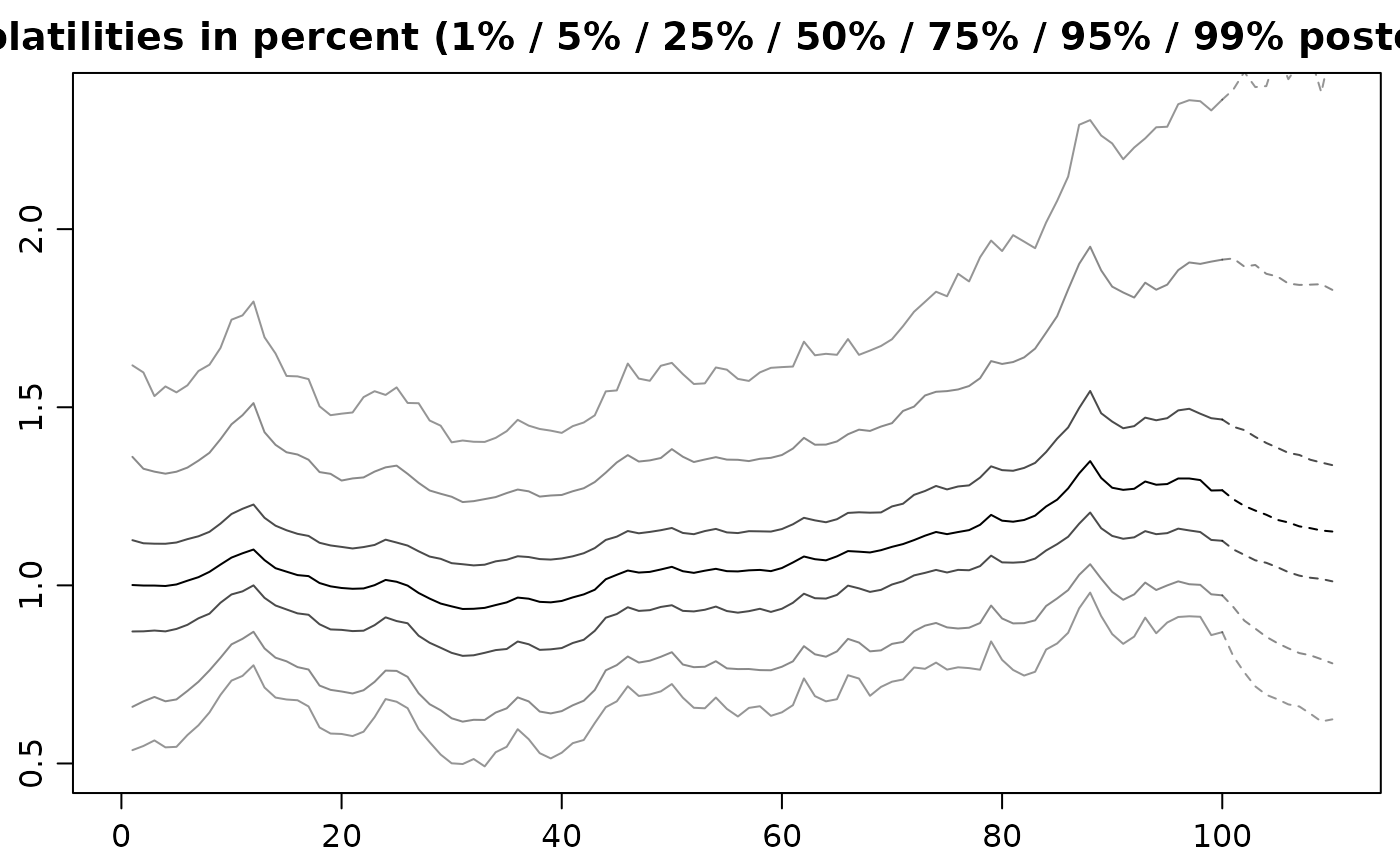

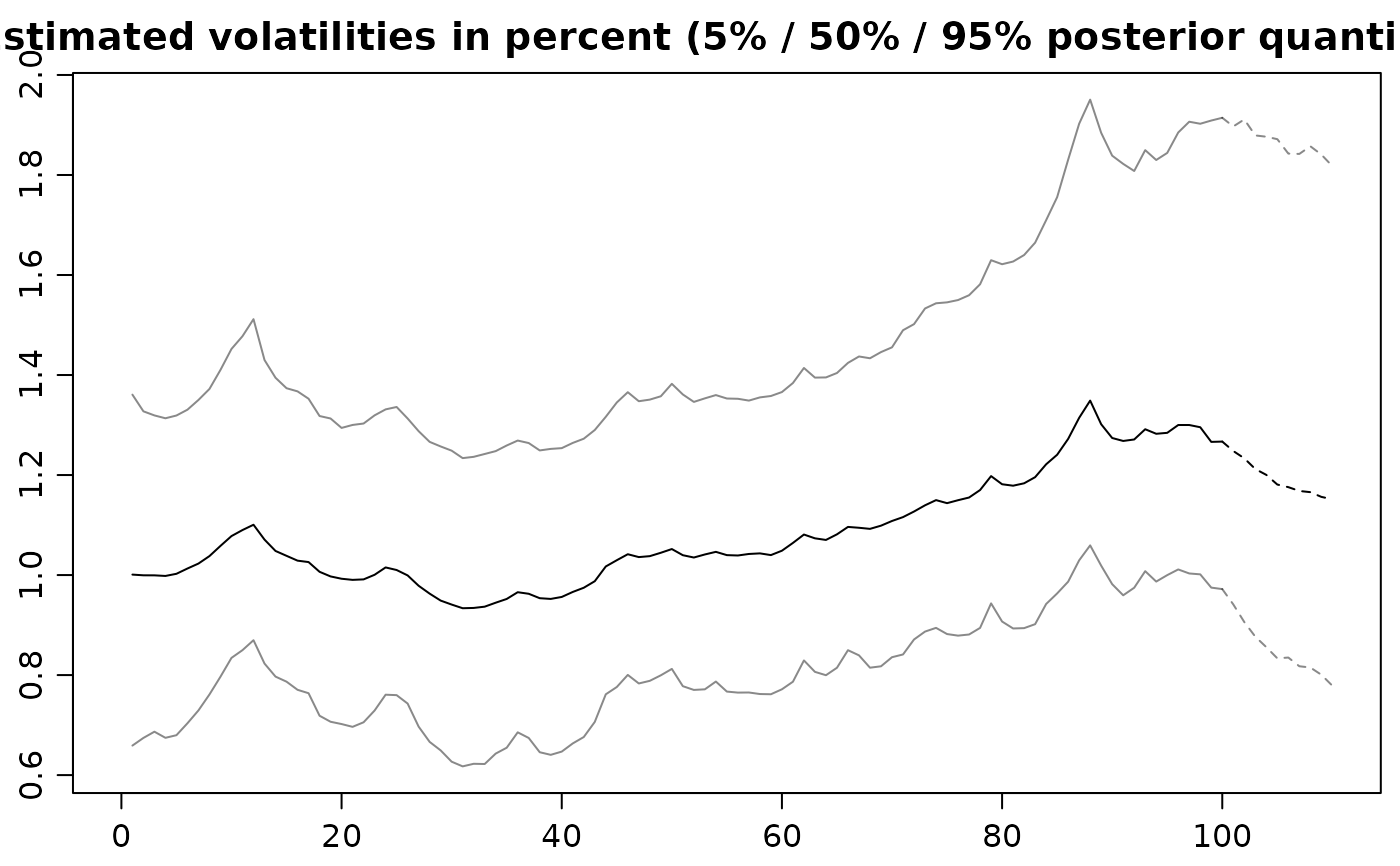

Displays quantiles of the posterior distribution of the volatilities over time as well as predictive distributions of future volatilities.

Arguments

- x

svdrawsobject.- forecast

nonnegative integer or object of class

svpredict, as returned bypredict.svdraws. If an integer greater than 0 is provided,predict.svdrawsis invoked to obtain theforecast-step-ahead prediction. The default value is0.- dates

vector of length

ncol(x$latent), providing optional dates for labeling the x-axis. The default value isNULL; in this case, the axis will be labeled with numbers.- show0

logical value, indicating whether the initial volatility

exp(h_0/2)should be displayed. The default value isFALSE. Only available for inputsxof classsvdraws.- forecastlty

vector of line type values (see

par) used for plotting quantiles of predictive distributions. The default valueNULLresults in dashed lines.- tcl

The length of tick marks as a fraction of the height of a line of text. See

parfor details. The default value is-0.4, which results in slightly shorter tick marks than usual.- mar

numerical vector of length 4, indicating the plot margins. See

parfor details. The default value isc(1.9, 1.9, 1.9, 0.5), which is slightly smaller than the R-defaults.- mgp

numerical vector of length 3, indicating the axis and label positions. See

parfor details. The default value isc(2, 0.6, 0), which is slightly smaller than the R-defaults.- simobj

