)),

log = TRUE) -

dnorm(y0, zeta / (1 - phi), sqrt(sigma2 / (1 - phi^2)), log = TRUE) +

dnorm(phi, auxpriormean, sqrt(auxpriorvar), log = TRUE) -

dnorm(phiprop, auxpriormean, sqrt(auxpriorvar), log = TRUE)

if (log(runif(1)) < logR) {

phi <- phiprop

if (m > nburn) naccepts <- naccepts + 1L

}

}

# Store the draws

if (m > nburn) {

y0s[m - nburn] <- y0

sigma2s[m - nburn] <- sigma2

zetas[m - nburn] <- zeta

phis[m - nburn] <- phi

}

}

stationary3 <- data.frame(zeta = zetas, phi = phis, sigma2 = sigma2s, y0 = y0s)

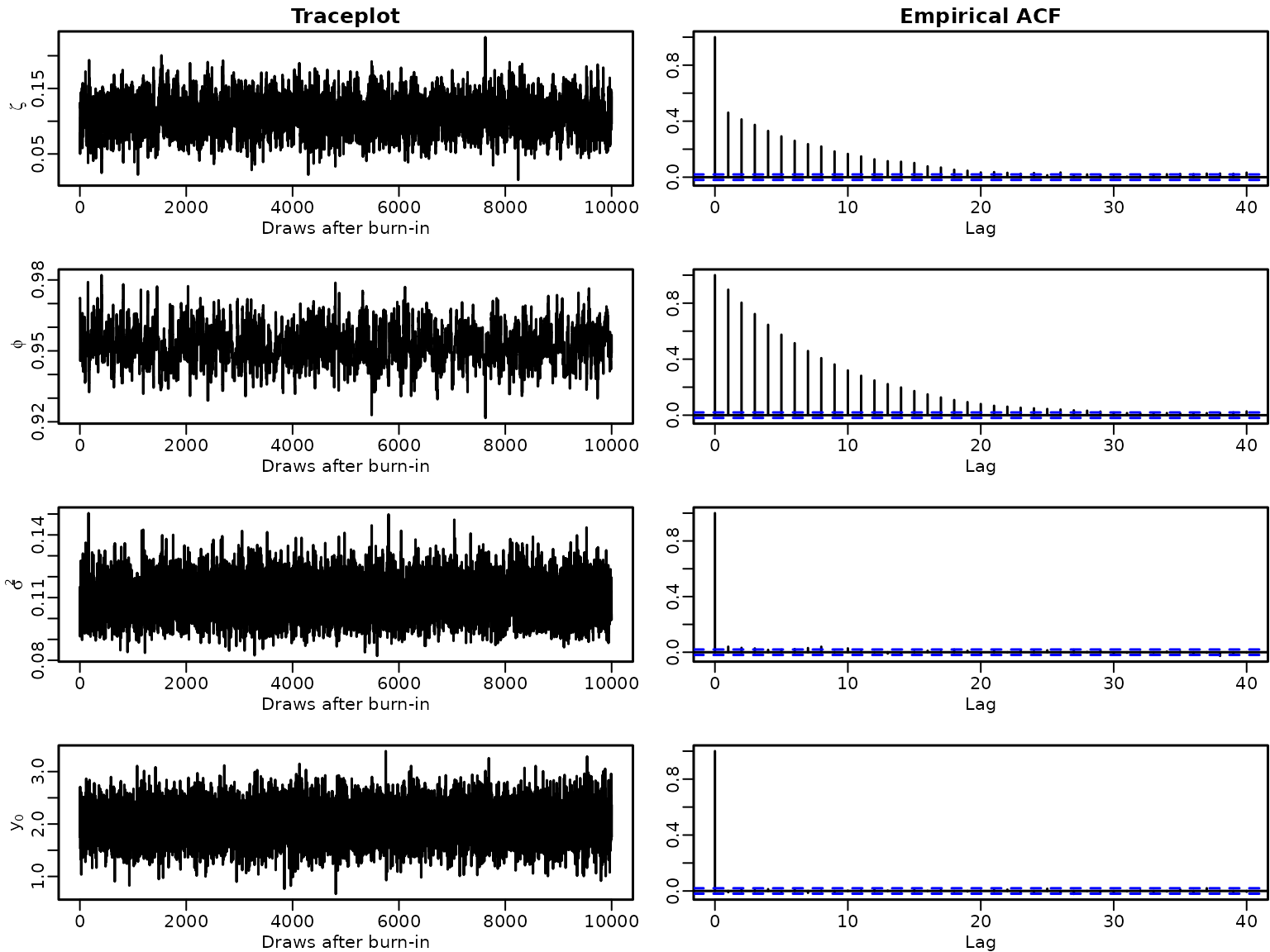

naccepts3 <- nacceptsAgain, we investigate traceplots and empirical autocorrelation functions of the draws. In addition, we check the percentage of accepted draws in MH-step (d).

par(mfrow = c(4, 2), mar = c(2.5, 2.8, 1.5, .1), mgp = c(1.5, .5, 0), lwd = 1.5)

for (i in seq_along(stationary3)) {

plot.ts(stationary3[i], xlab = "Draws after burn-in", ylab = labels[i])

if (i == 1) title("Traceplot")

acf(stationary3[i], ylab = "")

if (i == 1) title("Empirical ACF")

}

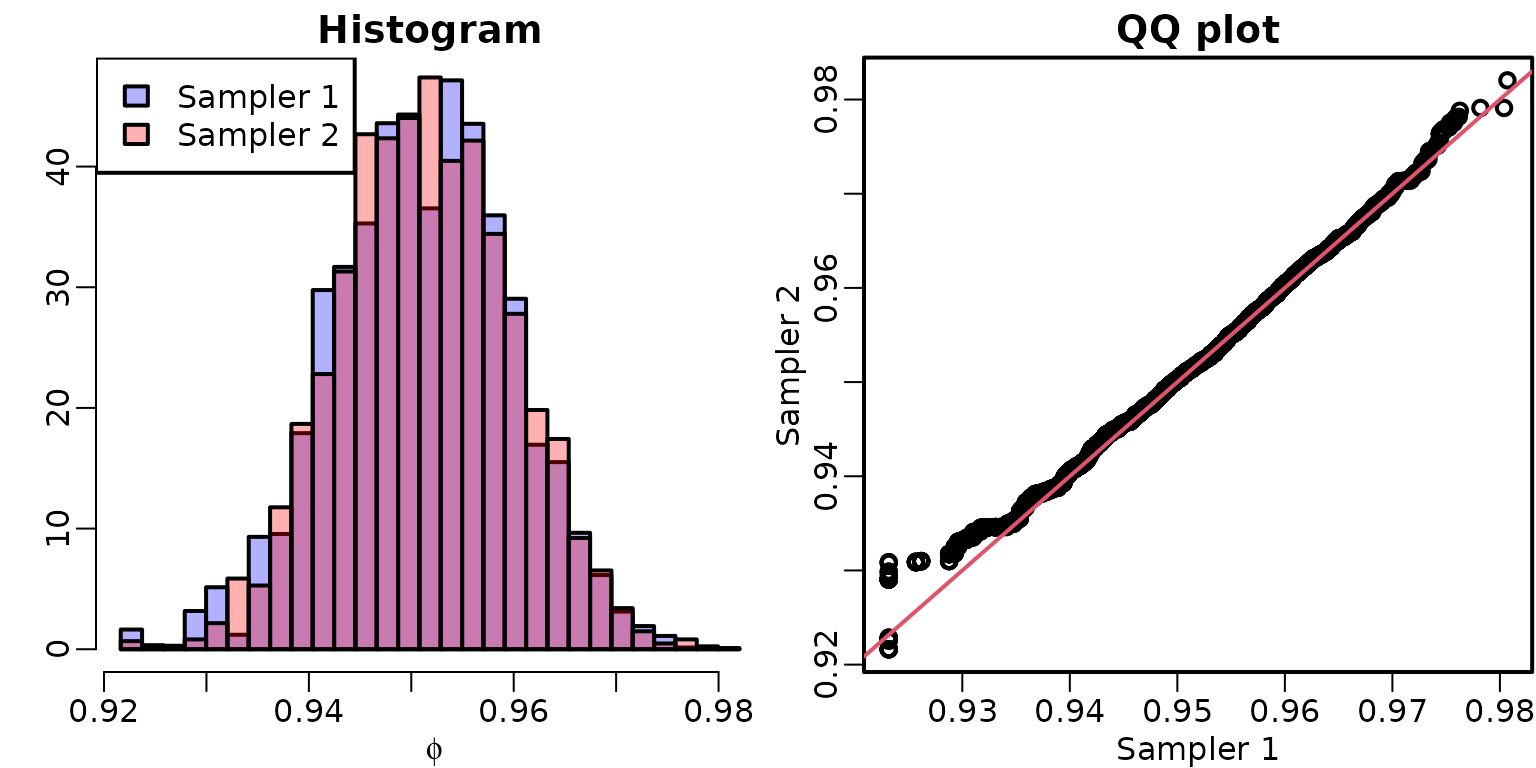

We now compare the draws from the two samplers; they should yield draws from the same distribution, irrespective of the acceptance rate and thus the mixing of the Markov chain. We graphically check this by comparing histograms and quantiles of draws from the marginal posterior of .

mybreaks <- seq(min(stationary2$phi, stationary3$phi),

max(stationary2$phi, stationary3$phi),

length.out = 30)

hist(stationary2$phi, breaks = mybreaks, col = rgb(0, 0, 1, .3),

main = "Histogram", xlab = expression(phi), freq = FALSE, ylab = "")

hist(stationary3$phi, breaks = mybreaks, col = rgb(1, 0, 0, .3), freq = FALSE,

add = TRUE)

legend("topleft", c("Sampler 1", "Sampler 2"), fill = rgb(0:1, 0, 1:0, .3))

qqplot(stationary2$phi, stationary3$phi, xlab = "Sampler 1", ylab = "Sampler 2",

main = "QQ plot")

abline(0, 1, col = 2)

We can see that the draws appear to come from the same distribution. Note, however, that the first sampler gets “stuck” slightly below 0.93 for a few draws, which isn’t the case for the second sampler.

