Markov Chain Monte Carlo (MCMC) Sampling for the Stochastic Volatility (SV) Model

Source:R/wrappers.R

svsample.Rdsvsample simulates from the joint posterior distribution of the SV

parameters mu, phi, sigma (and potentially nu and rho),

along with the latent log-volatilities h_0,...,h_n and returns the

MCMC draws. If a design matrix is provided, simple Bayesian regression can

also be conducted. For similar functionality with a formula interface,

see svlm.

svsample(

y,

draws = 10000,

burnin = 1000,

designmatrix = NA,

priormu = c(0, 100),

priorphi = c(5, 1.5),

priorsigma = 1,

priornu = 0,

priorrho = NA,

priorbeta = c(0, 10000),

priorlatent0 = "stationary",

priorspec = NULL,

thin = 1,

thinpara = thin,

thinlatent = thin,

keeptime = "all",

quiet = FALSE,

startpara = NULL,

startlatent = NULL,

parallel = c("no", "multicore", "snow"),

n_cpus = 1L,

cl = NULL,

n_chains = 1L,

print_progress = "automatic",

expert = NULL,

...

)

svtsample(

y,

draws = 10000,

burnin = 1000,

designmatrix = NA,

priormu = c(0, 100),

priorphi = c(5, 1.5),

priorsigma = 1,

priornu = 0.1,

priorrho = NA,

priorbeta = c(0, 10000),

priorlatent0 = "stationary",

priorspec = NULL,

thin = 1,

thinpara = thin,

thinlatent = thin,

keeptime = "all",

quiet = FALSE,

startpara = NULL,

startlatent = NULL,

parallel = c("no", "multicore", "snow"),

n_cpus = 1L,

cl = NULL,

n_chains = 1L,

print_progress = "automatic",

expert = NULL,

...

)

svlsample(

y,

draws = 20000,

burnin = 2000,

designmatrix = NA,

priormu = c(0, 100),

priorphi = c(5, 1.5),

priorsigma = 1,

priornu = 0,

priorrho = c(4, 4),

priorbeta = c(0, 10000),

priorlatent0 = "stationary",

priorspec = NULL,

thin = 1,

thinpara = thin,

thinlatent = thin,

keeptime = "all",

quiet = FALSE,

startpara = NULL,

startlatent = NULL,

parallel = c("no", "multicore", "snow"),

n_cpus = 1L,

cl = NULL,

n_chains = 1L,

print_progress = "automatic",

expert = NULL,

...

)

svtlsample(

y,

draws = 20000,

burnin = 2000,

designmatrix = NA,

priormu = c(0, 100),

priorphi = c(5, 1.5),

priorsigma = 1,

priornu = 0.1,

priorrho = c(4, 4),

priorbeta = c(0, 10000),

priorlatent0 = "stationary",

priorspec = NULL,

thin = 1,

thinpara = thin,

thinlatent = thin,

keeptime = "all",

quiet = FALSE,

startpara = NULL,

startlatent = NULL,

parallel = c("no", "multicore", "snow"),

n_cpus = 1L,

cl = NULL,

n_chains = 1L,

print_progress = "automatic",

expert = NULL,

...

)

svsample2(

y,

draws = 10000,

burnin = 1000,

designmatrix = NA,

priormu = c(0, 100),

priorphi = c(5, 1.5),

priorsigma = 1,

priornu = 0,

priorrho = NA,

priorbeta = c(0, 10000),

priorlatent0 = "stationary",

thinpara = 1,

thinlatent = 1,

keeptime = "all",

quiet = FALSE,

startpara = NULL,

startlatent = NULL

)Arguments

- y

numeric vector containing the data (usually log-returns), which must not contain zeros. Alternatively,

ycan be ansvsimobject. In this case, the returns will be extracted and a message is signalled.- draws

single number greater or equal to 1, indicating the number of draws after burn-in (see below). Will be automatically coerced to integer. The default value is 10000.

- burnin

single number greater or equal to 0, indicating the number of draws discarded as burn-in. Will be automatically coerced to integer. The default value is 1000.