object of class

svsimas returned by the SV simulation functionsvsim. If provided, “true” data generating values will be added to the plot(s).- newdata

corresponds to parameter

newdatainpredict.svdraws. Only ifforecastis a positive integer andpredict.svdrawsneeds anewdataobject. Corresponds to input parameterdesignmatrixinsvsample. A matrix of regressors with number of rows equal to parameterforecast.- ...

further arguments are passed on to the invoked

ts.plotfunction.

Value

Called for its side effects. Returns argument x invisibly.

Note

In case you want different quantiles to be plotted, use

updatesummary on the svdraws object first. An example

of doing so is given below.

See also

Examples

## Simulate a short and highly persistent SV process

sim <- svsim(100, mu = -10, phi = 0.99, sigma = 0.2)

## Obtain 5000 draws from the sampler (that's not a lot)

draws <- svsample(sim$y, draws = 5000, burnin = 100,

priormu = c(-10, 1), priorphi = c(20, 1.5),

priorsigma = 0.2)

#> Done!

#> Summarizing posterior draws...

## Plot the latent volatilities and some forecasts

volplot(draws, forecast = 10)

## Re-plot with different quantiles

newquants <- c(0.01, 0.05, 0.25, 0.5, 0.75, 0.95, 0.99)

draws <- updatesummary(draws, quantiles = newquants)

volplot(draws, forecast = 10)

## Re-plot with different quantiles

newquants <- c(0.01, 0.05, 0.25, 0.5, 0.75, 0.95, 0.99)

draws <- updatesummary(draws, quantiles = newquants)

volplot(draws, forecast = 10)