To conclude, we compute ESSs and IFs for the sampler utilizing the optimized MH step.

ess1 <- effectiveSize(stationary2)

ess2 <- effectiveSize(stationary3)

ess <- rbind(`Sampler 1` = ess1, `Sampler 2` = ess2)

knitr::kable(round(ess))| zeta | phi | sigma2 | y0 | |

|---|---|---|---|---|

| Sampler 1 | 634 | 338 | 6211 | 10000 |

| Sampler 2 | 966 | 504 | 7172 | 10000 |

| zeta | phi | sigma2 | y0 | |

|---|---|---|---|---|

| Sampler 1 | 15.77 | 29.55 | 1.61 | 1 |

| Sampler 2 | 10.35 | 19.85 | 1.39 | 1 |

Section 7.3: Some Extensions

Section 7.3.1: AR Models with a Unit Root

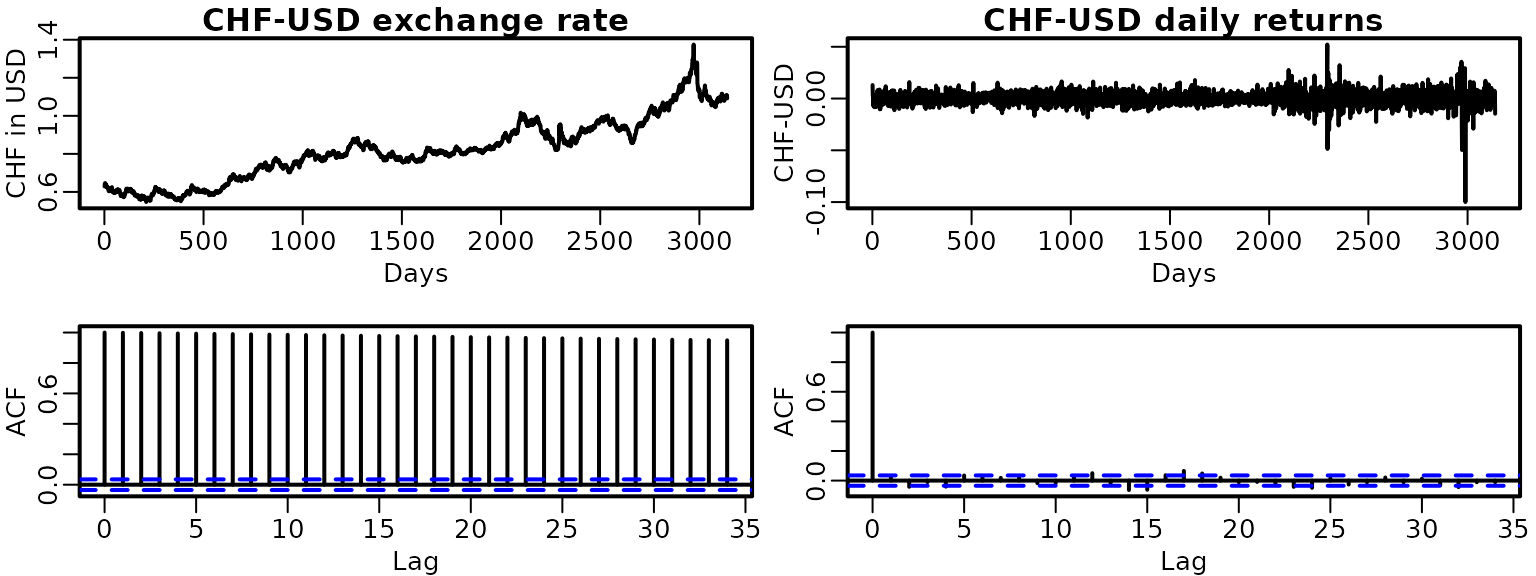

Let us check for stationarity of the exchange rate data. First, we load the data and visualize it as well as its empirical ACF. We do the same for the absolute returns.

data("exrates", package = "stochvol")

dat <- exrates$USD / exrates$CHF

ret <- diff(dat)

plot(dat, type = "l", main = "CHF-USD exchange rate", xlab = "Days",

ylab = "CHF in USD")

plot(ret, type = "l", main = "CHF-USD daily returns", xlab = "Days",

ylab = "CHF-USD")

acf(dat)

acf(ret)

This clearly hints at non-stationarity of the exchange rate series and at (first order) stationarity of the returns. To check more formally, we fit AR(p) models to both.

ardat <- arret <- list()

for (p in 1:4) {

y <- tail(dat, -p)

Xy <- ARdesignmatrix(dat, p)

ardat[[p]] <- regression(y, Xy, prior = "improper")

y <- tail(ret, -p)

Xy <- ARdesignmatrix(ret, p)

arret[[p]] <- regression(y, Xy, prior = "improper")

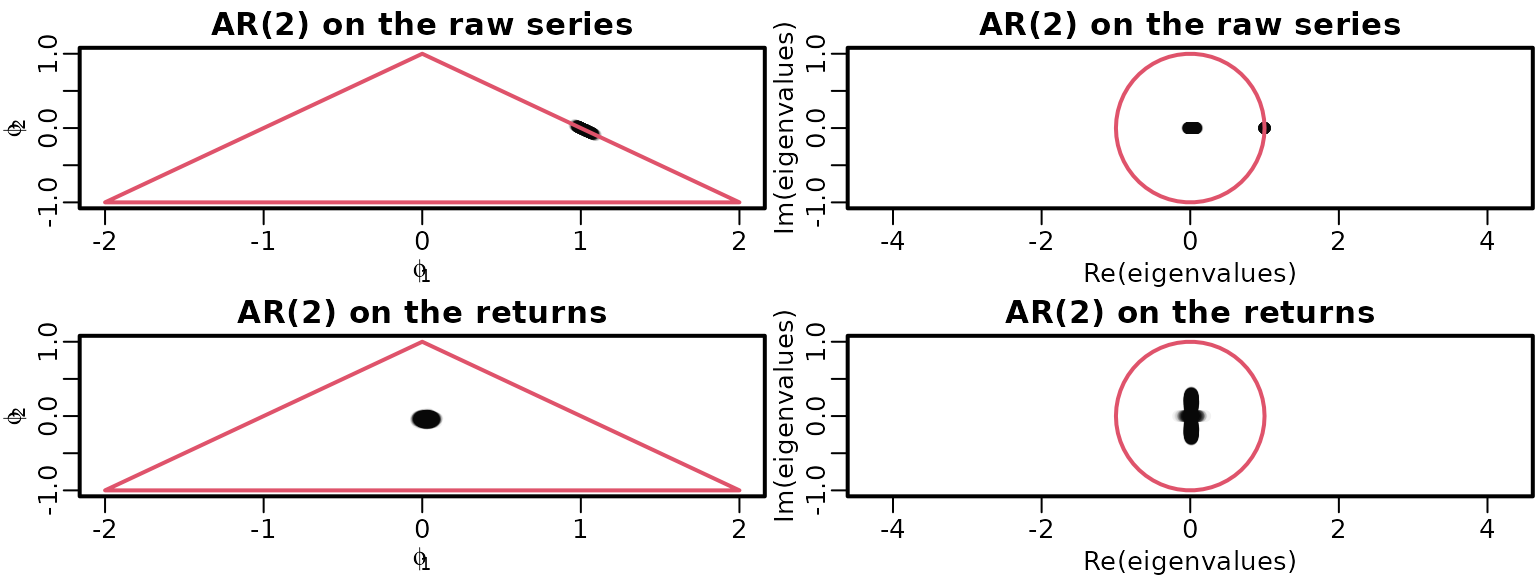

}Now we can graphically investigate stationarity as above.

draws <- list(ardat[[2]]$betas[, 2:3], arret[[2]]$betas[, 2:3])

eigenvalues <- matrix(NA_complex_, nrow(draws[[1]]), ncol(draws[[1]]))

mains <- c("AR(2) on the raw series", "AR(2) on the returns")

for (i in seq_along(draws)) {

plot(draws[[i]], main = mains[i], xlab = bquote(phi[1]),

ylab = bquote(phi[2]), xlim = c(-2, 2), ylim = c(-1, 1),

col = rgb(0, 0, 0, .05), pch = 16)

polygon(c(-2, 0, 2, -2), c(-1, 1, -1, -1), border = 2)

for (m in seq_len(nrow(draws[[i]]))) {

Phi <- matrix(c(draws[[i]][m, ], c(1, 0)), byrow = TRUE, nrow = 2)

eigenvalues[m, ] <- eigen(Phi, only.values = TRUE)$values

}

plot(eigenvalues, xlim = c(-1, 1), ylim = c(-1, 1), asp = 1,

main = mains[i], col = rgb(0, 0, 0, .05), pch = 16)

symbols(0, 0, 1, add = TRUE, fg = 2, inches = FALSE)