- designmatrix

regression design matrix for modeling the mean. Must have

length(y)rows. Alternatively,designmatrixmay be a string of the form"arX", whereXis a nonnegative integer. To fit a constant mean model, usedesignmatrix = "ar0"(which is equivalent todesignmatrix = matrix(1, nrow = length(y))). To fit an AR(1) model, usedesignmatrix = "ar1", and so on. If some elements ofdesignmatrixareNA, the mean is fixed to zero (pre-1.2.0 behavior of stochvol).- priormu

numeric vector of length 2, indicating mean and standard deviation for the Gaussian prior distribution of the parameter

mu, the level of the log-volatility. The default value isc(0, 100), which constitutes a practically uninformative prior for common exchange rate datasets, stock returns and the like.- priorphi

numeric vector of length 2, indicating the shape parameters for the Beta prior distribution of the transformed parameter

(phi + 1) / 2, wherephidenotes the persistence of the log-volatility. The default value isc(5, 1.5), which constitutes a prior that puts some belief in a persistent log-volatility but also encompasses the region wherephiis around 0.- priorsigma

single positive real number, which stands for the scaling of the transformed parameter

sigma^2, wheresigmadenotes the volatility of log-volatility. More precisely,sigma^2 ~ priorsigma * chisq(df = 1). The default value is1, which constitutes a reasonably vague prior for many common exchange rate datasets, stock returns and the like.- priornu

single non-negative number, indicating the rate parameter for the exponential prior distribution of the parameter; can be

Infnu, the degrees-of-freedom parameter of the conditional innovations t-distribution. The default value is0, fixing the degrees-of-freedom to infinity. This corresponds to conditional standard normal innovations, the pre-1.1.0 behavior of stochvol.- priorrho

either

NAfor the no-leverage case or a numeric vector of length 2 that specify the beta prior distribution for(rho+1)/2- priorbeta

numeric vector of length 2, indicating the mean and standard deviation of the Gaussian prior for the regression parameters. The default value is

c(0, 10000), which constitutes a very vague prior for many common datasets. Not used ifdesignmatrixisNA.- priorlatent0

either a single non-negative number or the string

'stationary'(the default, also the behavior before version 1.3.0). Whenpriorlatent0is equal to'stationary', the stationary distribution of the latent AR(1)-process is used as the prior for the initial log-volatilityh_0. Whenpriorlatent0is equal to a number \(B\), we have \(h_0 \sim N(\mu, B\sigma^2)\) a priori.- priorspec

in case one needs different prior distributions than the ones specified by

priormu,...,priorrho, apriorspecobject can be supplied here. A smart constructor for this usecase is specify_priors.- thin

single number greater or equal to 1, coercible to integer. Every

thinparath parameter and latent draw is kept and returned. The default value is 1, corresponding to no thinning of the parameter draws i.e. every draw is stored.- thinpara

single number greater or equal to 1, coercible to integer. Every

thinparath parameter draw is kept and returned. The default value isthin.- thinlatent

single number greater or equal to 1, coercible to integer. Every

thinlatentth latent variable draw is kept and returned. The default value isthin- keeptime

Either 'all' (the default) or 'last'. Indicates which latent volatility draws should be stored.

- quiet

logical value indicating whether the progress bar and other informative output during sampling should be omitted. The default value is

FALSE, implying verbose output.- startpara

optional named list, containing the starting values for the parameter draws. If supplied,

startparamay contain elements namedmu,phi,sigma,nu,rho,beta, andlatent0. The default value is equal to the prior mean. In case of parallel execution withclprovided,startparacan be a list of named lists that initialize the parallel chains.- startlatent

optional vector of length

length(y), containing the starting values for the latent log-volatility draws. The default value isrep(-10, length(y)). In case of parallel execution withclprovided,startlatentcan be a list of numeric vectors that initialize the parallel chains.- parallel

optional one of

"no"(default),"multicore", or"snow", indicating what type of parallellism is to be applied. Option"multicore"is not available on Windows.- n_cpus

optional positive integer, the number of CPUs to be used in case of parallel computations. Defaults to

1L. Ignored if parameterclis supplied andparallel != "snow".- cl

optional so-called SNOW cluster object as implemented in package

parallel. Ignored unlessparallel == "snow".- n_chains

optional positive integer specifying the number of independent MCMC chains

- print_progress

optional one of

"automatic","progressbar", or"iteration", controls the output. Ignored ifquietisTRUE.- expert

optional named list of expert parameters. For most applications, the default values probably work best. Interested users are referred to the literature provided in the References section. If

expertis provided, it may contain the following named elements:- interweave

Logical value. If

TRUE(the default), then ancillarity-sufficiency interweaving strategy (ASIS) is applied to improve on the sampling efficiency for the parameters. Otherwise one parameterization is used.- correct_model_misspecification

Logical value. If

FALSE(the default), then auxiliary mixture sampling is used to sample the latent states. IfTRUE, extra computations are made to correct for model misspecification either ex-post by reweighting or on-line using a Metropolis-Hastings step.

- ...

Any extra arguments will be forwarded to

updatesummary, controlling the type of statistics calculated for the posterior draws.