}

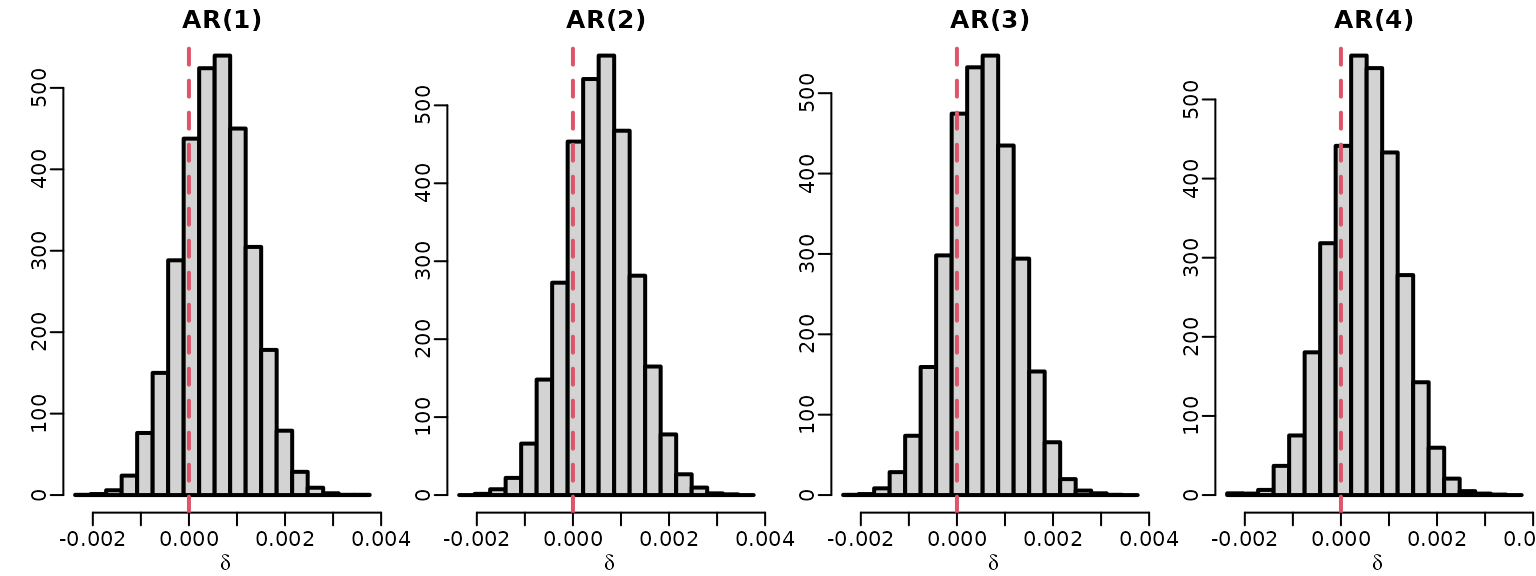

To explore whether the nonstationarity of the raw series could be caused by a unit root, we investigate the posterior of for .

toplot <- matrix(NA_real_, ndraws, 4)

for (p in 1:4)

toplot[, p] <- rowSums(ardat[[p]]$betas[, 2:(p + 1), drop = FALSE]) - 1

for (p in 1:4) {

hist(toplot[, p], freq = FALSE,

breaks = seq(min(toplot), max(toplot), length.out = 20),

main = paste0("AR(", p, ")"), xlab = expression(delta), ylab = "")

abline(v = 0, lty = 2, col = 2)

}

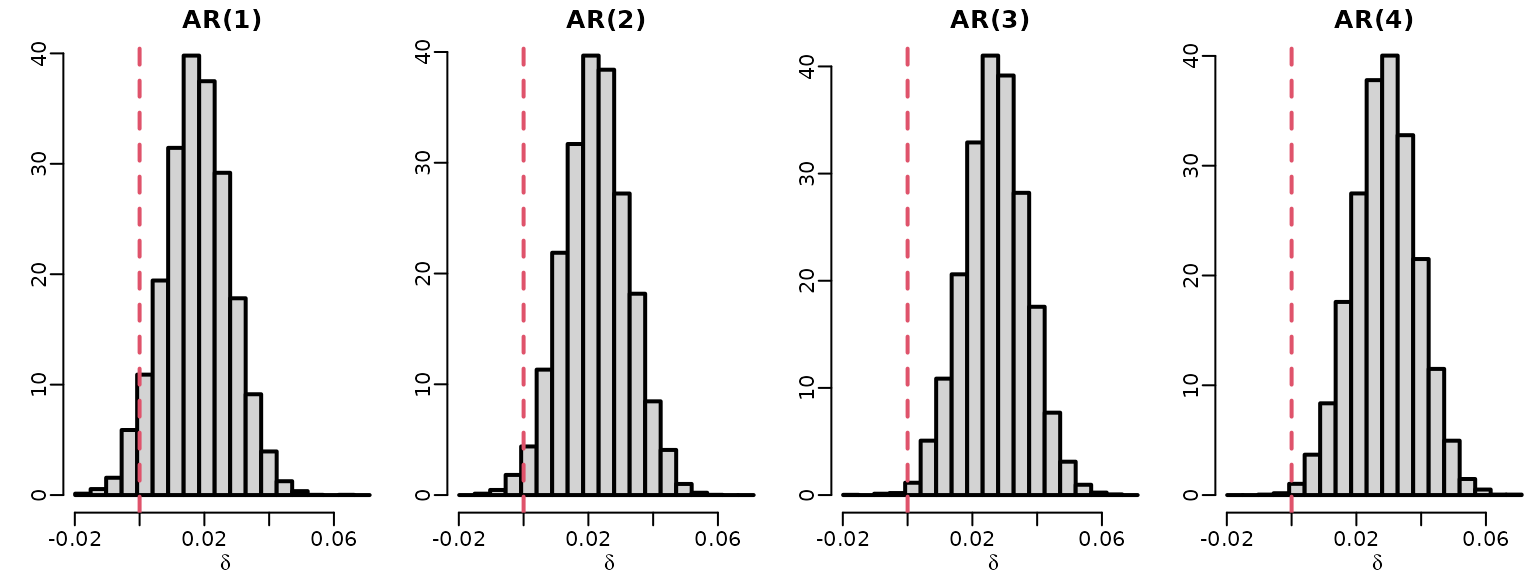

We do the same for the inflation data.

ardat <- arret <- list()

for (p in 1:4) {

y <- tail(inflation, -p)

Xy <- ARdesignmatrix(inflation, p)

ardat[[p]] <- regression(y, Xy, prior = "improper")

}

for (p in 1:4)

toplot[, p] <- rowSums(ardat[[p]]$betas[, 2:(p + 1), drop = FALSE]) - 1

for (p in 1:4) {

hist(toplot[, p], freq = FALSE,

breaks = seq(min(toplot), max(toplot), length.out = 20),

main = paste0("AR(", p, ")"), xlab = expression(delta), ylab = "")

abline(v = 0, lty = 2, col = 2)

}

Section 7.3.2: Bayesian Learning of an MA(1) Model

We now implement the MCMC sampler for fitting an MA(1) model, where we treat the latent state as unknown. For the innovation variance, we assume an inverse gamma prior, and is assumed to be a priori uniform on .

# Specify prior hyperparameters

c0 <- C0 <- 0.01

# standard deviation for random walk MH proposal

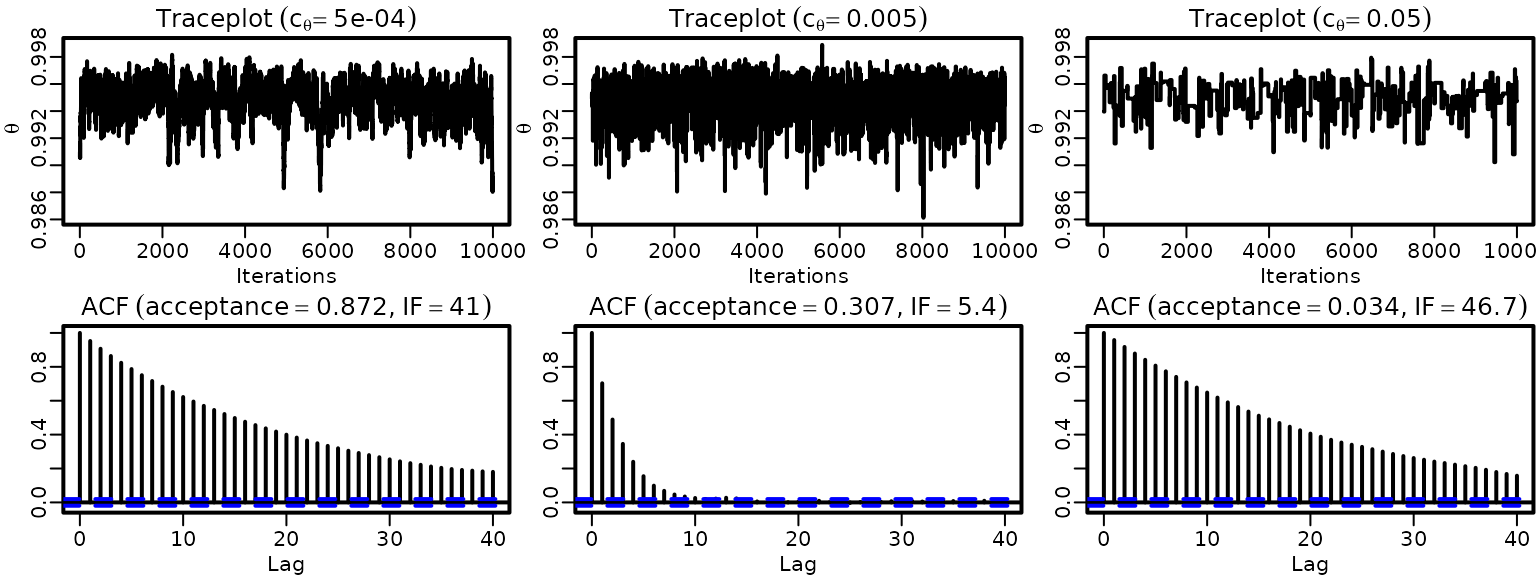

cthetas <- c(.0005, .005, .05)

# Allocate space for the draws

eps0s <- sigma2s <- thetas <- matrix(NA_real_, ndraws, length(cthetas))

naccepts <- rep(0L, length(cthetas))

for (i in seq_along(cthetas)) {

# Set the starting values

theta <- 0.9

sigma2 <- var(dat) / 2

# MCMC loop

for (m in seq_len(ndraws + nburn)) {

# Sample epsilon_0

bs <- (-theta)^seq_along(dat)

as <- filter(dat, -theta, "recursive")

tmp <- 1 + sum(bs^2)

eps0 <- rnorm(1, -sum(as * bs) / tmp, sqrt(sigma2 / tmp))

# Sample sigma^2

eps <- filter(dat, -theta, "recursive", init = eps0)

cN <- c0 + (length(dat) + 1) / 2

CN <- C0 + 0.5 * (eps0^2 + sum(eps^2))

sigma2 <- rinvgamma(1, cN, CN)

# Sample theta via RW-MH

thetaprop <- rnorm(1, theta, cthetas[i])

epsprop <- filter(dat, -thetaprop, "recursive", init = eps0)

# Now we accept/reject. Note that because we have a uniform prior on

# (-1, 1), it suffices to check whether the proposed value is in that

# interval and we do not need to include the prior in the acceptance ratio

if (abs(thetaprop) < 1) {

logR <- -0.5 / sigma2 * (sum(epsprop^2) - sum(eps^2))

if (log(runif(1)) < logR) {

theta <- thetaprop

if (m > nburn) naccepts[i] <- naccepts[i] + 1L

}

}

# Store the results

if (m > nburn) {

eps0s[m - nburn, i] <- eps0

sigma2s[m - nburn, i] <- sigma2

thetas[m - nburn, i] <- theta

}

}

}Now we plot traceplots and ACFs.

for (i in seq_along(cthetas)) {

ts.plot(thetas[, i], ylim = range(thetas), ylab = expression(theta),

xlab = "Iterations")

title(bquote(Traceplot ~ (c[theta] == .(cthetas[i]))))

acf(thetas[, i], ylab = "")

title(bquote(ACF ~ (acceptance == .(round(naccepts[i] / ndraws, 3))*","~

IF == .(round(ndraws / coda::effectiveSize(thetas[, i]), 1)))))

}

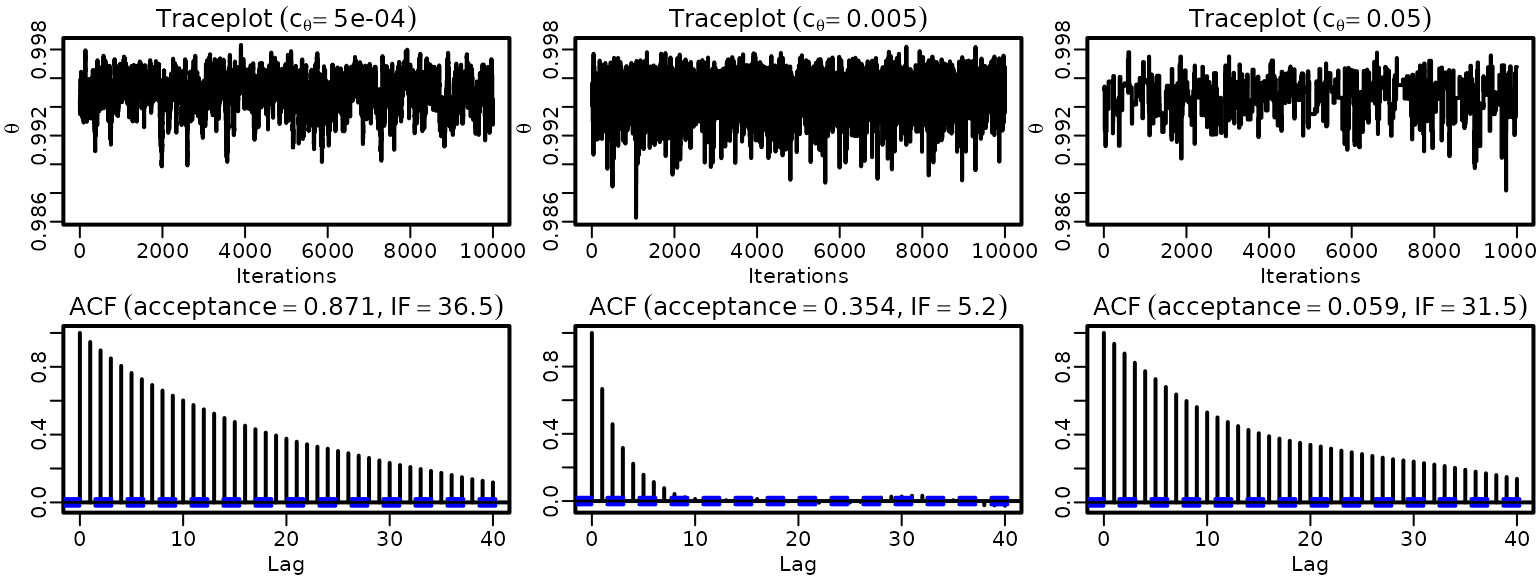

We repeat the exercise above, but now use a truncated Gaussian proposal for the random walk MH algorithm.

# standard deviation for random walk MH proposal

cthetas2 <- cthetas

# Allocate space for the draws

eps0s2 <- sigma2s2 <- thetas2 <- matrix(NA_real_, ndraws, length(cthetas2))

naccepts2 <- rep(0L, length(cthetas2))

for (i in seq_along(cthetas2)) {

# Set the starting values

theta <- 0.9

sigma2 <- var(dat) / 2

# MCMC loop

for (m in seq_len(ndraws + nburn)) {

# Sample epsilon_0

bs <- (-theta)^seq_along(dat)

as <- filter(dat, -theta, "recursive")

tmp <- 1 + sum(bs^2)

eps0 <- rnorm(1, -sum(as * bs) / tmp, sqrt(sigma2 / tmp))

# Sample sigma^2

eps <- filter(dat, -theta, "recursive", init = eps0)

cN <- c0 + (length(dat) + 1) / 2

CN <- C0 + 0.5 * (eps0^2 + sum(eps^2))

sigma2 <- rinvgamma(1, cN, CN)

# Sample theta via RW-MH using inverse transform sampling

# for the truncated Gaussian

pL <- pnorm(-1, theta, cthetas2[i])

pU <- pnorm(1, theta, cthetas2[i])

norm <- pU - pL

U <- runif(1)

thetaprop <- qnorm(pL + U * norm, theta, cthetas2[i])

epsprop <- filter(dat, -thetaprop, "recursive", init = eps0)

normprop <- diff(pnorm(c(-1, 1), thetaprop, cthetas2[i]))

# Now we accept/reject. Note that because we have a uniform prior on

# (-1, 1) and, due to the truncated proposal, we can be sure that a

# value within (-1, 1) is proposed, we do not need to include the

# prior in the acceptance ratio. However, we need to cater for the

# asymmetry of the proposal!

logR <- -0.5 / sigma2 * (sum(epsprop^2) - sum(eps^2)) +

log(norm) - log(normprop)

if (log(runif(1)) < logR) {

theta <- thetaprop

if (m > nburn) naccepts2[i] <- naccepts2[i] + 1L

}

# Store the results

if (m > nburn) {

eps0s2[m - nburn, i] <- eps0

sigma2s2[m - nburn, i] <- sigma2

thetas2[m - nburn, i] <- theta

}

}

}We again plot traceplots and ACFs.

for (i in seq_along(cthetas2)) {

ts.plot(thetas2[, i], ylim = range(thetas2), ylab = expression(theta),

xlab = "Iterations")

title(bquote(Traceplot ~ (c[theta] == .(cthetas2[i]))))

acf(thetas2[, i], ylab = "")

title(bquote(ACF ~ (acceptance == .(round(naccepts2[i] / ndraws, 3))*","~

IF == .(round(ndraws / coda::effectiveSize(thetas2[, i]), 1)))))