Value

The value returned is a list object of class svdraws holding

- para

mcmc.listobject containing the parameter draws from the posterior distribution.- latent

mcmc.listobject containing the latent instantaneous log-volatility draws from the posterior distribution.- latent0

mcmc.listobject containing the latent initial log-volatility draws from the posterior distribution.- tau

mcmc.listobject containing the latent variance inflation factors for the sampler with conditional t-innovations (optional).- beta

mcmc.listobject containing the regression coefficient draws from the posterior distribution (optional).- y

the left hand side of the observation equation, usually the argument

y. In case of an AR(k) specification, the firstkelements are removed.- runtime

proc_timeobject containing the run time of the sampler.- priors

a

priorspecobject containing the parameter values of the prior distributions formu,phi,sigma,nu,rho, andbetas, and the variance of specification forlatent0.- thinning

listcontaining the thinning parameters, i.e. the argumentsthinpara,thinlatentandkeeptime.- summary

listcontaining a collection of summary statistics of the posterior draws forpara,latent, andlatent0.- meanmodel

charactercontaining information about howdesignmatrixwas employed.

To display the output, use print, summary and plot. The

print method simply prints the posterior draws (which is very likely

a lot of output); the summary method displays the summary statistics

currently stored in the object; the plot method

plot.svdraws gives a graphical overview of the posterior

distribution by calling volplot, traceplot and

densplot and displaying the results on a single page.

Details

Functions svtsample, svlsample, and svtlsample are

wrappers around svsample with convenient default values for the SV

model with t-errors, leverage, and both t-errors and leverage, respectively.

For details concerning the algorithm please see the paper by Kastner and Frühwirth-Schnatter (2014) and Hosszejni and Kastner (2019).

Note

If y contains zeros, you might want to consider de-meaning your

returns or use designmatrix = "ar0".

svsample2 is deprecated.

References

Kastner, G. and Frühwirth-Schnatter, S. (2014). Ancillarity-sufficiency interweaving strategy (ASIS) for boosting MCMC estimation of stochastic volatility models. Computational Statistics & Data Analysis, 76, 408–423, doi:10.1016/j.csda.2013.01.002 .

Hosszejni, D. and Kastner, G. (2019). Approaches Toward the Bayesian Estimation of the Stochastic Volatility Model with Leverage. Springer Proceedings in Mathematics & Statistics, 296, 75–83, doi:10.1007/978-3-030-30611-3_8 .