}

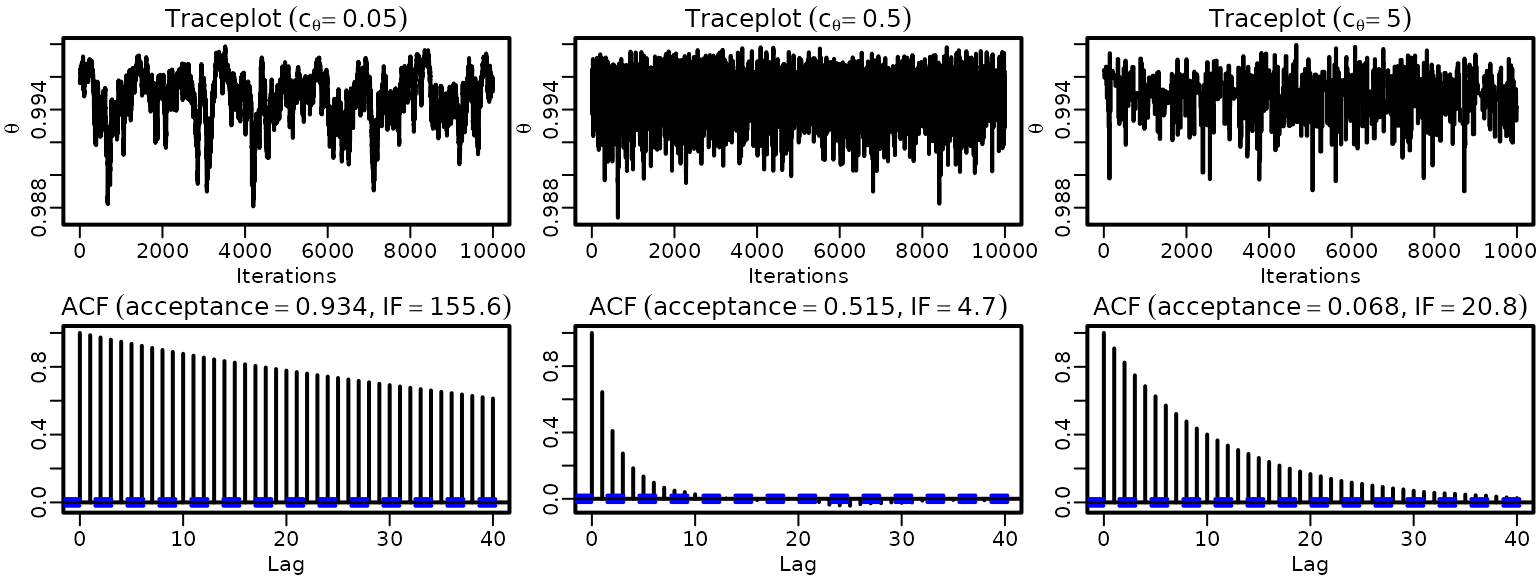

We repeat the exercise above once more, but now use a random walk proposal on .

# Define the transformation and its inverse

trans <- function(theta) log(1 + theta) - log(1 - theta)

invtrans <- function(thetatrans) (exp(thetatrans) - 1) / (exp(thetatrans) + 1)

# standard deviation for random walk MH proposal

cthetas3 <- 100 * cthetas2

# Allocate space for the draws

eps0s3 <- sigma2s3 <- thetas3 <- matrix(NA_real_, ndraws, length(cthetas3))

naccepts3 <- rep(0L, length(cthetas3))

for (i in seq_along(cthetas3)) {

# Set the starting values

theta <- 0.9

sigma2 <- var(dat) / 2

# MCMC loop

for (m in seq_len(ndraws + nburn)) {

# Sample epsilon_0

bs <- (-theta)^seq_along(dat)

as <- filter(dat, -theta, "recursive")

tmp <- 1 + sum(bs^2)

eps0 <- rnorm(1, -sum(as * bs) / tmp, sqrt(sigma2 / tmp))

# Sample sigma^2

eps <- filter(dat, -theta, "recursive", init = eps0)

cN <- c0 + (length(dat) + 1) / 2

CN <- C0 + 0.5 * (eps0^2 + sum(eps^2))

sigma2 <- rinvgamma(1, cN, CN)

# Sample theta via RW-MH on a trans(theta)

thetatransprop <- rnorm(1, trans(theta), cthetas3[i])

thetaprop <- invtrans(thetatransprop)

epsprop <- filter(dat, -thetaprop, "recursive", init = eps0)

# Now we accept/reject. Note that because we have a uniform prior on

# (-1, 1) and, due to the transformation, we can be sure that a

# value within (-1, 1) is proposed, we do not need to include the

# prior in the acceptance ratio. However, we need to cater for the

# asymmetry of the proposal!

logR <- -0.5 / sigma2 * (sum(epsprop^2) - sum(eps^2)) +

log(1 - thetaprop^2) - log(1 - theta^2)

if (log(runif(1)) < logR) {

theta <- thetaprop

if (m > nburn) naccepts3[i] <- naccepts3[i] + 1L

}

# Store the results

if (m > nburn) {

eps0s3[m - nburn, i] <- eps0

sigma2s3[m - nburn, i] <- sigma2

thetas3[m - nburn, i] <- theta

}

}

}We again plot traceplots and ACFs.

for (i in seq_along(cthetas3)) {

ts.plot(thetas3[, i], ylim = range(thetas3), ylab = expression(theta),

xlab = "Iterations")

title(bquote(Traceplot ~ (c[theta] == .(cthetas3[i]))))

acf(thetas3[, i], ylab = "")

title(bquote(ACF ~ (acceptance == .(round(naccepts3[i] / ndraws, 3))*","~

IF == .(round(ndraws / coda::effectiveSize(thetas3[, i]), 1)))))

}

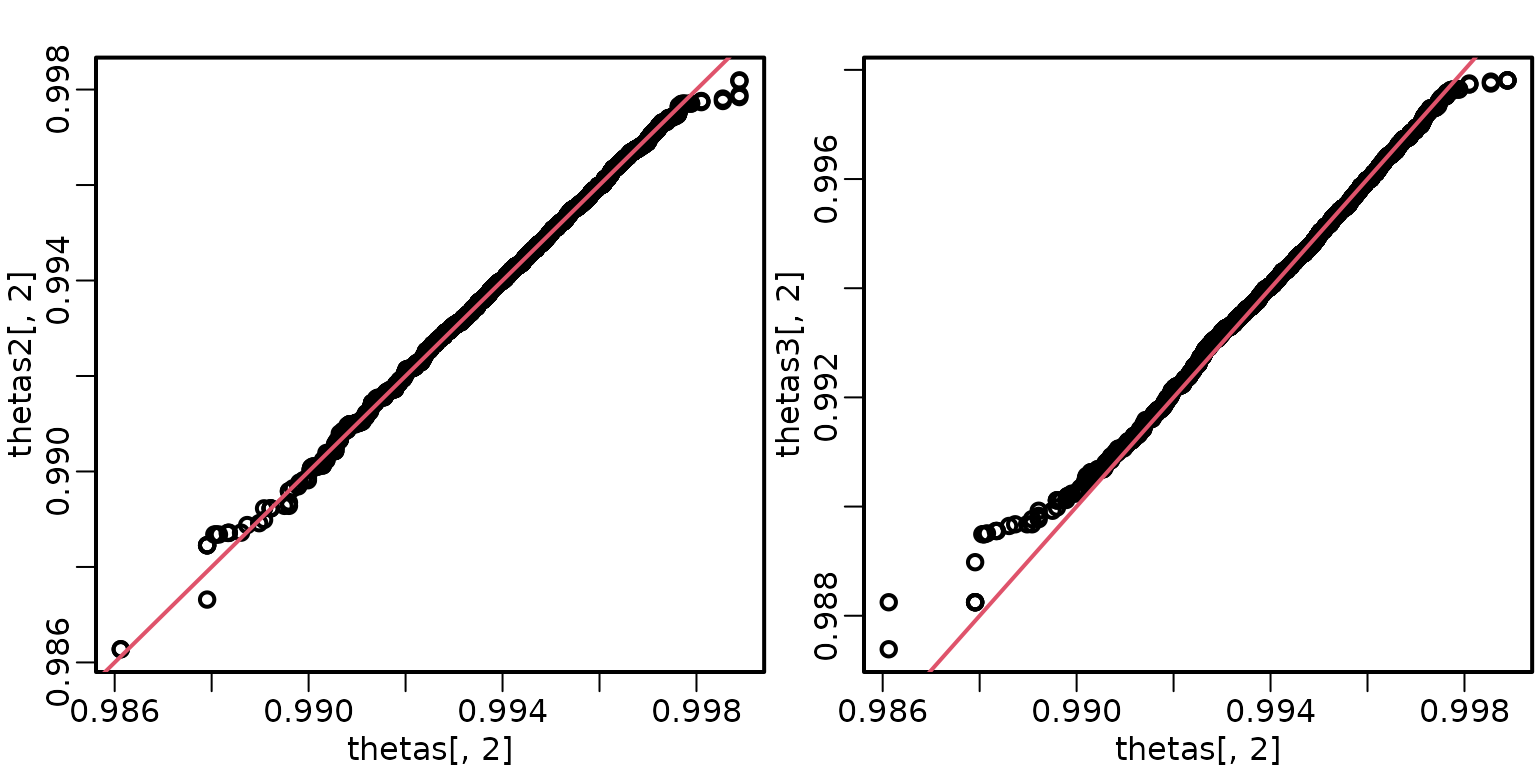

Let’s also check some QQ plots for equivalence.

Now, we compare acceptance rates and inefficiency factors for all 9 samplers.

accepts <- matrix(c(naccepts, naccepts2, naccepts3) / ndraws,

nrow = length(naccepts), ncol = 3, byrow = TRUE)

ESS <- matrix(coda::effectiveSize(cbind(thetas, thetas2, thetas3)),

nrow = ncol(thetas), ncol = 3, byrow = TRUE)

colnames(ESS) <- colnames(accepts) <- c("tiny", "medium", "huge")

rownames(ESS) <- rownames(accepts) <- c("Gaussian RW", "truncated RW",

"transformed RW")

IF <- ndraws / ESS

knitr::kable(round(accepts, 2))| tiny | medium | huge | |

|---|---|---|---|

| Gaussian RW | 0.87 | 0.31 | 0.03 |

| truncated RW | 0.87 | 0.35 | 0.06 |

| transformed RW | 0.94 | 0.52 | 0.07 |

| tiny | medium | huge | |

|---|---|---|---|

| Gaussian RW | 39.3 | 5.8 | 46.0 |

| truncated RW | 36.3 | 5.2 | 31.8 |

| transformed RW | 143.1 | 4.7 | 20.5 |

Section 7.4: Markov modeling for a panel of categorical time series

Example 7.13: Wage mobility data

We load the data and only consider workers from the birth cohort 1946-1960.

data("labor", package = "BayesianLearningCode")

labor <- subset(labor, birthyear >= 1946 & birthyear <= 1960)

nrow(labor)

#> [1] 1538We extract the columns about the income over time:

income <- labor[, grepl("^income", colnames(labor))]

income <- sapply(income, as.integer)

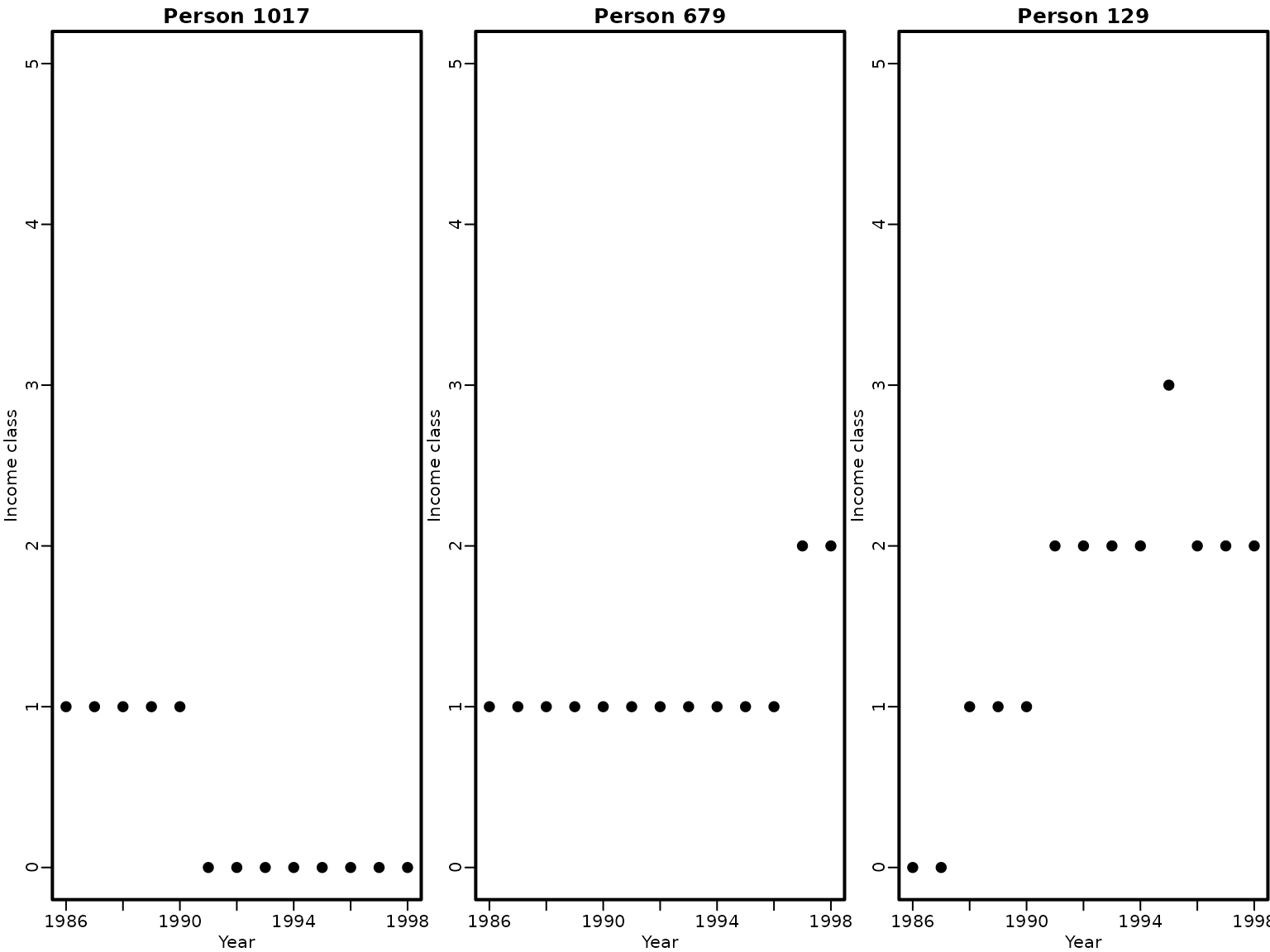

colnames(income) <- gsub("income_", "", colnames(income))We plot individual wage mobility time series for three workers. The persistence of belonging to a certain wage class is obvious for any specific person.

set.seed(1)

index <- sample(nrow(income), 3)

for (i in index) {

plot(as.integer(colnames(income)), income[i, ] - 1,

main = paste("Person", i), pch = 19, ylim = c(0, 5),

xlab = "Year", ylab = "Income class")

}

Example 7.14: Wage mobility data – comparing wage mobility of men and women

We transform the data to obtain for each worker the matrix which contains the number of transitions from one class to the other, i.e., the matrix with values .

getTransitions <- function(x, classes) {

transitions <- matrix(0, length(classes), length(classes))

for (i in seq_len(length(x) - 1)) {

transitions[x[i], x[i + 1]] <- transitions[x[i], x[i + 1]] + 1

}

dimnames(transitions) <- list(from = classes, to = classes)

transitions

}

income_transitions <-

lapply(seq_len(nrow(income)),

function(i) getTransitions(income[i, ], classes = 0:5))Based on the transition matrices, the total transitions between the wage categories for female and male workers can be obtained.

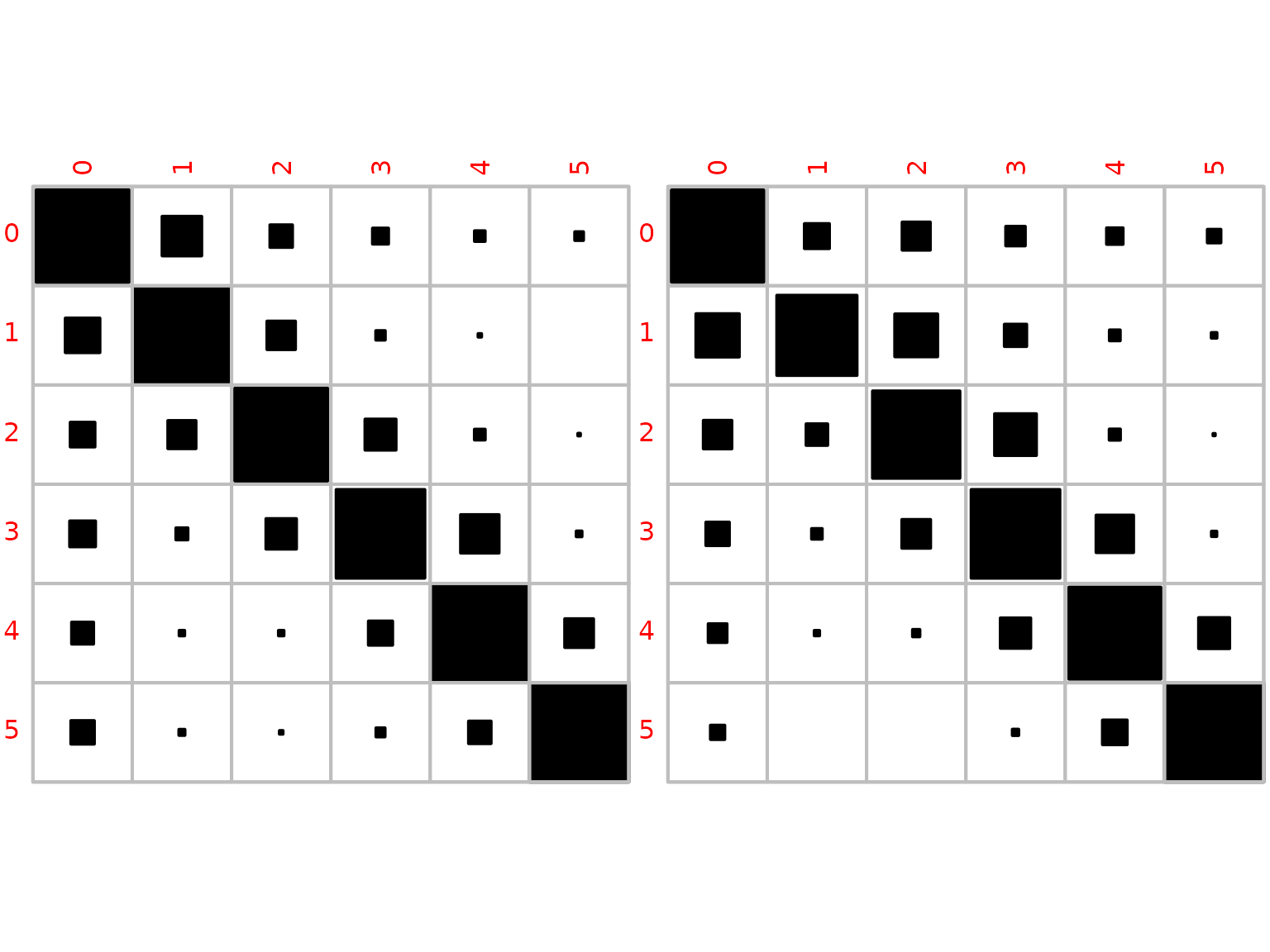

N_female <- Reduce("+", income_transitions[labor$female])