See also

Examples

###############

# Full examples

###############

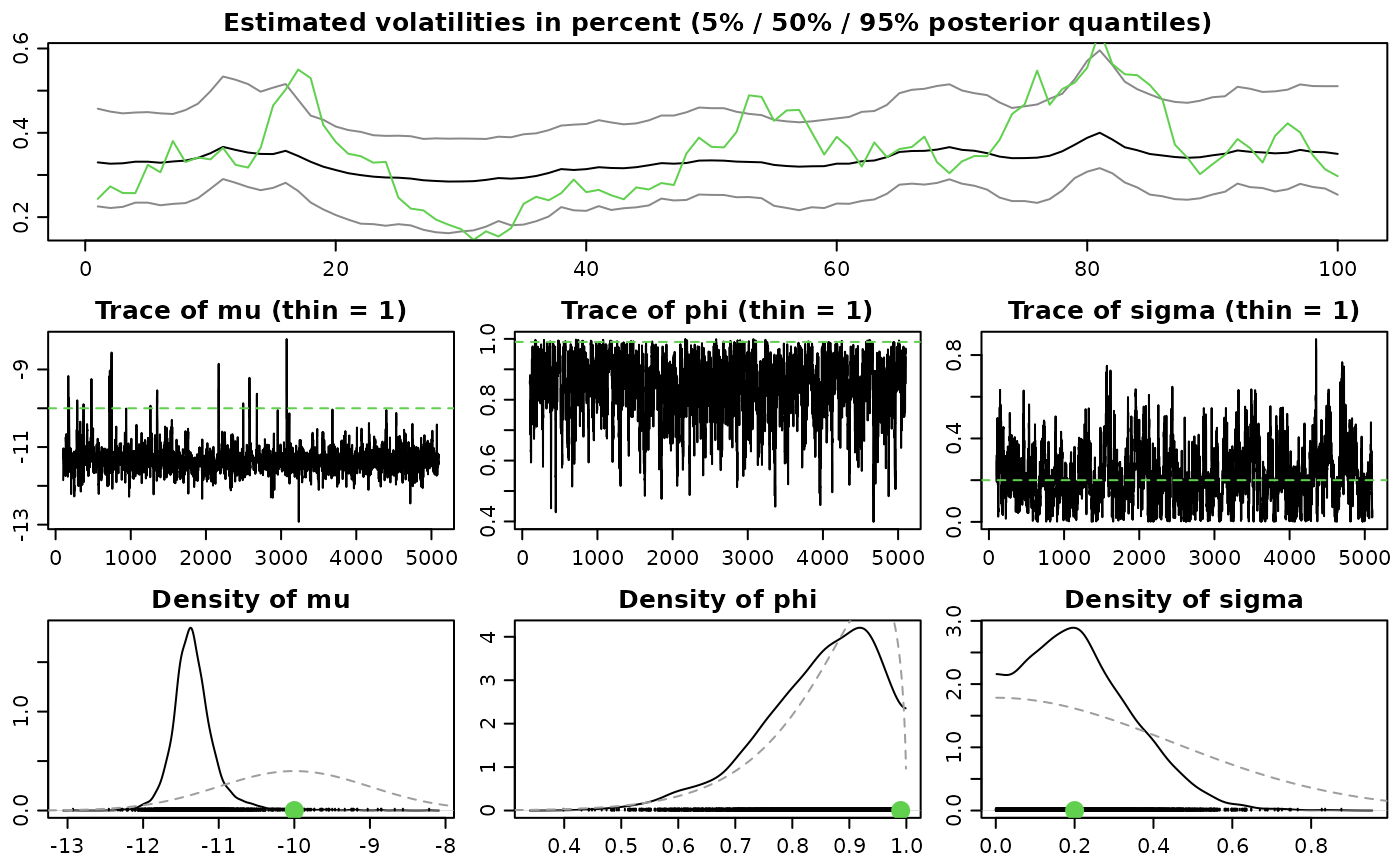

# Example 1

## Simulate a short and highly persistent SV process

sim <- svsim(100, mu = -10, phi = 0.99, sigma = 0.2)

## Obtain 5000 draws from the sampler (that's not a lot)

draws <-

svsample(sim, draws = 5000, burnin = 100,

priormu = c(-10, 1), priorphi = c(20, 1.5), priorsigma = 0.2)

#> Extracted data vector from 'svsim'-object.

#> Done!

#> Summarizing posterior draws...

## Check out the results

summary(draws)

#>

#> Summary of 'svdraws' object

#>

#> Prior distributions:

#> mu ~ Normal(mean = -10, sd = 1)

#> (phi+1)/2 ~ Beta(a = 20, b = 1.5)

#> sigma^2 ~ Gamma(shape = 0.5, rate = 2.5)

#> nu ~ Infinity

#> rho ~ Constant(value = 0)

#>

#> Stored 5000 MCMC draws after a burn-in of 100.

#> No thinning.

#>

#> Posterior draws of SV parameters (thinning = 1):

#> mean sd 5% 50% 95% ESS

#> mu -10.1400 0.23657 -1.0e+01 -10.1445 -9.7614 999

#> phi 0.8455 0.10712 6.4e-01 0.8676 0.9781 470

#> sigma 0.1616 0.11700 1.5e-02 0.1416 0.3759 355

#> exp(mu/2) 0.0063 0.00077 5.3e-03 0.0063 0.0076 999

#> sigma^2 0.0398 0.05906 2.4e-04 0.0200 0.1413 355

#>

plot(draws)