N_male <- Reduce("+", income_transitions[!labor$female])

knitr::kable(N_female)| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0 | 1651 | 300 | 97 | 49 | 22 | 15 |

| 1 | 223 | 1682 | 151 | 17 | 3 | 1 |

| 2 | 74 | 96 | 1056 | 117 | 14 | 1 |

| 3 | 48 | 10 | 67 | 574 | 107 | 2 |

| 4 | 37 | 2 | 2 | 45 | 717 | 64 |

| 5 | 24 | 1 | 0 | 3 | 22 | 446 |

knitr::kable(N_male)| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0 | 1655 | 121 | 153 | 74 | 53 | 36 |

| 1 | 89 | 307 | 87 | 23 | 5 | 1 |

| 2 | 98 | 56 | 926 | 211 | 15 | 1 |

| 3 | 100 | 21 | 150 | 1433 | 255 | 6 |

| 4 | 73 | 7 | 12 | 191 | 1755 | 199 |

| 5 | 50 | 2 | 2 | 11 | 147 | 2391 |

We obtain posterior mean estimates based on a uniform prior.

mean_xi_female <- (1 + N_female) / rowSums(1 + N_female)

mean_xi_male <- (1 + N_male) / rowSums(1 + N_male)

knitr::kable(mean_xi_female, digits = 3)| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0 | 0.772 | 0.141 | 0.046 | 0.023 | 0.011 | 0.007 |

| 1 | 0.108 | 0.808 | 0.073 | 0.009 | 0.002 | 0.001 |

| 2 | 0.055 | 0.071 | 0.775 | 0.087 | 0.011 | 0.001 |

| 3 | 0.060 | 0.014 | 0.084 | 0.706 | 0.133 | 0.004 |

| 4 | 0.044 | 0.003 | 0.003 | 0.053 | 0.822 | 0.074 |

| 5 | 0.050 | 0.004 | 0.002 | 0.008 | 0.046 | 0.890 |

knitr::kable(mean_xi_male, digits = 3)| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0 | 0.789 | 0.058 | 0.073 | 0.036 | 0.026 | 0.018 |

| 1 | 0.174 | 0.595 | 0.170 | 0.046 | 0.012 | 0.004 |

| 2 | 0.075 | 0.043 | 0.706 | 0.161 | 0.012 | 0.002 |

| 3 | 0.051 | 0.011 | 0.077 | 0.728 | 0.130 | 0.004 |

| 4 | 0.033 | 0.004 | 0.006 | 0.086 | 0.783 | 0.089 |

| 5 | 0.020 | 0.001 | 0.001 | 0.005 | 0.057 | 0.917 |

We also visualize the posterior mean estimates for women and men.

corrplot::corrplot(mean_xi_female, method = "square", is.corr = FALSE,

col = 1, cl.pos = "n", col.lim = c(0, 1.5))

corrplot::corrplot(mean_xi_male, method = "square", is.corr = FALSE,

col = 1, cl.pos = "n", col.lim = c(0, 1.5))

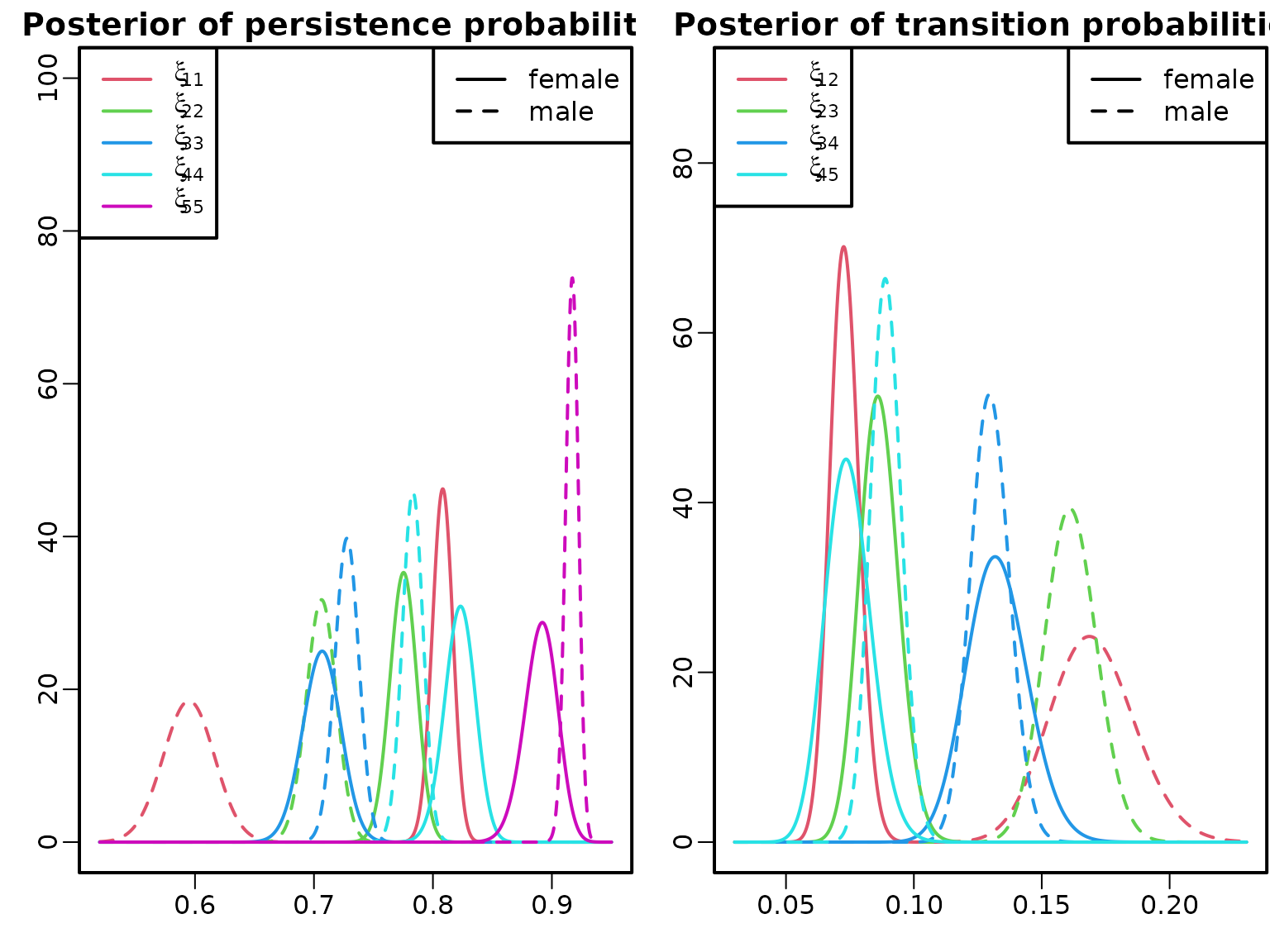

We compare the posterior densities of various transition probabilities for women and men.

plot(c(0.52, 0.95), c(0, 100), type = "n", xlab = "", ylab = "",

main = "Posterior of persistence probabilities")

pers_female <- cbind(diag(1 + N_female),

rowSums(1 + N_female) - diag(1 + N_female))

pers_male <- cbind(diag(1 + N_male),

rowSums(1 + N_male) - diag(1 + N_male))

for (i in 2:6) {

curve(dbeta(x, pers_female[i, 1], pers_female[i, 2]),

col = i, add = TRUE, n = 1001, lty = 1)

curve(dbeta(x, pers_male[i, 1], pers_male[i, 2]),

col = i, add = TRUE, n = 1001, lty = 2)

}

legend("topleft", col = 2:6, lty = 1,

legend = sapply(2:6, function(i)

substitute(xi[i], list(i = (i-1) * 11))))

legend("topright", col = 1, lty = 1:2,

legend = c("female", "male"))

plot(c(0.03, 0.23), c(0, 90), type = "n", xlab = "", ylab = "",

main = "Posterior of selected transition probabilities")

trans_female <- cbind((1 + N_female)[cbind(1:5, 2:6)],

rowSums(1 + N_female)[1:5] - (1 + N_female)[cbind(1:5, 2:6)])

trans_male <- cbind((1 + N_male)[cbind(1:5, 2:6)],

rowSums(1 + N_male)[1:5] - (1 + N_male)[cbind(1:5, 2:6)])

for (i in 2:5) {

curve(dbeta(x, trans_female[i, 1], trans_female[i, 2]),

col = i, add = TRUE, n = 1001, lty = 1)

curve(dbeta(x, trans_male[i, 1], trans_male[i, 2]),

col = i, add = TRUE, n = 1001, lty = 2)

}

legend("topleft", col = 2:5, lty = 1,

legend = sapply(2:5, function(i)

substitute(xi[i], list(i = c(01, 12, 23, 34, 45)[i]))))

legend("topright", col = 1, lty = 1:2,

legend = c("female", "male"))

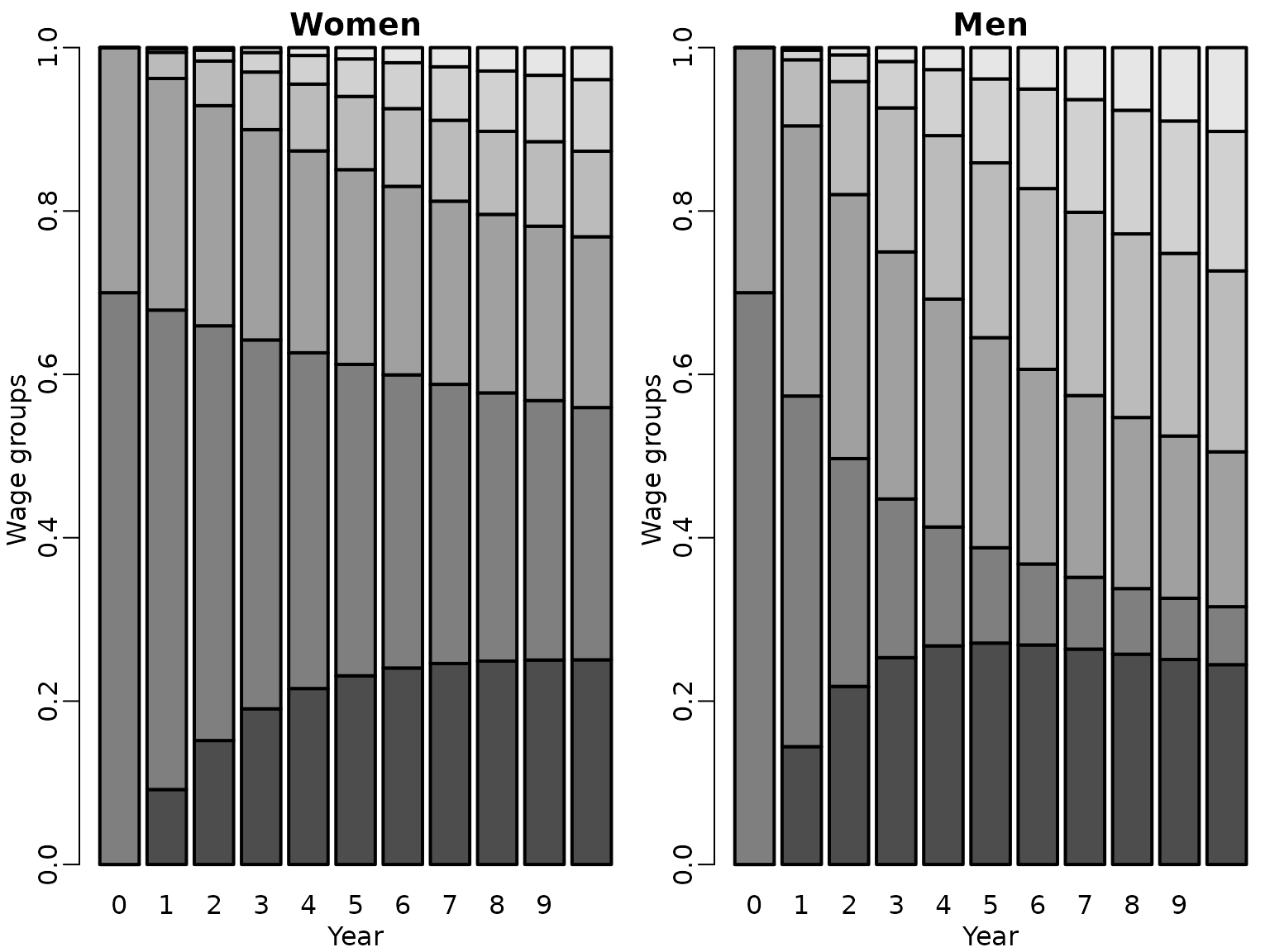

Example 7.15: Wage mobility data – long run

We assume that both men and women start out in the labor market with the same wage distribution, where 70% start in wage category 1 and 30% in wage category 2, i.e., . We compare the evolution of the estimated wage distribution over the first ten years for females and males.

eta_0 <- c(0, 0.7, 0.3, 0, 0, 0)

eta_hat_male_t <- eta_hat_female_t <-

matrix(NA_real_, nrow = 6, ncol = 11,

dimnames = list(0:5, 0:10))

eta_hat_male_t[, 1] <- eta_hat_female_t[, 1] <- eta_0

for (i in 2:11) {

eta_hat_female_t[, i] <- eta_hat_female_t[, i - 1] %*% mean_xi_female

eta_hat_male_t[, i] <- eta_hat_male_t[, i - 1] %*% mean_xi_male

}

barplot(eta_hat_female_t, main = "Women", xlab = "Year", ylab = "Wage groups")

barplot(eta_hat_male_t, main = "Men", xlab = "Year", ylab = "Wage groups")

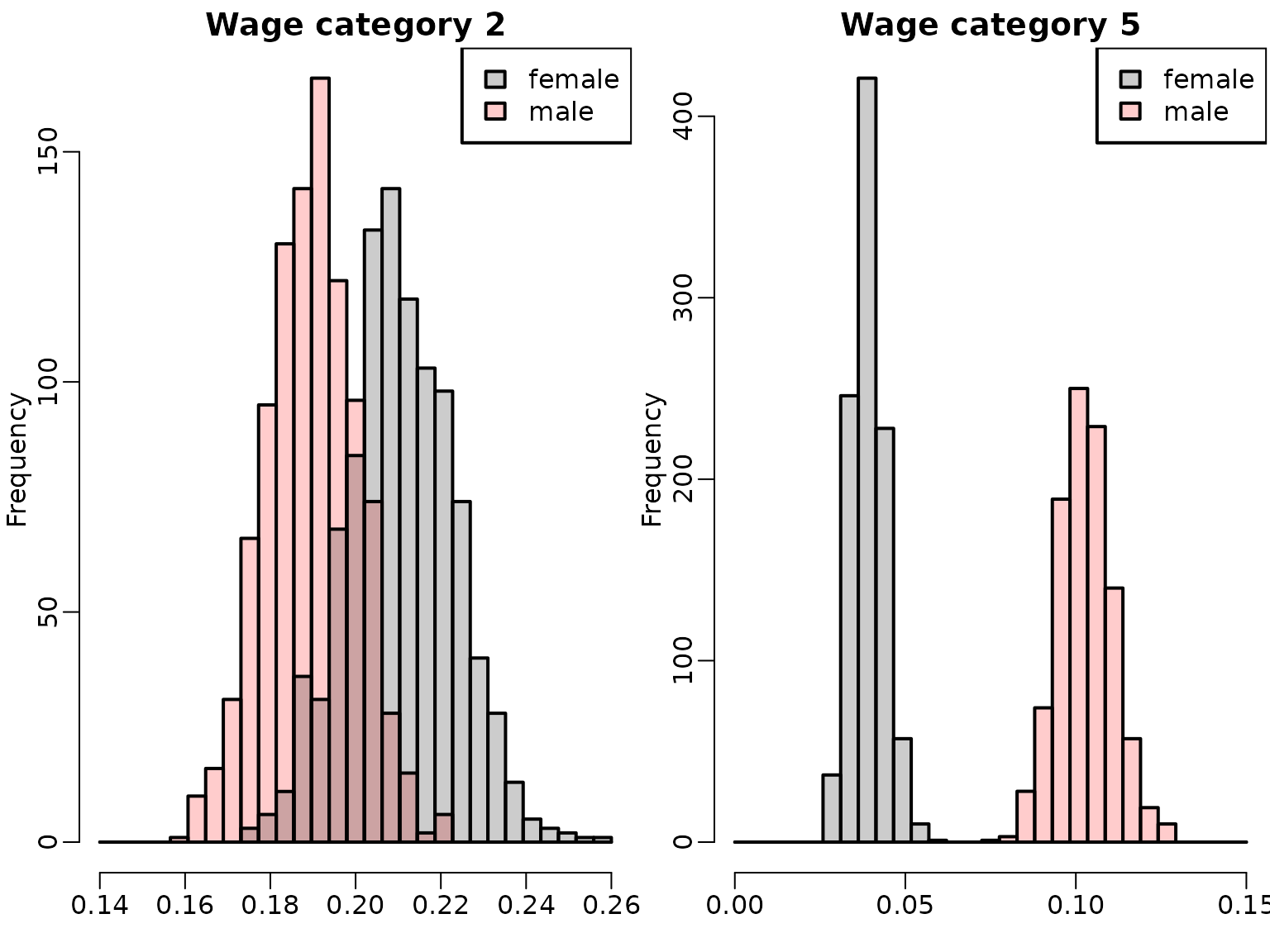

We inspect the posterior distributions of for wage category 2 (left-hand side) versus for wage category 5 (right-hand side) in year for females and males.

M <- 1000

xi_female <- replicate(M, apply(1 + N_female, 1,

function(alpha) rdirichlet(1, alpha)))

xi_male <- replicate(M, apply(1 + N_male, 1,

function(alpha) rdirichlet(1, alpha)))

eta_male_t <- eta_female_t <- matrix(eta_0, nrow = M, ncol = 6,

byrow = TRUE)

for (i in 2:11) {

eta_female_t <- t(sapply(1:M, function(m)

xi_female[, , m] %*% eta_female_t[m, ]))

eta_male_t <- t(sapply(1:M, function(m)

xi_male[, , m] %*% eta_male_t[m, ]))

}

breaks <- seq(0.14, 0.26, length.out = 30)

hist(eta_male_t[, 3], breaks = breaks, xlim = range(breaks),

col = rgb(1, 0, 0, 0.2), xlab = "", main = "Wage category 2")

hist(eta_female_t[, 3], breaks = breaks, col = rgb(0, 0, 0, 0.2), add = TRUE)

legend("topright", c("female", "male"), fill = rgb(c(0, 1), 0, 0, 0.2))

breaks <- seq(0, 0.15, length.out = 30)

hist(eta_female_t[, 6], breaks = breaks, xlim = range(breaks),

col = rgb(0, 0, 0, 0.2), xlab = "", main = "Wage category 5")

hist(eta_male_t[, 6], breaks = breaks,

col = rgb(1, 0, 0, 0.2), add = TRUE)

legend("topright", c("female", "male"), fill = rgb(c(0, 1), 0, 0, 0.2))