#> Simulation object extracted from input

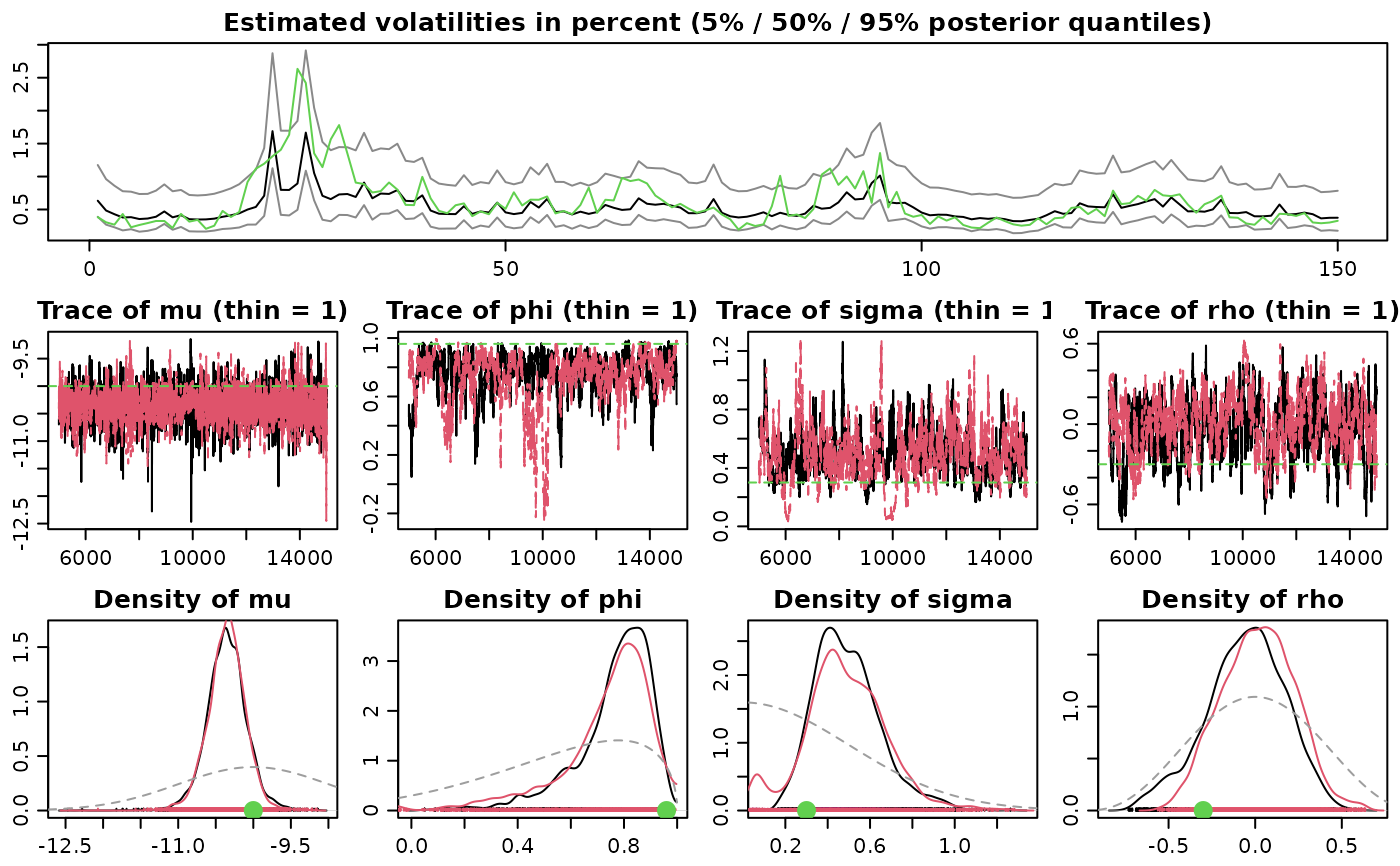

# \donttest{

# Example 2

## Simulate an asymmetric and conditionally heavy-tailed SV process

sim <- svsim(150, mu = -10, phi = 0.96, sigma = 0.3, nu = 10, rho = -0.3)

## Obtain 10000 draws from the sampler

## Use more advanced prior settings

## Run two parallel MCMC chains

advanced_draws <-

svsample(sim, draws = 10000, burnin = 5000,

priorspec = specify_priors(mu = sv_normal(-10, 1),

sigma2 = sv_gamma(0.5, 2),

rho = sv_beta(4, 4),

nu = sv_constant(5)),

parallel = "snow", n_chains = 2, n_cpus = 2)

#> Extracted data vector from 'svsim'-object.

#> Done!

#> Summarizing posterior draws...

## Check out the results

summary(advanced_draws)

#>

#> Summary of 'svdraws' object

#>

#> Prior distributions:

#> mu ~ Normal(mean = -10, sd = 1)

#> (phi+1)/2 ~ Beta(a = 5, b = 1.5)

#> sigma^2 ~ Gamma(shape = 0.5, rate = 2)

#> nu ~ Constant(value = 5)

#> rho ~ Beta(a = 4, b = 4)

#>

#> Stored 10000 MCMC draws after a burn-in of 5000.

#> No thinning.

#>

#> Posterior draws of SV parameters (thinning = 1):

#> mean sd 5% 50% 95% ESS

#> mu -9.8968 0.5676 -10.8475 -9.8698 -9.017 2561

#> phi 0.9314 0.0385 0.8574 0.9382 0.982 455

#> sigma 0.4948 0.1211 0.3093 0.4884 0.707 233

#> rho -0.3157 0.1648 -0.5679 -0.3275 -0.028 406

#> exp(mu/2) 0.0074 0.0021 0.0044 0.0072 0.011 2561

#> sigma^2 0.2595 0.1277 0.0956 0.2386 0.499 233

#>

plot(advanced_draws)

#> Simulation object extracted from input

# \donttest{

# Example 2

## Simulate an asymmetric and conditionally heavy-tailed SV process

sim <- svsim(150, mu = -10, phi = 0.96, sigma = 0.3, nu = 10, rho = -0.3)

## Obtain 10000 draws from the sampler

## Use more advanced prior settings

## Run two parallel MCMC chains

advanced_draws <-

svsample(sim, draws = 10000, burnin = 5000,

priorspec = specify_priors(mu = sv_normal(-10, 1),

sigma2 = sv_gamma(0.5, 2),

rho = sv_beta(4, 4),

nu = sv_constant(5)),

parallel = "snow", n_chains = 2, n_cpus = 2)

#> Extracted data vector from 'svsim'-object.

#> Done!

#> Summarizing posterior draws...

## Check out the results

summary(advanced_draws)

#>

#> Summary of 'svdraws' object

#>

#> Prior distributions:

#> mu ~ Normal(mean = -10, sd = 1)

#> (phi+1)/2 ~ Beta(a = 5, b = 1.5)

#> sigma^2 ~ Gamma(shape = 0.5, rate = 2)

#> nu ~ Constant(value = 5)

#> rho ~ Beta(a = 4, b = 4)

#>

#> Stored 10000 MCMC draws after a burn-in of 5000.

#> No thinning.

#>

#> Posterior draws of SV parameters (thinning = 1):

#> mean sd 5% 50% 95% ESS

#> mu -9.8968 0.5676 -10.8475 -9.8698 -9.017 2561

#> phi 0.9314 0.0385 0.8574 0.9382 0.982 455

#> sigma 0.4948 0.1211 0.3093 0.4884 0.707 233

#> rho -0.3157 0.1648 -0.5679 -0.3275 -0.028 406

#> exp(mu/2) 0.0074 0.0021 0.0044 0.0072 0.011 2561

#> sigma^2 0.2595 0.1277 0.0956 0.2386 0.499 233

#>

plot(advanced_draws)

#> Simulation object extracted from input

# Example 3

## AR(1) structure for the mean

data(exrates)

len <- 3000

ahead <- 100

y <- head(exrates$USD, len)

## Fit AR(1)-SVL model to EUR-USD exchange rates

res <- svsample(y, designmatrix = "ar1")

#> Done!

#> Summarizing posterior draws...

## Use predict.svdraws to obtain predictive distributions

preddraws <- predict(res, steps = ahead)

## Calculate predictive quantiles

predquants <- apply(predy(preddraws), 2, quantile, c(.1, .5, .9))

## Visualize

expost <- tail(head(exrates$USD, len+ahead), ahead)

ts.plot(y, xlim = c(length(y)-4*ahead, length(y)+ahead),

ylim = range(c(predquants, expost, tail(y, 4*ahead))))

for (i in 1:3) {

lines((length(y)+1):(length(y)+ahead), predquants[i,],

col = 3, lty = c(2, 1, 2)[i])

}

lines((length(y)+1):(length(y)+ahead), expost,

col = 2)

# Example 3

## AR(1) structure for the mean

data(exrates)

len <- 3000

ahead <- 100

y <- head(exrates$USD, len)

## Fit AR(1)-SVL model to EUR-USD exchange rates

res <- svsample(y, designmatrix = "ar1")

#> Done!

#> Summarizing posterior draws...

## Use predict.svdraws to obtain predictive distributions

preddraws <- predict(res, steps = ahead)

## Calculate predictive quantiles

predquants <- apply(predy(preddraws), 2, quantile, c(.1, .5, .9))

## Visualize

expost <- tail(head(exrates$USD, len+ahead), ahead)

ts.plot(y, xlim = c(length(y)-4*ahead, length(y)+ahead),

ylim = range(c(predquants, expost, tail(y, 4*ahead))))

for (i in 1:3) {

lines((length(y)+1):(length(y)+ahead), predquants[i,],

col = 3, lty = c(2, 1, 2)[i])

}

lines((length(y)+1):(length(y)+ahead), expost,

col = 2)

# Example 4

## Predicting USD based on JPY and GBP in the mean

data(exrates)

len <- 3000

ahead <- 30

## Calculate log-returns

logreturns <- apply(exrates[, c("USD", "JPY", "GBP")], 2,

function (x) diff(log(x)))

logretUSD <- logreturns[2:(len+1), "USD"]

regressors <- cbind(1, as.matrix(logreturns[1:len, ])) # lagged by 1 day

## Fit SV model to EUR-USD exchange rates

res <- svsample(logretUSD, designmatrix = regressors)

#> Done!

#> Summarizing posterior draws...

## Use predict.svdraws to obtain predictive distributions

predregressors <- cbind(1, as.matrix(logreturns[(len+1):(len+ahead), ]))

preddraws <- predict(res, steps = ahead,

newdata = predregressors)

predprice <- exrates[len+2, "USD"] * exp(t(apply(predy(preddraws), 1, cumsum)))

## Calculate predictive quantiles

predquants <- apply(predprice, 2, quantile, c(.1, .5, .9))

## Visualize

priceUSD <- exrates[3:(len+2), "USD"]

expost <- exrates[(len+3):(len+ahead+2), "USD"]

ts.plot(priceUSD, xlim = c(len-4*ahead, len+ahead+1),

ylim = range(c(expost, predquants, tail(priceUSD, 4*ahead))))

for (i in 1:3) {

lines(len:(len+ahead), c(tail(priceUSD, 1), predquants[i,]),

col = 3, lty = c(2, 1, 2)[i])

}

lines(len:(len+ahead), c(tail(priceUSD, 1), expost),

col = 2)

# Example 4

## Predicting USD based on JPY and GBP in the mean

data(exrates)

len <- 3000

ahead <- 30

## Calculate log-returns

logreturns <- apply(exrates[, c("USD", "JPY", "GBP")], 2,

function (x) diff(log(x)))

logretUSD <- logreturns[2:(len+1), "USD"]

regressors <- cbind(1, as.matrix(logreturns[1:len, ])) # lagged by 1 day

## Fit SV model to EUR-USD exchange rates

res <- svsample(logretUSD, designmatrix = regressors)

#> Done!

#> Summarizing posterior draws...

## Use predict.svdraws to obtain predictive distributions

predregressors <- cbind(1, as.matrix(logreturns[(len+1):(len+ahead), ]))

preddraws <- predict(res, steps = ahead,

newdata = predregressors)

predprice <- exrates[len+2, "USD"] * exp(t(apply(predy(preddraws), 1, cumsum)))

## Calculate predictive quantiles

predquants <- apply(predprice, 2, quantile, c(.1, .5, .9))

## Visualize

priceUSD <- exrates[3:(len+2), "USD"]

expost <- exrates[(len+3):(len+ahead+2), "USD"]

ts.plot(priceUSD, xlim = c(len-4*ahead, len+ahead+1),

ylim = range(c(expost, predquants, tail(priceUSD, 4*ahead))))

for (i in 1:3) {

lines(len:(len+ahead), c(tail(priceUSD, 1), predquants[i,]),

col = 3, lty = c(2, 1, 2)[i])

}

lines(len:(len+ahead), c(tail(priceUSD, 1), expost),

col = 2)

# }

########################

# Further short examples

########################

y <- svsim(50, nu = 10, rho = -0.1)$y

# Supply initial values

res <- svsample(y,

startpara = list(mu = -10, sigma = 1))

#> Done!

#> Summarizing posterior draws...

# \donttest{

# Supply initial values for parallel chains

res <- svsample(y,

startpara = list(list(mu = -10, sigma = 1),

list(mu = -11, sigma = .1, phi = 0.9),

list(mu = -9, sigma = .3, phi = 0.7)),

parallel = "snow", n_chains = 3, n_cpus = 2)

#> Done!

#> Summarizing posterior draws...

# Parallel chains with with a pre-defined cluster object

cl <- parallel::makeCluster(2, "PSOCK", outfile = NULL) # print to console

res <- svsample(y,

parallel = "snow", n_chains = 3, cl = cl)

#> Done!

#> Summarizing posterior draws...

parallel::stopCluster(cl)

# }

# Turn on correction for model misspecification

## Since the approximate model is fast and it is working very

## well in practice, this is turned off by default

res <- svsample(y,

expert = list(correct_model_misspecification = TRUE))

#> Done!

#> Summarizing posterior draws...

#> No computation of effective sample size after re-sampling

print(res)

#>

#> Summary of 'svdraws' object

#>

#> Prior distributions:

#> mu ~ Normal(mean = 0, sd = 100)

#> (phi+1)/2 ~ Beta(a = 5, b = 1.5)

#> sigma^2 ~ Gamma(shape = 0.5, rate = 0.5)

#> nu ~ Infinity

#> rho ~ Constant(value = 0)

#>

#> Stored 10000 MCMC draws after a burn-in of 1000.

#> No thinning.

#>

#> Posterior draws of SV parameters (thinning = 1):

#> mean sd 5% 50% 95%

#> mu -10.2642 0.5215 -10.9605 -10.226 -9.661

#> phi 0.5703 0.2863 0.0324 0.618 0.940

#> sigma 0.5192 0.2763 0.1077 0.495 1.014

#> exp(mu/2) 0.0061 0.0015 0.0042 0.006 0.008

#> sigma^2 0.3460 0.3468 0.0116 0.245 1.029

#>

#> Posterior draws from the auxiliary SV model were re-sampled after the MCMC

#> procedure ended to correct for model mis-specification.

#> Re-sampling of parameters and latents was of little practical importance:

#> - max reachable entropy for this sample size: 9.21034,

#> - entropy of the re-sampling weight distribution: 9.210184

#>

if (FALSE) { # \dontrun{

# Parallel multicore chains (not available on Windows)

res <- svsample(y, draws = 30000, burnin = 10000,

parallel = "multicore", n_chains = 3, n_cpus = 2)

# Plot using a color palette

palette(rainbow(coda::nchain(para(res, "all"))))

plot(res)

# Use functionality from package 'coda'

## E.g. Geweke's convergence diagnostics

coda::geweke.diag(para(res, "all")[, c("mu", "phi", "sigma")])

# Use functionality from package 'bayesplot'

bayesplot::mcmc_pairs(res, pars = c("sigma", "mu", "phi", "h_0", "h_15"))

} # }

# }

########################

# Further short examples

########################

y <- svsim(50, nu = 10, rho = -0.1)$y

# Supply initial values

res <- svsample(y,

startpara = list(mu = -10, sigma = 1))

#> Done!

#> Summarizing posterior draws...

# \donttest{

# Supply initial values for parallel chains

res <- svsample(y,

startpara = list(list(mu = -10, sigma = 1),

list(mu = -11, sigma = .1, phi = 0.9),

list(mu = -9, sigma = .3, phi = 0.7)),

parallel = "snow", n_chains = 3, n_cpus = 2)

#> Done!

#> Summarizing posterior draws...

# Parallel chains with with a pre-defined cluster object

cl <- parallel::makeCluster(2, "PSOCK", outfile = NULL) # print to console

res <- svsample(y,

parallel = "snow", n_chains = 3, cl = cl)

#> Done!

#> Summarizing posterior draws...

parallel::stopCluster(cl)

# }

# Turn on correction for model misspecification

## Since the approximate model is fast and it is working very

## well in practice, this is turned off by default

res <- svsample(y,

expert = list(correct_model_misspecification = TRUE))

#> Done!

#> Summarizing posterior draws...

#> No computation of effective sample size after re-sampling

print(res)

#>

#> Summary of 'svdraws' object

#>

#> Prior distributions:

#> mu ~ Normal(mean = 0, sd = 100)

#> (phi+1)/2 ~ Beta(a = 5, b = 1.5)

#> sigma^2 ~ Gamma(shape = 0.5, rate = 0.5)

#> nu ~ Infinity

#> rho ~ Constant(value = 0)

#>

#> Stored 10000 MCMC draws after a burn-in of 1000.

#> No thinning.

#>

#> Posterior draws of SV parameters (thinning = 1):

#> mean sd 5% 50% 95%

#> mu -10.2642 0.5215 -10.9605 -10.226 -9.661

#> phi 0.5703 0.2863 0.0324 0.618 0.940

#> sigma 0.5192 0.2763 0.1077 0.495 1.014

#> exp(mu/2) 0.0061 0.0015 0.0042 0.006 0.008

#> sigma^2 0.3460 0.3468 0.0116 0.245 1.029

#>

#> Posterior draws from the auxiliary SV model were re-sampled after the MCMC

#> procedure ended to correct for model mis-specification.

#> Re-sampling of parameters and latents was of little practical importance:

#> - max reachable entropy for this sample size: 9.21034,

#> - entropy of the re-sampling weight distribution: 9.210184

#>

if (FALSE) { # \dontrun{

# Parallel multicore chains (not available on Windows)

res <- svsample(y, draws = 30000, burnin = 10000,

parallel = "multicore", n_chains = 3, n_cpus = 2)

# Plot using a color palette

palette(rainbow(coda::nchain(para(res, "all"))))

plot(res)

# Use functionality from package 'coda'

## E.g. Geweke's convergence diagnostics

coda::geweke.diag(para(res, "all")[, c("mu", "phi", "sigma")])

# Use functionality from package 'bayesplot'

bayesplot::mcmc_pairs(res, pars = c("sigma", "mu", "phi", "h_0", "h_15"))

} # }